4 Chapter 4: Sales versus Advising.

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- Define financial advising and differentiate it from traditional sales roles.

- Summarize the evolution of sales and its impact on financial services.

- Compare transactional and relationship selling approaches.

- Explain the role of credentialing bodies in promoting ethical and transparent practices.

- Assess how compensation models influence advisor behaviour.

- Discuss the ethical use of social media in financial advising.

- Recognize how finance professionals build trust and challenge industry stereotypes.

Defining Advising

What is Advising?

Why is it so important?

Is financial advising simply sales?

These are essential questions for anyone pursuing a career in finance. Future finance professionals must understand that advising is more than offering financial products — it’s about serving as a trusted guide through a client’s financial life. In Canada, where the financial industry is highly regulated, professionals must perform due diligence, meet compliance standards, and demonstrate ethical behaviour while growing their book of business.

Canadians seek knowledgeable advisors to support their short- and long-term financial goals. These clients aren’t just looking for a product — they’re looking for confidence, clarity, and consistency in the advice they receive. As such, advising involves listening, understanding individual circumstances, identifying needs, and developing personalized recommendations.

Although advising includes elements of sales, it is a service-driven role, rooted in client trust and ongoing relationships, rather than one-time transactions.

A Brief History of Sales and Its Impact on the Finance Industry

Sales as a profession has evolved significantly over the past century — from the aggressive, product-pushing tactics of the early 20th century to more customer-centric and ethical approaches (Swensson, 2015; SalesForceSearch, 2013). Historically, salespeople were trained to focus on closing the deal quickly, regardless of whether the product truly met the client’s needs (Kotler & Armstrong, 2008).

During the post-WWII economic boom, the sales profession became more structured, with formalized quotas, commissions, and sales training programs (Kotler & Armstrong, 2008). However, this system also introduced high-pressure tactics that reinforced the stereotype of the untrustworthy, quota-driven salesperson (Rao, n.d.; SalesForceSearch, 2013).

In more recent decades, technology has reshaped the profession. As Petrone (2023) explains, twenty years ago CRM systems were in their infancy, smartphones did not exist, and door-to-door selling remained common. Today’s sales professionals face new expectations: buyers are more informed, expect advisors to understand their industries, and demand personalized, consultative experiences. While tools and techniques have changed, the foundation of successful sales — relationships, integrity, and communication skills — remains constant.

The finance industry has experienced this evolution firsthand. The Canadian Bankers Association (CBA) notes that the first bank in Canada was established in 1891. Today, more than 80 domestic and foreign banks operate across the country (Canadian Bankers Association, n.d.). Technology has accelerated this growth, and recent global events — such as the COVID-19 pandemic — forced financial institutions to rapidly adopt virtual models of client engagement. As a result, adaptability and relationship-building in digital spaces have become critical components of effective financial advising.

Why Advising is Different from Traditional Sales

While advising may involve selling investment or insurance products, it differs significantly from a traditional sales role. Sales is often transactional and product-focused, with the goal of meeting quotas or closing deals. Advising, on the other hand, emphasizes relationship selling — a long-term, trust-based approach that prioritizes the client’s best interest.

Finance professionals must be especially mindful of the delicate relationship that forms with clients. They are not just selling financial solutions; they are also selling themselves — their credibility, ethics, and professionalism. Clients must believe that their advisor genuinely understands and supports their goals.

Relationship selling, by definition, is a technique where the advisor focuses on building a personal connection with the client. Trust is developed over time by consistently adding value, demonstrating empathy, and maintaining open lines of communication before recommending any specific solution.

Unlike traditional sales roles, financial advisors are also held to higher regulatory and ethical standards. In Canada, advisors are expected to meet obligations such as suitability assessments, full disclosure, and transparent documentation. These expectations reflect the advisor’s responsibility to act in the client’s best interest, not just to complete a sale. In Canada the body that oversees Financial Institutions and their sales practices is Financial Consumer Agency of Canada(FCAC). On March 20th 2018, the FCAC published a report titled “Domestic Bank Retail Sales Practices Review”. The main findings show that the retail banking culture employees to sell products and services, and rewards them for sales success(Financial Consumer Agency of Canada, 2018). Measures were recommended to the retail banks in Canada to establish a formal sales practices governance framework.

It is important to note that in the finance industry that all bodies have a code of ethics – what is present in all of these codes is that protection of the client is critical to ensure that key client components are considered and that the client needs are always considered. We will refer to two Credentialing bodies in Canada in the next section on how Ethics plays a key role for client interactions.

In short, while sales and advising may overlap in action, their intention, accountability, and client impact are fundamentally different. Understanding this distinction is essential to becoming an ethical, effective finance professional.

