3 Chapter 3: Maintaining and Growing Your Book of Business/Professional Practice

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- Explain the importance of treating your book of business as your own professional practice.

- Identify how financial advisors allocate their time and the activities that drive success.

- Apply effective strategies to build, grow, and maintain a client base.

- Develop and nurture Centres of Influence (COIs) to support business development

- How to use social media for professional visibility and client acquisition.

- Utilize networking strategies to expand your reach and acquire new clients.

- Recognize the traits and habits of successful financial advisors.

- what traits successful financial advisors possess.

- Create a personalized business plan that outlines your goals, strategies, and focus areas.

Establishing Your Own Business/Professional Practice

A book of business is the list of clients maintained by someone who provides specialized professional services, such as financial services. Ideally, the professional regularly adds clients and customers to keep their book of business growing (Kolakowski, 2020).

-

demographics (e.g., age and occupation)

-

accounts the client has with you and other financial institutions; maturity dates should be documented

-

outcomes of client meetings (i.e., the products/services the client has acquired)

-

referrals that you provided to your client

-

potential future needs; gaps you have identified through previous meetings.

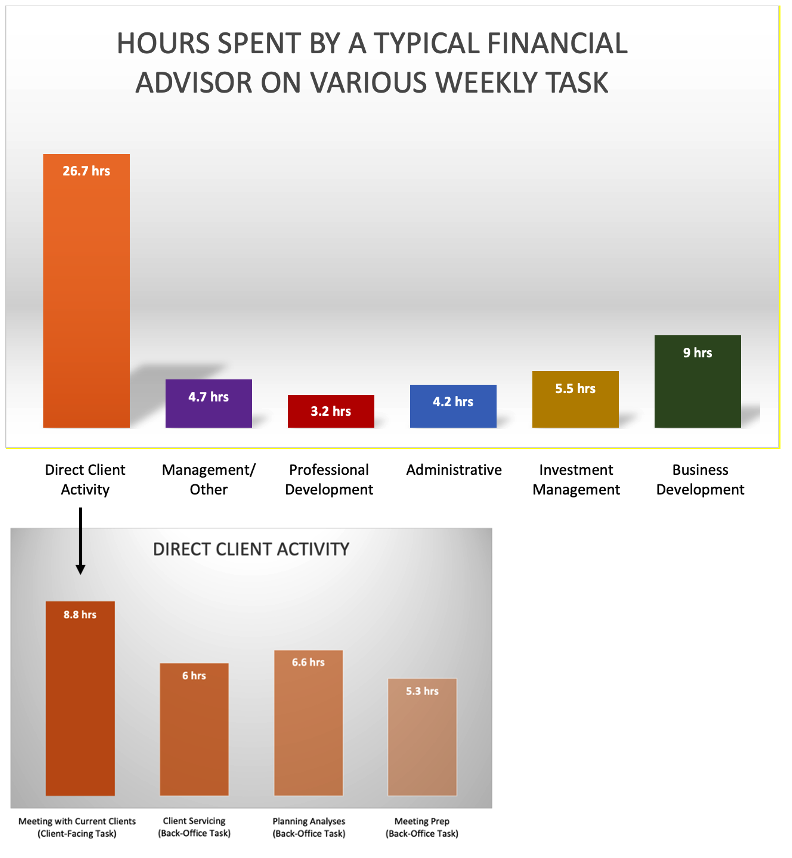

How an Advisor Spends Their Time

-

Advisors/planners spend 43 hours per week working as a financial advisor; of those 43 hours, 26.7 are spent addressing the following direct client needs…

-

They meet with their current clients, on average, 8.8 hours per week.

-

They spend 5.3 hours per week preparing for meetings.

-

They spend 6.6 hours per week answering client questions.

-

They spend an average of 6 hours per week doing follow-through on client servicing tasks.

-

Advisors indicated that finding and getting new clients took, on average, 9 hours per week. This includes 4 hours meeting with prospective clients and another 5 hours working on marketing and related business development activities.

-

They spend about 9 hours per week finding and meeting new clients.

-

They spend about 3 hours per week on administrative work and professional development.

