8 Chapter 8: Building Rapport and Deepening Client Relationships

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- Explain the importance of relationship building in the client-advisor dynamic.

- Identify key elements of emotional intelligence that contribute to building trust and rapport.

- Demonstrate how effective communication, including active listening and empathy, strengthens relationships.

- Evaluate the ethical responsibilities involved in maintaining long-term client relationships.

- Apply relationship-focused strategies to foster client loyalty and sustained engagement.

.

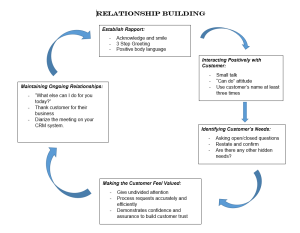

While emotional intelligence — including self-awareness and self-management — was explored in Chapter 6, this chapter shows how those skills are put into action during real client interactions. Previously, we established that relationship building is key to the overall success of a finance professional. In this chapter, we will walk through the Relationship Building Process (see the chart below) in greater detail and demonstrate how effective client communication is critical in assessing client needs.

[Figure 8.1] Relationship Building Chart. (Source: Professor Rosanna Anderson, NAIT)

Establish Rapport with a Client

When meeting with a client, the first step is to establish rapport. Rapport is defined as a close and harmonious relationship in which the people or groups understand each other’s feelings or ideas and communicate well (Oxford University Press, 2022). The definition of rapport clearly indicates that a relationship must exist for there to be rapport. Establishing rapport with a new client may commonly be overlooked, even though this step is one of the most crucial. What makes this step so important is that it influences the first impression.

Often, people begin a conversation to build rapport by discussing frivolous topics (e.g., the weather.) This is a flawed approach, as a conversation that begins superficially does not foster a true connection. It is also true that clients may be uncomfortable during this initial conversation and are eager to move on to more important topics.

As you approach your client, be amiable and acknowledge them. Three-steps to a successful greeting include:

- making eye contact — when eye contact is made the client knows you have seen them.

- using positive, open body language — no slouching and do not not turn your back on a client.

- taking your time — do not ambush the client as they walk in the door; give them time to come in and then greet them.

You should also choose a welcoming greeting, something more unique than the standard, “How are you today?” Some different options include:

- “What brings you in today?”

- “How can I help you?”

Moreover, if you know the client’s name, use it. Calling the client by name helps break the ice and allows for some common ground. Introduce yourself explain that you will be assisting them.

“My name is Tanya Redington. I am a financial advisor, and I will be working with you today.”

If the client’s name is difficult to pronounce, ask them how to pronounce it. Do not shorten their name to make it easier. It is much more respectful, and clients appreciate when their correct name is used.

Please read the following article titled 3 Strategies Financial Advisors Can Use to Build and Nurture Client Relationships

Share a meal

While sharing a meal can promote teamwork and collaboration, some may argue that it blurs the line between professional and personal boundaries. How can finance professionals maintain a balance between being personable and building strong relationships while still upholding a level of professionalism and confidentiality?

The article mentions that sharing a meal can help reduce perceptions of inequality and foster a sense of equality among individuals from different backgrounds. How can this aspect be relevant and beneficial when building rapport with diverse clients in the financial sector?

The article suggests inviting clients and their families for dinner as a way to enhance bonding. What are the potential benefits and challenges of including family members in client interactions? How can this practice influence the long-term nature of client relationships?

The F. O. R. D. method

The F.O.R.D. method emphasizes asking questions related to friends, occupation, recreation, and dreams. How can these specific topics help finance professionals gather valuable information about their clients’ financial goals and preferences? What kind of insights can be gained from discussing these areas?

Building trust is crucial in financial advisory relationships. How does the practice of disclosing similar information about yourself, as prompted by the F.O.R.D. method, contribute to creating a stronger bond with clients? Are there any potential risks or considerations in revealing personal details as a finance professional?

In some cultures, discussing personal matters can be considered intrusive or inappropriate. How can finance professionals navigate cultural differences and sensitivities when using the F.O.R.D. method to build rapport with clients? What strategies can be employed to ensure that clients feel comfortable and respected during such conversations?

Do you foresee any challenges using the FORD method (family, occupation, recreation, dreams) in your conversations?

Interacting Positively

When good rapport has been established with the client, moving on to the next step — interacting positively — is seamless.

