6 Chapter 6: Before the Client Meeting

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- Define emotional intelligence and explain the roles of self-awareness and self-management in financial advising.

- Apply emotional intelligence strategies to build client trust and manage difficult conversations.

- Describe the principles of relationship selling and how they support ethical advising practices.

- Identify and explain the three key knowledge areas for finance professionals: process knowledge, product knowledge, and client knowledge.

- Differentiate between personality types and adapt communication styles accordingly.

- Outline the steps required to prepare effectively for a client meeting, including impression management and ethical considerations.

- Compare communication methods (phone, email, and virtual platforms) for initiating and scheduling client meetings.

- Explain how technology has changed client engagement and how to adapt to virtual or hybrid advising.

- Develop strategies for effective time management in a financial services context.

Revised: Relationship-Selling and Emotional Intelligence in Action

Relationship-selling is more than a sales technique — it is the cornerstone of ethical advising in financial services. It prioritizes trust, long-term value, and a deep understanding of the client’s needs and goals. While introduced in earlier chapters, we now examine how emotional intelligence enhances this approach.

Building Trust through Self-Awareness

Finance professionals must recognize that clients often approach financial conversations with emotions ranging from anxiety to confusion. By applying self-awareness — understanding your own emotional triggers and how your behavior is perceived — you can avoid projecting impatience or pressure during client conversations.

For example, an advisor who is aware of their tendency to speak quickly when nervous can learn to pause and create space for clients to process information. This supports a more trusting and collaborative relationship.

Meeting Emotional Needs through Self-Management

Emotional intelligence has been defined as “the ability to acquire and apply knowledge from one’s emotions and those of others to produce beneficial outcomes” (Kidwell, et al., 2011). Clients value advisors who can stay calm under pressure, especially when discussing sensitive topics like debt, retirement savings shortfalls, or complex investments. Self-management allows finance professionals to regulate their reactions, maintain professionalism, and create a safe space for honest dialogue.

A client expressing hesitation about an investment may not be rejecting your advice — they may need reassurance. Your ability to respond with empathy rather than defensiveness can keep the conversation moving forward and preserve trust.

The Long-Term Value of Relationship-Selling

When finance professionals invest time in truly understanding their clients, they gain more than just a transaction — they gain loyalty. This client loyalty often results in future business and valuable referrals. Over time, the advisor-client relationship becomes one of partnership, not persuasion.

This approach also aligns with ethical best practices: putting the client’s needs first, practicing full disclosure, and focusing on long-term outcomes rather than short-term sales goals. Click on the link to take the free Emotional Intelligence Quiz from the Institute of Health and Human Potential.

Building Credibility through Knowledge

There are three major areas of knowledge that are the most important for finance professionals:

- process knowledge

- product knowledge

- customer/situational knowledge

Process Knowledge

Process knowledge refers to your understanding of the relationship building process (discussed in more detail in later chapters). If a finance professional has a good grasp of the relationship building process, they will have more effective conversations with their clients. The relationship building process revolves around how to effectively communicate with a client by being adept at the following:

- doing research and other background investigative activities (which should be completed prior to the sales conversation)

- understanding the various aspects of client conversations… from making a connection to identifying and exploring needs to questioning and active listening

- knowing how to best present a customized solution, handle client objections, and finalize the necessary elements after the conversation

- ensuring that the client feels valued so a long-term relationship can be built and maintained.

Product Knowledge

In order to build trust and long-term relationships in business, credibility is essential. Finance professionals must have considerable knowledge about the products and services available to clients. Possessing the knowledge necessary to help clients achieve their goals is one major way finance professionals gain credibility with their potential clients.

Other points to consider when considering credibility:

- Having prior knowledge of the topics your client wants to discuss will be incredibly helpful to your preparation and research.

- In advising conversations, you will commonly find that the client does not know what it is that they need to do to achieve their goals. They are coming to you to guide them, and you should be prepared to take the lead and educate them.

- You need to be ready to pivot the conversation, as it may segue from a discussion about purchasing a home to a conversation about a registered education savings plans (RESPs) when a couple mentions they expecting a child in 6 months.

Clients seek an expert to assist them with concerns about their financial situation. Putting a client at ease early on in a conversation is when the advisor can demonstrate their confidence by having a solid understanding of the product knowledge of the products/services they offer. When clients can have their questions answered correctly, they gain trust in the advisor.

Client Knowledge (Know Your Customer)

Know Your Customer, commonly known as KYC in the finance industry, is often used by banks and financial institutions as a way of identifying their clients in order to prevent fraud. KYC is important to finance professionals because gaining an understanding of who your client is and what they care about will help build and foster the relationship you have with them. For example,

- knowing a client’s age can tell you what stage of life they are in and may provide insight into what their financial needs are.

- employment information can provide critical information you may want to explore (e.g., does the client’s employer have a pension and or retirement plan?).