Why Ethics in the Finance Industry are Crucial

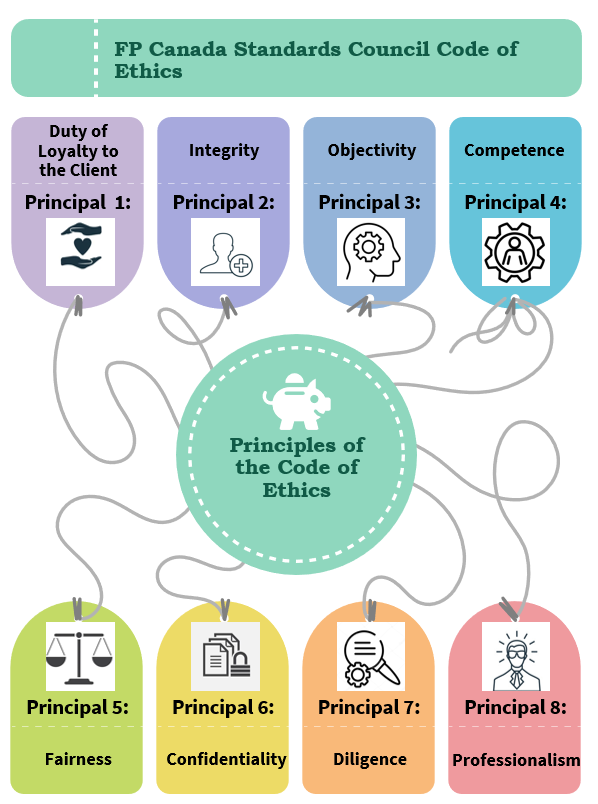

In recent years, the finance industry has had its challenges, and this has impacted how it is perceived in Canadian society. In 2017, the media reported that employees of one of the largest banks in Canada admitted to unethical practices. The employees claimed they acted in unethical ways due to the pressure they felt to achieve their sales targets. Since the time these events made mainstream news, financial institutions have made it a priority to focus on the ethical behaviour of their employees. They want to reassure their clients that their institution is trustworthy. Consider the Standards of Professional Responsibility for Certified Financial Planners (CFPs) and Qualified Associate Financial Planners (QAFPs) published in July 2021 by FP Canada Standard Council™. In this document, the council describes their Code of Ethics, which identifies the conduct that is required from their certificates and their peers.

FP Canada requires certificants to have discretionary authority over their clients’ investments, and they are subject to a fiduciary duty that requires them to act solely in their clients’ interests (FP Canada Standards Council, 2021). In Canada, a fiduciary duty refers to the relationship in which one party (the fiduciary) is responsible for looking after the best interests of another party (the beneficiary) (Litman, 2021). Finance professionals must recognize the significance of their roles, and the influence they have on their clients. They have a responsibility not only to their clients but to the entire finance industry. It is critical to the future of the finance industry that it becomes more transparent and ethical. All professionals need to ensure that ethical behaviour is demonstrated with their clients on a daily basis. It is vital that finance professionals be recognized and trusted for the experts they are.

Example: Wells Fargo Account Fraud ScandalThe recent account fraud scandal that Wells Fargo was involved in underscores the importance of ethical compensation strategies. The top management at Wells Fargo knew that their stock price would be enhanced if they could report a high average number of products per customer. Wall Street felt that a bank customer having multiple bank products was a good measure of customer loyalty. Therefore, Wells Fargo strongly encouraged and pressured their bank managers and salespeople to cross-sell products to inflate this metric. However, the intense pressure and focus on this metric led to unethical behavior, where additional accounts were being opened without customer knowledge. The impact, when this scandal came to light in 2016, was very damaging to the Wells Fargo brand and is a key reason why companies need to look at sales strategies in terms of how they might motivate unethical (or ethical) behaviors. |

Varied Complexity and Compensation

Depending on the complexity of the financial institutions (FIs) financial products and/or value proposition, different levels of expertise are required from the advisors and planners. In addition, compensation for finance professionals varies greatly across the finance industry, ranging from hourly pay… to 100% commission… to salary plus commission and/or bonus compensation structures.

Finance professionals enjoy a very comfortable living. The average financial advisor salary in Canada is $94,060 or $45.22 per hour. Entry level positions can start at $60,000 per year, while experienced advisors can make up to up to $119,325per year (June 2025). It is also important to note that different institutions and companies can have different compensation models. These can vary from salary to commission driven income or they can be a combination of both.(SmartAsset, n.d.). Credentialling bodies emphasize transparency in how advisors are compensated, as seen in their code of ethics for both FP Canada and the CFA Institute.(FP Canada Standards Council, 2023; CFA Institute Research & Policy Center, 2018).