You can engage in small talk, being sure to keep things light and high energy. Ask the client what they did over the weekend, or what plans they have for the next weekend. Clients like to talk about things that interest them or events they are looking forward to.

The client will likely tell you what they need, and what they feel the purpose of the meeting is. The best thing you can do is display a “can-do” attitude. A can-do attitude is characterized by a determination or willingness to take action and achieve (Oxford University Press, 2022). The client needs to know that they have come to the right person; someone who is prepared to assist them with their needs. It may happen that it is beyond your ability to assist the client with their need or request. When this happens, you can display your can-do attitude by finding the right person to assist the client and facilitate a warm handoff with the next finance professional.

As mentioned above, using the client’s name throughout the conversation helps foster the connection being built. Saying the client’s name three times in a conversation helps the client remember that you called them by their name.

Finally, and it can’t be said enough, listening is a critical conversational skill. It is important the client knows you are interested and paying attention to what is being said. As listening is such an important skill, we expand on this topic later in the chapter, focusing specifically on active listening.

Importance of Asking Questions in Client Conversations

A financial advisor who wants to build solid relationships with their clients understands that, in order to bring value to their clients, they need to know their clients’ challenges, problems, needs and overall perspective. Understanding their client’s point-of-view allows an advisor to customize solutions to the unique situations of a client. As was stated previously, clients often recognize they have a need, and that is what prompts them to ask for a meeting with their advisor. However, clients are rarely aware of what the best solution to their need or problem is. This is where the advisor (as the expert) can apply their knowledge to determine the best approach to the client’s financial situation.

An advisor who does this is helping solve their client’s problems and, therefore, providing superior value to their client. These types of positive, value-driven interactions are the building blocks for a long-term, mutually-beneficial relationship between advisor and client. It is important to not jump to a conclusion about a clients needs at this point of the conversation. Although there may be similarities between client situations, each situation is unique. Therefore, each solution needs to be customized and personalized with unique elements of the situation in mind.

Using the client’s name is essential at this stage of the relationship-building process and throughout the entire conversation. Seek first an understanding from the client as to their preference for how you are to refer to them. In previous chapters, it is vital to ensure we are respectful and pronouncing a client’s name correctly – this assists with putting the client at ease and is essential to helping build trust with the advisor.

Identify the Needs of a Customer/Client

Advisors use questioning strategies to derive the information that they are seeking from the client. In order for the Advisor to get to the root of the issue they will use questioning strategies as introduced previously. Closed-ended and Open-ended questions. We will explore questioning strategies that are useful at this stage as well as the skill of active listening. We will also look at how important empathy plays into the role of the conversation and how it helps the advisor have a more successful conversation.

Close-ended Questions

Close-ended questions are ones that require a very short answer (for example, multiple choice or yes/no questions.) Close-ended questions are useful when you need to know a specific piece of information rather than achieve a deeper understanding of an issue or perspective.

Some examples of close-ended questions are:

- Which package looks the best to you?

- Would you like to set up another meeting?

- Do you see how this will benefit you?

- Would you like to move forward and set up the account right now?

- How does that sound?

Which of the following best describes the purpose of close-ended questions in client interactions?

To delve deeper into an issue and achieve a better understanding of a client’s perspective.

To generate lengthy responses and encourage detailed discussion.

To obtain specific pieces of information and help make decisions more quickly.

To explore a client’s emotional responses and personal experiences.

Open-ended Questions

Open-ended questions are designed to elicit longer responses, and they often involve using words like what, how and why as part of the questions. Using open-ended questions to learn more about what is occurring in your client’s life will help you capture more information and inform you of what the true issue is so you can determine what the best solution may be. For example, a client may be coming to see you about a mortgage for home renovations. During this meeting, you learn of other capital needs the client has or see that the client has cash flow issues due to multiple credit cards and/or loans or lease payments. This may lead you to recommend a solution that can alleviate the greater problems your client is experiencing.

Some examples of open-ended questions are:

- Can you tell me about some of the challenges you are currently facing?

- Tell me about how you like to do your banking?

- What plans do you have for your retirement?

- How is your mortgage working for you?

- What renovation plans do you have for your home?

What is the main purpose of using open-ended questions in client interactions?

