Financial Planning

Personal financial planning is a process that individuals use to manage their finances to achieve their financial goals and ensure long-term financial security. This comprehensive approach involves evaluating one’s current financial situation, setting realistic financial goals, and devising strategies to achieve these goals. The process is ongoing and requires regular review and adjustment to adapt to changes in financial circumstances, life stages, and economic conditions.

Financial planning requires you to address several questions, some of them relatively simple:

- What’s my annual income?

- How much debt do I have, and what are my monthly payments on that debt?

Others will require some investigation and calculation:

- What’s the value of my assets?

- How can I best budget my annual income?

Still, others will require some forethought and forecasting:

- How much wealth can I expect to accumulate during my working lifetime?

- How much money will I need when I retire?

The Financial Planning Life Cycle

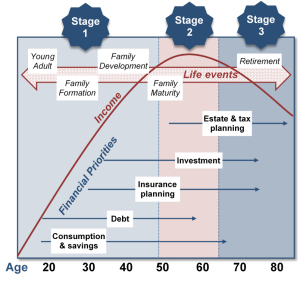

Another question that you might ask yourself—and certainly would do if you worked with a professional in financial planning—is: “How will my financial plans change throughout my life?” The figure below illustrates the financial life cycle of a typical individual—one whose financial outlook and likely outcomes are probably a lot like yours. [1] As you can see, our diagram divides this individual’s life into three stages, each of which is characterized by different life events (such as beginning a family, buying a home, planning an estate, and retiring).

At each stage, there are recommended changes in the focus of the individual’s financial planning:

- Stage 1 focuses on building wealth.

. - Stage 2 shifts the focus to the process of preserving and increasing wealth that one has accumulated and continues to accumulate.

. - Stage 3 turns the focus to the process of living on (and, if possible, continuing to grow) one’s saved wealth after retirement.

At each stage, of course, complications can set in—changes in such conditions as marital or employment status or the overall economic outlook, for example. Finally, as you can also see, your financial needs will probably peak somewhere in stage 2, at approximately age fifty-five, or ten years before the typical retirement age.

Figure 9.2: The Financial Planning Life Cycle

Choosing a Career

Until you’re on your own and working, you’re probably living on your parents’ wealth right now. In our hypothetical life cycle, financial planning begins in the individual’s early twenties. If that seems like rushing things, consider a basic fact of life: this is the age at which you’ll be choosing your career—not only the sort of work you want to do during your prime income-generating years but also the kind of lifestyle you want to live. What about college? Most readers of this book, of course, have decided to go to college. If you haven’t yet decided, you need to know that college is an extremely good investment of both money and time.

The figure below summarizes the most recent, 2015, findings from Statistics Canada. [2] A quick review shows that people who graduate from high school can expect to enjoy average annual earnings of just under $50,000, and those who go on to finish college can expect to generate 17 percent more annual income than high school graduates who didn’t attend college. With better access to health care—and, studies show, with better dietary and health practices—college graduates will also live longer. And so will their children.) [3]

| Education | Average Income: Canadian Women | Average Income: Canadian Men |

| High school diploma | $43,254 | $55,774 |

| College/university diploma | $48,599 | $67,965 |

| Bachelor’s degree | $68,342 | $82,082 |

What about the student loan debt that so many people accumulate? At an average cost of $27,000 (the average amount of debt accumulated by post-secondary students upon graduation) and an average increase in earnings of $263,000 over an average work-life expectancy of 30 years, you would need to invest that $27,000 for 30 years at an average annual rate of return of 8%. [4] At that rate of return, you should be able to pay off your student loans (unless, of course, you fail to practice reasonable financial planning).

Naturally, there are exceptions to these average outcomes. You’ll find some college graduates stocking shelves at 7-Eleven, and you’ll find college dropouts running multibillion-dollar enterprises. Microsoft co-founder Bill Gates dropped out of college after two years, as did his founding partner, Paul Allen. Though exceptions to rules (and average outcomes) certainly can be found, they fall far short of disproving them: in entrepreneurship as in most other walks of adult life, the better your education, the more promising your financial future. One expert in the field puts the case for the average person bluntly: educational credentials “are about being employable, becoming a legitimate candidate for a job with a future. They are about climbing out of the dead-end job market”. [5]

Bringing Down Those Monthly Bills

So to be able to practice reasonable financial planning you must first be able to identify how you can bring down your monthly bills. If you want to take a gradual approach, one financial planner suggests that you perform the following “exercises” for one week: [6]

- Keep a written record of everything you spend and total it at week’s end.

- Keep all your ATM receipts and count up the fees.

- Take $100 out of the bank and don’t spend a penny more.

- Avoid gourmet coffee shops.