Social media is a vital tool in helping the finance professional grow their book of business. According to the 2020 LIMRA Insurance Barometer Study, the proportion of consumers seeking a financial advisor is growing (Scanlon, et al, 2020). One in four is looking for an advisor, a rise of 64% in three years. The data suggests that some 64 million consumers seek financial guidance, and the most significant segment of this market is Generation X and Millennials. Furthermore, 49% of those seeking an advisor say they are looking for them on social media platforms (Bernas, 2021). Social Media use needs to be done in accordance with credentialling bodies and their guidelines. (FP Canada Standards Council, 2023; CFA Institute Research & Policy Center, 2018).

Ultimately, the financial professionals success depends not only on their technical knowledge and compensation model but also on how well they balance ethical responsibility with evolving tools like social media to grow their business authentically.

Breaking the Negative Stereotype of Salespeople/Finance Professionals

The history of sales, and the questionable sales techniques still employed by some modern companies, has contributed to the persistent stereotype that salespeople/finance professionals are unprofessional and not to be trusted. The perception, which is still prevalent today, is that salespeople/finance professionals are often deceptive, unethical, untrustworthy, focused on personal gain and do not add value to customers or society.

However, ethical, relationship-focused salespeople/finance professionals are intent on solving client issues, helping people and providing accurate information so a client can make an educated and informed decision about their finances. Finance professionals also learn valuable information working directly with their clients, and this information can be a resource to help the financial institution continue to grow their business overall.

Finally, finance professionals will often be the only true advocates for their clients. By working directly with a clients, finance professionals can learn about client needs and overall perspectives, and then they can voice this information to the other functional areas of their financial institution. In doing so, finance professionals can serve to make sure that the focus of their financial institution always remains on bringing clients value and building long-term relationships.

Throughout this textbook, we will explore the concept of relationship selling and its application in the financial services industry. Clients are looking for guidance and direction, which is very different from purchasing something tangible they can hold in their hands. We will learn what barriers clients have in their decision-making process when it comes to solutions, and where finance professionals can guide clients to a well-thought-out and communicated solution. Concepts that will be addressed throughout the book include:

- how to connect and build a relationship with a client

- how to demonstrate interpersonal skills and balance them with industry standards

- how to recommend solutions to clients in a confident manner

- what a financial professional can expect to see on a daily basis.

- how to grow and maintain your book of business

The first step, though, is to begin to understand our clients and what can can impact their purchasing decisions.

Summary

While this chapter discussed how sales evolved, this text focuses on creating those connections with our clients to gain their trust and, ultimately, their business. Finance professionals are advocates for their clients and will highlight the importance of relationship selling in the financial services industry. The textbook will explore various concepts, including building relationships, demonstrating interpersonal skills while adhering to industry standards, and confidently recommending solutions. Understanding clients and their decisions is the initial step in this process.

REFERENCES

Bernas, R. (2021, March 2). Social Media: A Financial Professional’s New Best Friend. The Field Exclusive News.

Canadian Bankers Association. (n.d.). Milestones in Canadian banking. https://cba.ca/article/milestones-in-canadian-banking

ERI SalaryExpert. (2025, June 18). Financial advisor—Canada: Salary overview. https://www.salaryexpert.com/salary/job/financial-advisor/canada

Financial Consumer Agency of Canada. (2018, March 20). Domestic Bank Retail Sales Practices Review. Government of Canada. https://www.canada.ca/en/financial-consumer-agency/programs/research/bank-sales-practices.html

FP Canada Standards Council™. (2021, July 1). Standards of Professional Responsibility FP Canada™.

Gallo, Amy. (2014, October 29). The Value of Keeping the Right Customer. Harvard Business Review.

Kotler, P., & Armstrong, G. (2008). Principles of marketing (12th ed.). Pearson Education.

Litman, M.M. (2021, April 14). Law of Fiduciary Obligation. The Canadian Encyclopedia.

Petrone, P. (2023, May 2). The past, present, and future of sales. LinkedIn. https://www.linkedin.com/pulse/past-present-future-sales-paul-petrone/

Rao, R. (n.d.). The evolution of selling. LinkedIn. https://www.linkedin.com/pulse/evolution-selling-ramesh-rao/

SalesForceSearch. (2013, January 1). 3 sales techniques of the past, present, and future. https://www.salesforcesearch.com/blog/3-sales-techniques-of-the-past-present-and-future/

Scanlon, J.T., Leyes, M., Wood, S. (2020, May 22). 2020 Insurance Barometer Study. LIMRA.

SmartAsset. (n.d.). A guide to financial advisor compensation models. SmartAsset. Retrieved June 18, 2025, from https://smartasset.com/financial-advisor/a-guide-to-financial-advisor-compensation-models

Swensson, R. (2015, January 1). Salesmanship and sales management: A historical framework. LinkedIn. https://www.linkedin.com/pulse/salesmanship-sales-management-historical-framework-roger-swensson/

Credentialing bodies and organizations are entities responsible for establishing and maintaining standards of competence and professionalism in specific industries or fields.