7 Chapter 7: Navigating Client Resistance: A Toolkit for Handling Objections

Learning Objectives

Upon completion of this chapter, you should understand:

- Define client objections and identify when they typically arise during the advising process.

- Recognize how low financial literacy and common financial stressors contribute to client objections.

- Apply a structured process to effectively handle objections with professionalism and empathy.

- Anticipate and respond to common client objections using practical, client-centered strategies.

- Demonstrate techniques for maintaining trust and guiding clients toward informed financial decisions.

45% of middle-aged Americans would rather see the dentist than meet with a financial advisor (Perron, 2017).

What are Objections?

Client concerns, resistance, or outright disagreement—these are all types of objections. Anything a client says or does that slows or stops the advising process can be considered an objection. It may sound like “I don’t have the money,” “Let me think about it,” or simply, “No.”.

Image generated using the prompt “Show an Advisor with a client who has an objection,” sourced from OpenAI, 2025.

When Do Clients Object?

Objections can happen at any stage of the client relationship: when trying to book a meeting, during your introduction, or—most often—after presenting a recommendation. Clients may object because they don’t understand, feel overwhelmed, or aren’t ready to make a decision. These are normal moments in the advising process, not signs of failure.

Financial literacy is a key factor. Many clients are unfamiliar with financial terminology or decision-making, and this knowledge gap can trigger resistance.

Why Financial Literacy Matters

The Financial Consumer Agency of Canada (FCAC) completed a survey in 2019, “Canadian Financial Capability Survey (CFCS).” The findings from this survey can help you better interpret the underlying concerns clients may have and will help you develop a solid understanding of challenges facing the majority of Canadians. Understanding what your clients are facing can help you work through any objections that may occur.

Debt Pressures Canadians are Facing

Image generated using the prompt “Show aa couple struggling with mounting debts,” sourced from OpenAI, 2025.

- Canadian household debt represented 179% of disposable income in 2024(Statistics Canada, 2024).

- As of 2024, about 69.8% of Canadians have some form of outstanding debt, including mortgages, student loans, and credit card debt (Made in CA, 2024).

- According to recent data from Statistics Canada in 2023, 35% of Canadians reported finding it difficult to meet their financial needs, which indicates a significant level of financial stress. (Statistics Canada, 2023).

Statistics like these can be overwhelming. If we restate the statistics regarding disposable income it would read as such, “For every $1 a Canadian brings into the home, $1.79 is leaving to be paid towards debt and other necessities.”

How does the high level of household debt among Canadians, as indicated in the 2019 Canadian Financial Capability Survey canadian-financial-capability-survey-2019 , impact your approach as a financial advisor when addressing client objections? How can understanding these statistics help you to better assist your clients in managing their financial situation and concerns?

Impact on Advisor Approach:

-

Empathy-First Communication

Understanding that financial stress is common allows you to approach objections with greater empathy. Clients may resist advice not out of disagreement but due to fear, embarrassment, or financial strain. Acknowledge their concerns sincerely and without judgment. -

Reframing Objections as Opportunities

A client who says “I can’t afford that right now” may be signaling broader cash flow issues. This is a cue to revisit their budget or debt load, rather than push forward with the original recommendation. -

Tailoring Recommendations

Knowing household debt is a common challenge, tailor solutions to be realistic and manageable—for example, starting with debt consolidation or emergency savings before introducing more complex investment strategies. -

Building Trust Through Education

Use the data to educate clients: “You’re not alone. Many Canadians face similar challenges, but there are steps we can take together.” This helps normalize their experience and reinforces that you’re on their side

How Statistics Help You Serve Better:

-

Contextual Awareness: Understanding the national landscape keeps you grounded in what’s realistic for clients and helps avoid recommending overly aggressive financial plans.

-

Informed Planning: You can better prioritize strategies that address the root causes of financial stress—like reducing high-interest debt or building financial literacy.

-

Anticipating Resistance: With many Canadians facing similar challenges, you can proactively address common objections before they arise, improving client engagement and decision-making.

These statistics allow you to become a more compassionate, realistic, and effective advisor—one who doesn’t just sell products but builds sustainable, trust-based client relationships.

Maintaining a Budget

Image generated using the prompt “Show a client who feels overwhelmed with managing their money,” sourced from OpenAI, 2025.

Students taking this course understand the importance of having a budget. According to Investopedia, a budget helps create financial stability. Plus, following a budget ensures that bills are paid on time, an emergency fund can be established and clients can account for their other savings needs (Bell, 2022).

Nonetheless, 51% of Canadians do not have a budget. When asked why, Canadians cited a wide range of reasons for not having a budget including:

- not having enough time for it or find budgeting boring (9%)

- feeling overwhelmed at the idea of managing money (6%)

- not being responsible for financial matters in their household or preferring not to know about their finances (4%)

- preferred not to say (5%) (Financial Consumer Agency of Canada, 2019).

Recognizing that your clients may fall into one of these categories can be concerning. However, it does present as an opportunity for you to educate your clients, and help them overcome the challenges they face when managing their money.