-

The spend about 5 hours per week on management tasks (as needed.)

In fact, given that the average experienced lead advisor has 96 clients, the average advisor only spends 2.9 hours per year actually “investment managing” the client’s portfolio (Kitces, 2019).

-

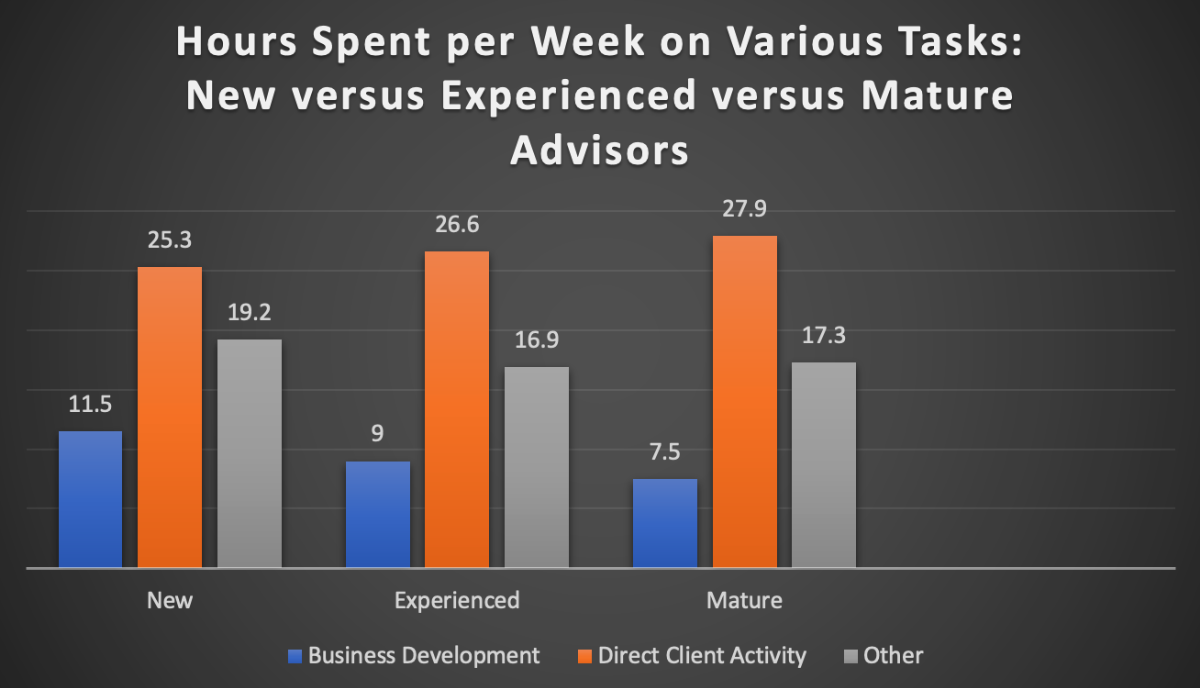

Business development time averages about 21% or about 12 hours per week.

-

Client meetings with current clients averages about 13% of their time or about 7 hours per week.

-

Business development time averages about 17% of their time or about 9 hours per week.

-

Client meetings with current clients averages about 16% of their time or about 8.3 hours per week.

-

Business development time averages about 14% of their time or about 7.5 hours per week.

-

Client meetings with current clients averages about 19% or their time or about 10.2 hours per week.

Watch the video below:

Strategies to Build Your Book of Business as a New Advisor

Centres of Influence

Image generated using the prompt “Create an image of a Centre of Influence,” sourced from OpenAI, 2025.

-

They give you access to a number of potential clients that you can service.

-

They are willing to recommend you and your services to potential clients.

-

They are respected in their industry.

-

A mutual relationship can develop, where you also becomes a Centre of Influence for them.

Networking for Client Acquisition and career sustainability

In addition to building your skills and industry knowledge, one of the most critical activities for any advisor is building and maintaining a strong professional network. Networking is not simply about job hunting; it is an essential part of building your client base and sustaining long-term success in financial services.