To limit the client’s response to a simple ‘yes’ or ‘no’

To encourage the client to give brief responses

To capture more information and gain deeper understanding of the client’s situation

To quickly steer the conversation towards a pre-determined conclusion

Questions Helps Determine Value

When using the questioning strategies described above to determine the client’s root issue, it is critical to receive permission to ask questions. Proper questioning elicits the information necessary to assess whether the solutions offered by your institution provide value to the client. These solutions should address pressing needs, solve problems, provide opportunities, or help overcome challenges. If there is no value or fit between the problem and solution, an ethical advisor should not try to make a sale. Remember, the only thing worse than no sale is a bad sale. A bad sale brings no value to the buying organization, forces an advisor to be unethical and can damage the reputation of both the advisor and the advisor’s financial institution.

T/F Open-ended questions lead to a deeper understanding than close-ended questions.

Active Listening

Image generated using the prompt “Create an image of a financial advisor meeting with a client where it demonstrates active listening,” sourced from OpenAI, 2025.

There is another side that comes into play when asking questions — being able to truly and actively listen to the responses. In personal relationships and social situations, listening is a great trait to have but not an essential requirement. People don’t expect you to retain everything they say and are fairly satisfied if they are allowed to speak without excessive interruption. Consequently, in social situations, most people will listen to respond not listen to understand. Poor advisors have the same tendency.

In advising conversations, listening is essential if you are going to develop a complete understanding of the client’s perspective and the current situation surrounding the client’s financial situation. There are a variety of reasons why people struggle with listening. For one, it is cognitively difficult. It takes concentration and commitment and requires the listener to focus completely on the person with whom they are communicating. Also, people tend to focus on themselves and what they are going to say when the other person stops talking. This human inclination can take on an extreme form; when a person is so focused on what they are going to say that they interrupt the person speaking and don’t let them finish.

In addition, to truly listen to understand, you (as the advisor) need to be able to be able to put your own perceptions and truths aside and focus on the prospective client’s perceptions and truths. This is why the concept of empathy, or the ability to understand and sense other people’s emotions and thoughts, is so important (empathy is discussed in more detail later in this chapter). If you are able to gain an understanding of the client’s perspective by being empathetic, you will be able to present information using the client’s “language.” This is much more persuasive than using your own “language.” People who listen are also more likable. Listening is a way to show a genuine desire and curiosity to learn more about the speaker, demonstrate respect for the speaker and honor the speaker’s psychological need to be heard.

Active listening (listening to understand) allows you to tailor your follow-up questions based on what you have heard. Later, when presenting the solution to the client, there will be a high degree of customization. A customized solution not only makes your message more relevant, it also demonstrates that you were carefully and respectfully listening when the client was speaking.

People also communicate nonverbally (through body language); therefore, active listening also involves observing and reading (listening to) body language. This can give you an even richer understanding of the words spoken and their underlying meaning. During the discovery stage, it is important to observe your client’s body language to discern their level of comfort with the questions being asked and determine if they understand what is being discussed. The client, when engaged, should be leaning in to the conversation, nodding their head in agreement and focusing on what the advisor is saying. If the client is leaning back in their chair, looking at their watch or looking at the door, there is a good chance the client is disengaged from the conversation. To re-engage the client, it may be best to ask a closed-ended question or to confirm understanding by restating and verifying the information gathered (paraphrasing). You need to be cognizant of a client’s time, and you should periodically check-in to ensure that the client has the time to continue the conversation. Rescheduling the meeting for another day may be a better option.

Image generated using the prompt “Create an image of a financial professional assisting a client demonstrating good body language of leaning in.” sourced from OpenAI, 2025.

An advisor’s goal should always be to persuade a client to want to work with them. In order for that to be achieved, you need to be an empathetic, active listener who is focused on helping your customer.

Active listening is not something one can improve through practice. tf

Active listening does not only involve listening but also speaking. TF

What is Empathy?

Empathy is defined as the ability to understand and share the feelings of another (Oxford University Press, 2022). In the content that follows, we examine why empathy matters, not only with our clients but with our colleagues and co-workers. Before continuing, take a moment to watch the following video, to obtain additional insight into why empathy is important.

How Does an Advisor Show Empathy with Clients?

Earlier chapters discussed how individuals have emotional attachments to their financial situations. A client’s financial situation can have both positive and negative implications throughout their lives. Life experiences, such as childbirth, marriage, divorce, loss of employment and death, can impact a client’s emotions and significantly affect their financial situation. A good financial advisor can display empathy at the right moment, even if they has not experienced these life challenges themselves. Working with clients during difficult times, and listening and responding with empathy, can lead to future gains in the client/advisor relationship. You should look to yourself to see what level of empathy you have and investigate how you can build on this skill.