Retirement Savings

According to the FCAC survey, 69% of Canadians who have not yet retired are preparing for retirement. Canadians are either doing this independently or with a pension through their employer. This statistic is an improvement, as the percentage of people preparing for retirement has increased from 66% in 2014 (Financial Consumer Agency of Canada, 2015). This is good news! Awareness surrounding saving for retirement is improving, and Canadians see that planning for their retirement is necessary. You should recognize, though, that roughly 31% of Canadians do not have a retirement plan, and these individuals are likely feeling uncertain and overwhelmed regarding their retirement (Financial Consumer Agency of Canada, 2019). If your client has no plan for retirement, you should approach this topic carefully and determine the level of knowledge they have on the subject. You should work with the client; educate them on the importance of saving for retirement and help them see it as a goal they can achieve.

Emergency Fund

Image generated using the prompt “Create an image that represents an emergency fund,” sourced from OpenAI, 2025.

According to an article on Wealthsimple, the standard amount of funds that a client should have in an emergency savings fund should be 3 to 6 months worth of your household income. However, new economic pressures now have advisors saying 8 to 12 months (Goldman, 2021). The FCAC study results indicated that 64% of Canadians have emergency funds for three months worth of expenses, and 65% of Canadians are confident that they could come up with an additional $2,000 if needed.

This statement needs to be considered on a case-by-case basis. If you have a client who has paid off their mortgage and has minimal bills, they are more likely to come up with that additional $2,000. A client who is a retired senior and on a fixed income is much less likely to be able to find the additional funds needed. Having an emergency fund is correlated to those Canadians that have a budget; 65% of budgets have an emergency account (Financial Consumer Agency of Canada, 2019).

Where Do Clients Get Their Advice?

Eventually, as we seek to understand our clients, we begin to see why financial advisors are needed, and why clients are often hesitant to commit and may object when a proposed solution is presented to them. The FCAC survey provides some food for thought for advisors — where are Canadians going to get their financial advice?

- 49% of Canadians seek financial advice from a financial advisor/planner

- 41% seek advice from their bank

- 39% seek advice from family and friends

- 33% do internet research

- 15% get information from print media

- 10% get information from radio or television programs (Financial Consumer Agency of Canada, 2019).

The above information is valuable. Advisors need to know where their clients are gathering information from as this allows them to correct any incorrect or misinformation that the client may have come to learn.

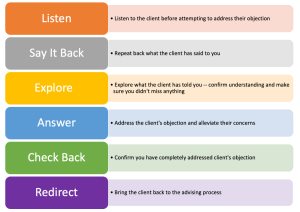

The Process for Handling Objections

Having an approach to objections can assist the advisor in ensuring that you are addressing the correct issue that the client is concerned with. This objection handling process will take you through the steps to overcome and resolve the client underlying concerns.

[Figure 7.1] Objection-handling process. (Created by: Professor Carla Van Horne, NAIT)

Listen

Image generated using the prompt “Create an image that shows someone listening to their client,” sourced from OpenAI, 2025.

Say It Back to the Client

When you are sure the client is done talking, look thoughtful for a moment and then repeat back what he has said. Saying something like, “I see you’re concerned about tying up the equity in your home,” is fine. This both shows that you were listening and allows the client a chance to clarify. The key here is to wait and allow the client time to share the concerns they are bringing to your attention. Maybe you missed something in explaining how the product or service will work or even how the process will work.

Image generated using the prompt “Create an image that shows an advisor saying it back to the client,” sourced from OpenAI, 2025.

Explore for Reasoning

Sometimes the client’s first objection isn’t their real concern. For example, many clients will use the objection that the cost is too high, but perhaps the client doesn’t understand what the product and/or service is and how it truly can benefit them. It is possible they object because you missed some vital information. Clarification is important for you to ensure you are listening to what your client is saying.

Image generated using the prompt “Create an image that shows an advisor exploring for reasoning,” sourced from OpenAI, 2025.

Answer the Objection

Image generated using the prompt “Create an image that shows an advisor answering the objection,” sourced from OpenAI, 2025.

Check Back with the Client

Redirect the Conversation

The Next Steps (Closing)

Asking to Proceed to the Next Step (Close)

Common Client Objections and How to Overcome Them

1. It is not the right time.

4. I need to speak to my spouse.

5. I already have an advisor.

6. I’m waiting until after the election.

7. Call me in a year.

8. You are new at this, or you are too young.

9. The stock market is too high.

10. The stock market is too low.

11. I am waiting for interest rates to go up.

12. You are too expensive.

Summary

REFERENCES

Media Attributions

- c7f3fc2b-f16c-47bc-be6a-04abfe70ceea

- 3fa30309-f83c-459b-94a5-d93544308bcf

- 6200c10d-47ff-4b7a-a67e-6df6bb88266b

- 63634b2f-9291-4a78-bf6e-36dd93ef0880

- OBJECTIONS2

- 7ccfce46-7ac7-4dff-a73e-d6f817c3db67

- 71ba64b5-ce43-4bfd-a078-bea61c3b8b47

- 58674bb5-a7d2-41d5-8c81-a54f323141a6

- Screenshot 2025-06-23 135013