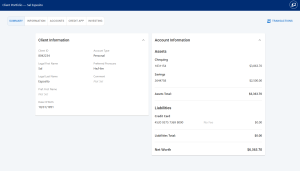

[Figure 6.1] Client and account information. (Source: NAITLAB Financial, 2025)

In addition, knowledge about the client’s abilities to manage their finances can provide insight into how the client makes decisions. Knowing what challenges they face provides an opportunity for you to bring value by presenting the benefits of a product or service your financial institution offers. Understanding the unique situation of the client can help you determine what is motivating them to work with a finance professional and financial institution. Finally, client and situational knowledge would allow you to customize the advising conversation to confirm their needs and motivations and then connect the benefit of your product or service to those needs and motivations.

Customer Personalities

Understanding your own emotions is only one part of emotional intelligence—equally important is recognizing how your client thinks, feels, and reacts. This is where an awareness of different client personality types becomes essential. There are different personality types that a client can have, and these personality types are important understand. Understanding personality types can help a finance professional navigate client conversations. According to Paresh Jadhav, Director of Modernization Business, there are four personality types:

- driver

- analytical

- expressive

- amiable

To better understand each of these personality types, it is important to distinguish them from each other and explore how to best interact with each of them (Jadhav, 2019).

Drivers

Drivers are goal-oriented individuals. They are dedicated to their success and finding ways to achieve it. They can make decisions quickly because they know what outcomes they are seeking. Drivers can also be competitive in their endeavours, as they want to succeed in their activities. This type of individual can be impatient and controlling at times. They want to get their information fast so they can make a decision quickly.

How can you identify a driver? According to Jadhav, the driver will usually speak in declarative sentences and ask few questions. The volume they speak at is somewhat louder than average, and they are animated while speaking.

Jadhav’s recommendations for interacting with a driver:

- Professionalism is always important. Always be prepared when meeting with an assertive personality type. If you do not know the answer to a question, let the client know that you will follow up instead of giving them a partially correct answer.

- Drivers appreciate efficiency. Don’t waste their time repeating facts or building up to your point.

- Emphasize how your product/service will solve their problems.

- As drivers are not great listeners, keep statements short and to the point.

Image generated using the prompt “Create an image of the Driver personality,” sourced from OpenAI, 2025.

Image generated using the prompt “Create an image of the Driver personality,” sourced from OpenAI, 2025.

Analytical

Analytical clients love data, facts and figures. They like a straightforward approach to conversation. Analytical clients do their research prior to meetings, which assists them in making decisions quickly. An analytical person can be logical and cautious in their approach.

How can you identify an analytical client? They tend to be less expressive and are concerned with facts over emotion. They may be less interested in building a relationship with the finance professional. They will often present as serious, direct and formal.

Image generated using the prompt “Create an image of the Analytical personality,” sourced from OpenAI, 2025.

Jadhav’s recommendations for interacting with an analytical client:

- Never rush an analytical client. Be prepared for a more extended conversation.

- Assume they are prepared and have done their research.

- Avoid making high-level claims. Always provide data when you make an assertion, or you risk losing credibility.

- Provide as much detailed information as possible. Do not try to force a relationship that’s not there; the analytical client could become annoyed.

Expressive

Expressive clients feel that relationships are important. They tend to care for others well being and consider how the decisions they make could impact the people around them. An expressive client can be creative, outgoing and spontaneous. They value respect, loyalty and friendship.

How can you identify an expressive client? They often present with high energy and are willing to engage. The expressive client seeks to connect with others and desires to know individuals more personally. When they speak, they typically express themselves in statements rather than questions.

Image generated using the prompt “Create an image of the Expressive personality,” sourced from OpenAI, 2025.

dhav’s recommendations for interacting with an expressive client:

- Present previous client experiences (while still maintaining client privacy.) Expressive people want to be reassured that you are looking out for them, and what better way to prove your track record than to share stories of how your client service impacted other people’s lives?

- Emphasize an ongoing relationship.

- Do not focus extensively on facts and figures. Data is essential, but an expressive client will ultimately want to know how their buying decision affects their finances on a human level.

- Summarize along the way. You want to continually paraphrase and get their buy-in to ensure agreement and provide reassurance.

Amiable

Amiable clients value personal relationships and want to trust their finance professional. They can be enthusiastic and enjoy taking on new challenges. Decisions will not be arrived at quickly, meaning that the client conversation will likely be longer than usual.

How can you identify an amiable client? Amiable individuals are usually great listeners and may ask more personal questions to get to know the finance professional outside of their role. They tend to be friendly, calm and laid-back, even in client meetings.

Image generated using the prompt “Create an image of the Amiable personality,” sourced from OpenAI, 2025.

Jadhav’s recommendations for interacting with an amiable client:

- Help them visualize the outcomes that could be achieved with the help of your product or service.