Using empathetic questions requires you to 1) truly hear the client and 2) for the client to truly feel heard. More often, you will need to use empathetic statements and responses to what a client says, and these responses help show the client that you understand their feelings. Following are examples of empathetic questions you can ask and empathic responses you can give during client conversations.

Questions you can ask:

- What financial decisions make you feel uncomfortable?

- When have your instincts let you down when it comes to investing?

- Can you share with me how you previous banking experience is impacted you personally, so I can better support you and tailor our financial conversation accordingly?”

Responses you can give:

- I am sorry that happened to you.

- That would upset me too.

- I want to thank you for being so open and honest with me.

- This sort of challenge is never easy.

- It is clear this has impacted you deeply.

- What else would you like to share?

- It sounds like you had a very stressful time.

- Yes, what happened makes no sense at all.

- I am on your side.

- It’s no surprise you are upset.

- That sounds frightening.

- You are making complete sense.

One final thing to note about empathy, while empathic questions are important and can be helpful, they should not dominate your meetings.

How Empathetic are You? Click on the link to take an Empathy Quiz (Greater Good Magazine).

Identification of Needs

The reason financial advisors need to be highly skilled at asking questions and active listening is because their goal is to identify needs and understand the client’s perspective. It is common to discover that your client is struggling with their financial situation and determine that their situation can be simplified by recommending an alternative product or service.

For example:

You learn your client is not able to contribute to their registered retirement saving plan (RRSP) because they have a number of monthly payments to credit cards and loans. Knowing this, you can investigate the option of consolidating the client’s debts to free up cash flow, giving them savings that could be contributed to their RRSP.

Benefits Statements

In the example above, when presenting your solution to the client, you should focus on the features that illustrate the benefit of simplifying the process and connect that benefit to the client’s current struggle. The likelihood is high that the client will recognize the value in being able to continue to pay their debts while also being able to contribute to their retirement savings.

Benefit statements are one way you can connect the client’s struggles to the solutions you are presenting; solutions that will help solve the client’s issues. These statements reinforce to the client “what is in it for them.” Remember, benefit statements are only effective if you match them up to the client’s specific needs or wants. If you don’t first take the time to collect that information, you will simply be shooting in the dark.

- Peace of Mind

- Save your Money

- Grow your Money

- Convenience

- Flexibility

- Save Time

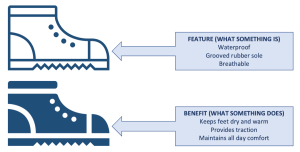

Features and Benefits

There are times when an advisor may confuse a feature of a product/service with a benefit of the product/service. It is important to discern between the two, as it helps you communicate and sell a solution to the client. To be clear, a feature of a product/service is what it is, and a benefit is what it does for the client.

[Figure 8.2] Features versus benefits.

[Figure 8.2] Features versus benefits.

Funnel Approach

-

relevant facts questions

-

problem/challenge questions

-

follow-up questions

-

paraphrase and pre-commit questions.

-

How can I assist you today?

-

Can you tell me about what brings you in today?

-

What challenges are you currently facing in meeting your retirement goals?

-

What are some of the major issues with meeting your cash flow needs?

-

Can you tell me more about your plan for retirement? How much income do you think you will need to live comfortably?

-

Would you walk me through your monthly budget in more detail?

-

Paraphrase: To summarize, you are facing this pretty significant challenge with respect to achieving your retirement goals, and you also would benefit from a better way to manage cash flow needs?

-

Pre-commitment: If I can show you some solutions we offer at NAITLAB Financial that could help you achieve your retirement goals and make it easier to manage your cash flow would that be of interest to you?

-

The questioning and active listening processes are enhanced when an advisor momentarily abandons his/her own opinions and assumptions. It is important for the advisor to not jump to conclusions to quickly – assuming the solution too soon.

-

When a client makes a statement, it’s important to be able to confirm, clarify, and/or get a deeper understanding. When participating in sales conversations, the active part of listening is to respond to client’s answers with clarifying questions (when appropriate) or by restating or paraphrasing what is said.

-

By clarifying or restating/paraphrasing, an advisor can be confident that the sales conversation is defined by clear communication and mutual understanding.