You’ll probably be surprised at how much of your money can quickly become somebody else’s money. If, for example, you spend $3 every day for one cup of coffee at a coffee shop, you’re laying out nearly $1,100 a year just for coffee. If you use your ATM card at a bank other than your own, you’ll probably be charged a fee that can be as high as $3. The average person pays more than $60 a year in ATM fees. If you withdraw cash from an ATM twice a week, you could be racking up $300 in annual fees. [7] Another idea – eat out as a reward, not as a rule. A sandwich or leftovers from home can be just as tasty and can save you $6 to $10 a day, even more than our number for coffee! In 2013, the website DailyWorth asked three women to try to cut their spending in half. After tracking her spending, one participant discovered that she had spent $175 eating out in just one week; do that for a year and you’d spend over $9,000! [8] If you think your cable bill is too high, consider alternatives like Playstation Vue or Sling. Changing channels is a bit different, but the savings can be substantial.

The Latte Factor is actually trademarked by financial guru David Bach. He and other financial advisors recommend that everyone calculate her/his latte factor. He even developed a calculator that shows how much money, over time, you could save by cutting out a small, unnecessary thing from your daily/weekly expenses. Even if you assume a low interest rate e.g., 1%, the savings add up. Find your latte factor!

You may or may not be among the Canadian consumers who purchased more than 3 billion cans, 2 billion bottles, and 40 million kegs of beer, in 2016 alone, or purchased one or more of the over 2 billion Tim Hortons coffees sold each year. You may not be one of the 37% percent of Canadian consumers who regret spending outside of your means. [9] Bottom line – if, at age twenty-eight, you have a good education and a good job, a $60,000 income, and $70,000 in debt—by no means an implausible scenario—there’s a very good reason why you should think hard about controlling your debt: your level of indebtedness will be a key factor in your ability—or inability—to reach your longer-term financial goals, such as home ownership, a dream trip, and, perhaps most importantly, a reasonably comfortable retirement.

One of the best ways to manage your money and personal finances is to build a personal budget.

Personal Budget

You will need to have all your information gathered. This includes what you bring in – from employment to student loans – and what goes out – for food, entertainment, health and wellness, rent, utilities, etc. Be honest and thorough.

The Government of Canada, through the Financial Agency of Canada, created a tool that provides an in-depth account of your personal finances. Use the Budget Calculator to document your situation. Export your budget as an Excel spreadsheet. You will now be able to make improvements, if appropriate. If your balance is negative, or when your expenses exceed your income, you need to make some choices based on what you learned when you tracked your spending. Ask yourself some tough questions:

- What can be eliminated from my expenses?

- What can be reduced from my expenses?

- In what areas can I be a smarter consumer?

- Where does my money seem to get gobbled up?

After you have made some difficult choices, turn back to the budget worksheet and create a new “revised” column. You will want to work toward achieving a positive balance.

Should you end up with a surplus or positive balance, you need to make some choices about what to do with the extra money. Perhaps you could put it toward your financial S.M.A.R.T. goal. Avoid the temptation to spend it.

Financial Tip

When you think about budgeting, it’s important to look beyond balancing expenses against income in the short term. Be sure to include savings for an emergency fund and for future needs like ongoing education, mortgage, etc.

Savings should always be part of your budget. Small savings add up fast and can be there for emergencies or unexpected expenses.

Building a Good Credit Rating

So, you may or may not have a financial problem. According to the quick test you took, do you splurge? Are your bills too high for your income? If you get in over your head and can’t make your loan or rent payments on time, you risk hurting your credit rating—your ability to borrow in the future.

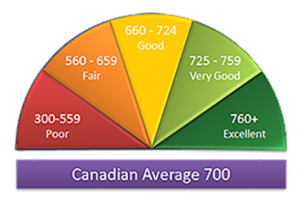

How do potential lenders decide whether you’re a good or bad credit risk? If you’re a poor credit risk, how does this affect your ability to borrow, or the rate of interest you have to pay? Whenever you use credit, those from whom you borrow (retailers, credit card companies, banks) provide information on your debt and payment habits to two national credit bureaus: Equifax, and TransUnion. The credit bureaus use the information to compile a numerical credit score, called a FICO score; it ranges from 300 to 900, with the majority of people falling in the 600–700 range. In compiling the score, the credit bureaus consider five criteria: However, the main factors that are used to calculate your score include:

- Payment history

- Use of available credit

- Length of credit history

- Number of inquiries

- Types of credit

The credit bureaus share their score and other information about your credit history with their subscribers. [10]

So what does this do for you? It depends. If you pay your bills on time and don’t borrow too heavily, you’d likely have a high FICO score and lenders would like you, probably giving you reasonable interest rates on the loans you requested. But if your FICO score is low, lenders won’t likely lend you money (or would lend it to you at high interest rates). A low FICO score can even affect your chances of renting an apartment or landing a particular job. So you must do everything possible to earn and maintain a high credit score.

Figure 9.3: Credit Score Ranges

As a young person, though, how do you build a credit history that will give you a high FICO score? Based on feedback from several financial experts, Emily Starbuck Gerson and Jeremy Simon of CreditCards.com compiled the following list of ways students can build good credit. [11]

- Become an authorized user on a parent’s account.