- Take time to build rapport. Amiable clients will need to feel safe in their relationship with your company before they will be comfortable doing business with you.

- Bring up similar client stories, provide examples where clients have successfully used your product/service. Flesh out the story… Why did the client come to you? Which features were most important? Details like these are convincing for an amiable person.

- Take the role of an expert and walk them through the decision-making process. Instead of overwhelming an amiable client with information, help them through the process and act as an advisor.

Preparing to Meet the Client

First impressions are critical — research shows that people form opinions within the first seven seconds of meeting someone(Willis & Todorov, 2006). In financial advising, these early moments can shape the client’s level of trust and openness throughout the relationship. For this reason, impression management is not just professional etiquette — it’s an ethical responsibility. Clients deserve to feel valued, respected, and confident in the advisor’s capabilities.

Moreover, preparation reflects the core of emotional intelligence:

-

Self-awareness is required to assess your tone, posture, and presentation style.

-

Self-management is needed to regulate stress, remain present, and engage positively — even after a difficult day or meeting.

.Seven Steps to Prepare for a Meeting

The following seven steps expand on the ways to prepare for a client meeting.

Step 1: Appearance. It may seem that having a well-prepared appearance is simple common sense, but it is essential to making a good first impression. A finance professional should be dressed according to their company’s dress code. You should also take into consideration what your clients would expect their finance professional to be wearing.

Step 2: Attitude. Being present is critical for any client interaction. A positive attitude ensures the finance professional is mentally prepared to meet with clients. You will often be faced with challenging situations when dealing with clients. Taking a “time out” after a stressful situation can help you to clear your mind and be ready and prepared for the next client.

Step 3: Clear desk policy. Presenting yourself as prepared and organized is critical to setting the tone of your meeting. Your client wants to know that they are your priority. Having a clear desk, meaning all papers and files are secured and put away, is also important for sensitive information privacy.

Step 4: Fundamentals. It is important to review the client’s name and their preference for how they want to be addressed. You want to respect a client’s pronouns and name pronunciation. For new clients, you should review the appointment notes to ascertain the client’s purpose of the meeting. When you first greet the client, be sure to confirm their preference on how they would like to be addressed and the pronunciation of their name.

Step 5: Set the stage. Review the current account holdings your client has with your financial institution. This information is important because it allows you to anticipate what you may be asked about during the meeting. It can also help you determine if there are opportunities to recommend or other products/services that the client might find beneficial. Look for gaps you may want to discuss. Create an agenda of points to be addressed in the meeting. If all agenda points are not addressed, be sure to document that information in your notes for the next client meeting.

Step 6: Creature comforts. The environment where the meeting takes place is also important. It should not be too hot or too cold. You should have beverages on hand (e.g., coffee and or water.) Ensuring that a client is comfortable and free of distractions (like thirst) allows them to focus on the discussion.

Step 7: All about you. Clients will want to know who they are working with, have a credibility statement prepared. Sharing appropriate personal details can humanize the advisor-client relationship, but must be done thoughtfully and ethically.

Prep Lists

Some institutions or companies may have premade checklists to assist the finance professional in preparing for their meeting. Click the link to see an example of client meeting prep checklist (Kitces.com).

Additional Preparation Tips

Prior to the client meeting, it is advisable to review any notes previous professionals have entered. Often, there are comments relating to previous interactions with the client. This information is important because it can ensure you don’t propose something to the client that has been addressed in the past, and you can avoid frustrating the client and wasting their time.

As was touched on earlier, knowing the reason for the meeting is important. You want to be prepared to address the topic of the meeting. For example, if the purpose of the meeting is to discuss investments, you will want to make sure that you have key investment websites open in tabs on your computer/device. Having information readily accessible reinforces your credibility and helps build trust with your client.

Once you have completed your preparation, you are ready to meet your client!

Seeking Clients in the Digital Age

Once prepared, advisors must take the initiative to reach out to clients — both new and existing — using a variety of contact methods. In order for finance professionals to set up meetings with potential clients, there needs to be a process in place for generating, qualifying, contacting and setting appointments with potential clients (often called leads). Many financial institutions have software systems to assist with this process. Software systems will identify client gaps/needs based on data analytics, and the software system will provide suggestions of products/services to possibly offer the client. A successful finance professional should schedule time in their day to: 1) contact new clients and 2) contact existing clients with products and services recommendations.

Contacting Clients

Once a new client has been identified, the next step involves making contact with the client in an attempt to begin a conversation. Where no relationship exists, contacting a potential client is referred to as cold-calling or cold calls. Cold calls can be done in-person, on the phone, or via email or social media message. If the client has a previous connection with the finance professional or financial institution, the call can become ‘warmer’. The initial cold calls you make can be nerve-wracking, but the more experience you have with these interactions, the easier they become.