Making the Client Feel Valued

Image generated using the prompt “Create an image of a client showing that they are feeling valued.” sourced from OpenAI, 2025.

The probability of selling to an existing client is 60-70%, whereas for a new client it is 5-20% (Mansfield, 2016).

Undivided Attention

-

Silence your devices. Your phone, tablet and computer can be distracting, and distractions can have an impact on the success of the meeting.

-

Close down most of the browsers on your computer. Only keep windows that pertain to your client open on the screen. This practice will also ensure the privacy of your other clients’ information.

-

Face the clients you are meeting. If you have more than one client, attempt to look at both of them throughout the meeting. Even if one person dominates the conversation, it is vital to include everyone present.

-

Provide entertainment for children. If your clients bring their child to the meeting, and the child has nothing to do, it is helpful to have a colouring book and crayons/markers on hand. Not only will this keep the child occupied, the parents will appreciate the consideration you have shown their child. If the child becomes upset and is taking attention away from the meeting, it may be advisable to offer to reschedule for a better time. Alternatively, you can offer to meet the clients in their home.

-

Listen before you speak. This has been mentioned before, but this serves as an important reminder. Take notes if needed; this is a good way to not miss out on critical information. Make sure you first ask your clients if they will permit you to take notes. Repeat to the client what you heard. This will reassure the client that you are listening, and they have been understood.

Process Requests Accurately and Efficiently

-

Pay attention to detail. Financial matters can and will be complicated. Ensure that you follow appropriate guidelines and do not rush a request; you can be efficient without rushing. Often, when a person rushes, they cut corners and mistakes occur. You need to be meticulous and organized with your work. Essential details to stay on top of are: dates, capital requests and deadlines.

-

Confirm your understanding of your client’s request by restating and confirming. Often, clients will be overwhelmed and may provide incorrect information. It is the your responsibility to be cognizant of when the client has provided incorrect information and repeat the correct information back in a way that is not patronizing to the client.

-

Document your steps. It is good practice to document your work. Documentation provides you with a file that accounts for the work that has taken place. Documentation in a client file is helpful for future client dealings or when a file has been pulled for audit purposes. The file shows the auditor what the advisor did, and as an audits can occur years after the work has taken place, the documented notes in the file can act as a good reminder for you. Documentation is also helpful when there is a customer dispute — you will have proof of the work you did.

Demonstrate Confidence and Assurance to continue to Build Customer Trust

Making the Recommendation

Closing Philosophy and Mindset

When a Client is Not Ready to Commit

-

“I’m not sure that will work.”

-

“The interest rate/fees is higher than I thought it would be.”

-

“Your timeline does not work for us.”

-

“I don’t see the advantage of going with your solution.”

-

They ask questions. “My brother-in-law got his mortgage a few weeks ago at ABC bank, and his banker charged him a higher rate from what you are offering?”

-

They ask another person’s opinion (such as a family member or friend.) “This seems interesting. I would like to run it by my father if that is ok?”

-

They relax and become more friendly.

-

The read over any brochure material you have provided.

-

“What do you think about what we’ve discussed so far?”

-

“Do you see how this will help you achieve your financial goals?”

-

“I am sorry that your brother-in-law received a higher rate. The rate I am offering you is based on your long relationship with our institution. We reward loyalty! Can I confirm that rate today?

Presenting the Solution

The Use of Visual Aids/Tools

Image generated using the prompt “Create an image of financial advisor using visual aids in their presentation. (Open AI, 2025)

Client Involvement

Maintaining Ongoing Relationships

-

Thank you for trusting me with your mortgage today! Please let me know how else I can make this experience as enjoyable as possible.

-

Thank you for your business! We truly appreciate you and look forward to seeing you again.

-

I know that you could have chosen many other financial institutions to set up your investment accounts. Thank you for choosing us!

-

Thank you, Mr. Bing, for seeing me today to process your RRSP contribution. I look forward to seeing you again to discuss setting up your children’s RESP accounts.

-

We take pride in your business with us. Thank you!

Diarize the Meeting

Summary

REFERENCES

Media Attributions

- Relationship chart UPD

- Financial_Advisor_Active_Listening_Realistic

- Bank_Teller_Active_Listening_Realistic

- Screen Shot 2022-04-26 at 11.49.42 AM

- Client_Feeling_Valued_Realistic

- Advisor_Using_Visual_Aids