Image generated using the prompt “Create an image depicting Networking,” sourced from OpenAI, 2025.

According to the University of Manchester (2023), networking is an essential ability encompassing interpersonal communication, rapport management, and professionalism. These competencies are fundamental to establishing strong client relationships and business growth.

Effective networking allows you to:

- Expand your circle of influence

- Build meaningful relationships with clients, professionals, and community contacts

- Gain referrals and build trust and credibility

- Establish a recognizable personal brand in the industry

Strategic Networking Tips for Financial Professionals

- Look for the Right People

Reach out to former colleagues, community leaders, and industry professionals such as CPAs, lawyers, and mortgage specialists. Attend local business networking events or webinars to connect with new contacts. - Be Proactive

Stay in regular contact with your network through brief updates or messages. Don’t wait until you need something—relationships grow from consistent, genuine engagement. - Offer Assistance

Helping others in your network builds goodwill and positions you as a knowledgeable and dependable resource. If you can’t help directly, connect them with someone who can. - Cultivate Online Connections

Use platforms like LinkedIn to maintain visibility, share insights, and engage with others. Join online groups relevant to financial professionals or your niche market. - Follow Up After Events

Whether in-person or virtual, following up with a new contact after a networking event demonstrates professionalism and interest. A well-timed follow-up can lead to opportunities, introductions, or even new clients. - Develop an Elevator Pitch

Be ready to explain who you are, what you do, and how you help clients—in 30 seconds or less. Practice this so it feels natural when opportunities arise unexpectedly.

Remember, effective networking is not transactional—it is relational. Your goal is to build long-term trust with people who may become clients, refer clients, or support your practice in other ways.

Carve Out a Niche of the Market

Image generated using the prompt “Create an image of a Niche Market for a Financial professional,” sourced from OpenAI, 2025.

Community Engagement

|

Ways for a New Advisor to Find Clients |

|

Growing your network is essential, but that means reaching beyond your inner circle to develop personal relationships with a variety of people. |

|

Look beyond soon-to-be-retirees as clients and find relatively underserved markets, so as to be competitive. |

|

Get involved with your community through volunteering and other programs as a way to feel connected and to find potential client |

Strategies to Grow Your Book of Business

Word of Mouth

Social Media Presence/Website

Being established on social media or having a website is a requirement for today’s businesses. However, having a social media account/website is only beneficial if it’s being actively maintained and updated.

Guest Speaker Opportunities

Pipeline

Traits of Successful Financial Advisors

Successful financial advisors know not only how to manage their clients’ money, but how to ensure their clients feel safe and financially cared for (Anthony, 2022).

|

Traits of Successful Advisors |

|

Successful financial advisors have a large book of client business and a track record of performance and service. |

|

Getting clients and having them stick with you—and recommend you—means being professional and putting your clients first. |

|

At the same time, you need to have a deep understanding of the markets, analytical skills and training, and a passion for finance. |

|

Soft skills can be equally as important as hard skills such as investing acumen and market timing. |

[Table 3.2] Key takeaways from the article, “5 Traits of Successful Financial Advisors”. (Source: Anthony, 2022)

Business Plan for your Book of Business/Practice

Your business plan as a financial advisor exists to help you keep focus and avoid distraction (Kitces, 2015).

1. WHO will you serve? Who is your TARGET MARKET?

3. How will you REACH them?

-

unsolicited referrals

-

proactive introductions

-

professional alliances

-

social prospecting

-

intimate social events

-

educational events

-

social media, website and content marketing.

4. How will you know if it’s WORKING?

5. Where will you focus YOUR TIME in the business?

6. How will you STRENGTHEN the foundation?

The goal here is to do what is necessary to move forward, not everything; as with so much in the business, waiting until perfection may mean nothing gets done at all (Kitces, 2015).

Summary

References

Media Attributions

- 50f1da1b-0dce-4ba1-bb47-80e0a422074e

- 8a1de285-e22d-483e-913b-fec2e814c3f9

- bf56c963-596e-4dbd-8c0d-336b61cde4f1

- a961b643-5417-45e1-a435-218dfac79ff3