Generally speaking, when cold-calling a new client, the goal is not to sell a product or service (or even discuss a product or service.) The primary goal of a cold call is to set an appointment for a later time. At this appointment, the client will have a secured block of time with no distractions. The finance professional will have time to learn about the client’s needs and discuss how the products and services they offer could potentially address those needs.

Setting Appointments (Email vs. Phone)

It’s important to understand the differences associated with contacting clients via email (or other written message) versus the phone. Emails and other written messages are a type of one-way communication. The primary advantage of one-way communication is that you have complete control of your message and ample time to craft it and any subsequent responses. A key limitation of one-way communication is, without being able to interpret voice inflection or body language, interpreting the meaning and subtext of written words can be challenging, both for you and the client.

In order for emails to be effective, they need to be relatively brief (i.e., short paragraphs, possibly a bulleted list.) Emails need to create as much interest and connection as possible in the subject line and/or at the very beginning of the message. Your message should be compelling and, if possible, mention a common connection. It is important to use the contact information provided on the financial institutions website and use the preferred method of contact.

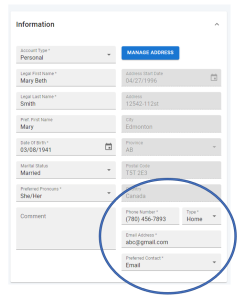

[Figure 6.3] Note “Preferred Contact” method in the client information. (Source: NAITLAB Financial, 2025)

The initial email with a new client should have a short introduction, describing the finance professional and the financial institution they are representing. This helps a new client understand who is trying to connect with them. The email could also contain information on current promotions or mention a need the client may not be aware that exists. An example could be one of their investments, a GIC is coming to the end of the investment term, and no specific instructions are on file. The advisor could email to remind the client of the upcoming renewal and request a meeting to get the renewal instructions.

Phone

Technology-driven Advising

Historically, finance professionals aimed to meet clients in person. However, the COVID-19 pandemic accelerated a shift toward virtual advising. Advisors and clients alike had to quickly adapt to tools such as Zoom, Webex, and screen-sharing software to continue doing business remotely.

This shift revealed important long-term benefits. Virtual meetings can increase accessibility for clients with physical limitations or social anxiety. They also provide flexibility for clients with busy schedules or who live in remote areas.

Today, the most successful advisors understand how to blend in-person and virtual approaches based on client preference. Using technology effectively is not just about efficiency — it’s about creating inclusive, client-centered experiences.

Importance of Time Management

Tips for Managing Your Time

-

At the start of the day, look at your schedule and set up a plan of action.

-

Dedicate a block of time to completing files, notes and other paperwork.

-

Dedicate a block of time to contacting new clients (schedule this block around your client meetings.)

-

Ask the individual who manages clients to help manage the time you spend with clients; if they see you are going too long, ask them to call you or interrupt the conversation.

-

Some client meetings may require more than one appointment. Consider meeting a client at their place of business to make it more convenient for them.

-

Make sure you account for travel time in your calendar so you aren’t late to client meetings.

Summary

In summary, emotional intelligence — particularly self-awareness and self-management — plays a critical role in the financial advising profession. Relationship selling, grounded in ethical communication and empathy, allows finance professionals to build lasting, trust-based client relationships.

Credibility is enhanced through mastery of process knowledge, product knowledge, and client-specific insights. Preparing thoroughly for meetings — from first impressions to reviewing account information — supports ethical, personalized advising.

Technology has expanded how advisors connect with clients. Virtual meetings provide flexibility and accessibility, allowing professionals to tailor communication methods to each client’s preferences and needs. Integrating in-person and digital approaches ensures inclusive, client-centered service delivery.

Finally, effective time management enables finance professionals to balance client relationships with operational demands. Structuring the day with intention helps advisors meet both their goals and their clients’ expectations.

REFERENCES

Kidwell, B., Dardesty, D.M., Murtha, B.R., Sheng, S. (2011). Emotional Intelligence in Marketing Exchanges. Journal of Marketing, 75(1), 78-98.

OECD. (2016). OECD/INFE International Survey of Adult Financial Literacy Competencies. OECD, Paris.

Willis, J., & Todorov, A. (2006). First impressions: Making up your mind after a 100-ms exposure to a face. Psychological Science, 17(7), 592–598. https://doi.org/10.1111/j.1467-9280.2006.01750.x

Wikipedia. (2022). COVID-19 Pandemic in Canada. Wikipedia. Retrieved March 30, 2022.

Media Attributions

- Screenshot 2025-06-18 130327

- Driver_Personality_Type_Image

- Analytical_Personality_Type_Image

- df21937a-baaa-49c0-b300-8e2e28b0fea1

- Amiable_Personality_Type_Image

- Screen Shot 2022-03-29 at 1.57.34 PM

- Screenshot 2025-06-18 130745