- Obtain your own credit card.

- Get the right card for you.

- Use the credit card for occasional, small purchases.

- Avoid big-ticket buys, except in case of emergency.

- Pay off your balance each month.

- Pay all your other bills on time.

- Don’t cosign for your friends.

- Don’t apply for several credit cards at one time.

- Use student loans for education expenses only, and pay on time.

If you meet the qualifications to obtain your own credit card, look for a card with a low-interest rate and no annual fee.

A Few More Words About Debt

What should you do to turn things around—to start getting out of debt? According to many experts, you need to take two steps:

- Cut up your credit cards and start living on a cash-only basis.

- Do whatever you can to bring down your monthly bills.

Although credit cards can be an important way to build a credit rating, many people simply lack the financial discipline to handle them well. If you see yourself in that statement, then moving to a pay-as-you-go basis, i.e., cash or debit card only, may be for you. Be honest with yourself; if you can’t handle credit, then don’t use it.

More Information

To understand more about the credit analysis lenders will perform when deciding to approve a new loan or credit card, check out this article by Investopedia: Understanding the Five Cs of Credit.

Build Your Emergency Fund

An emergency fund is a pool of readily accessible money set aside to cover unexpected expenses that could arise due to unforeseen circumstances. These situations can range from job loss, medical emergencies, urgent car repairs, or unexpected home maintenance costs, among others. The primary purpose of an emergency fund is to provide financial security by creating a safety net that can be used to cover living expenses if income is disrupted or large, unexpected costs arise.

An emergency fund is a pool of readily accessible money set aside to cover unexpected expenses that could arise due to unforeseen circumstances. These situations can range from job loss, medical emergencies, urgent car repairs, or unexpected home maintenance costs, among others. The primary purpose of an emergency fund is to provide financial security by creating a safety net that can be used to cover living expenses if income is disrupted or large, unexpected costs arise.

Having an emergency fund can help alleviate stress during a crisis by providing the needed funds without having to rely on credit cards, high-interest loans, or other borrowing methods that can lead to long-term debt. Without an emergency fund, people often resort to these types of costly debts when confronted with an unexpected financial burden, which can exacerbate financial strain and lead to a debt cycle that is hard to break free from.

The recommended size of an emergency fund can vary depending on an individual’s circumstances. However, a commonly suggested guideline is to save enough to cover 3 to 6 months of living expenses. It’s important to remember that an emergency fund is not built overnight. Instead, it’s generally built up slowly over time as part of a regular savings plan. Once the fund reaches the target size, it’s typically maintained at that level, with any withdrawals for emergencies replaced as soon as possible.

In essence, an emergency fund serves as a financial buffer against life’s uncertainties, providing a level of financial security and peace of mind. It is an essential component of sound financial management and should be a priority in personal finance planning.

More Information

You can find a free online budgeting tool on the FCAC website and other tools in the Canadian Financial Literacy Database. Go to Canada.ca/financial-tools, then click on Budget Planner.

- Gallager T. J., & and Andrews, J. D. Jr., (2003). Financial Management: Principles and Practice, 3rd ed. Upper Saddle River, NJ: Prentice Hall. p. 34, 196. ↵

- Statistics Canada, Table 1 “Median annual earnings of women and men aged 25 to 64 who worked full time and full year as paid employees, by highest level of education and province or territory, 2015.” Retrieved from https://www12.statcan.gc.ca/census-recensement/2016/as-sa/98-200-x/2016024/98-200-x2016024-eng.cfm ↵

- Hansen, K. (2016). “What Good is a College Education Anyway? The Value of a College Education.” Retrieved from: https://www.livecareer.com/quintessential/college-education-value ↵

- Hansen, K. (2016). “What Good is a College Education Anyway? The Value of a College Education.” Retrieved from: https://www.livecareer.com/quintessential/college-education-value ↵

- Hansen, K. (2016). “What Good is a College Education Anyway? The Value of a College Education.” Retrieved from: https://www.livecareer.com/quintessential/college-education-value ↵

- USA Today (2005). “Exercise 1: Start small, watch progress grow.” Retrieved from: http://usatoday30.usatoday.com/money/perfi/basics/2005-04-14-financial-diet-excercise1_x.htm ↵

- Fetterman, M. (2005). “You’ll be amazed once you fix the leak in your wallet.” Retrieved from: http://usatoday30.usatoday.com/money/perfi/basics/2005-04-14-financial-diet-little-things_x.htm ↵

- Ramnarace, C. (2013). “Could you cut your spending in half?” Retrieved from: https://www.dailyworth.com/posts/2046-could-you-cut-your-spending-in-half/2 ↵

- Arrington, M. (2008). “Ebay Survey Says Americans Buy Crap They Don’t Want.” Retrieved from: https://techcrunch.com/2008/08/21/ebay-survey-says-americans-buy-crap-they-dont-want/ ↵

- Robertson, C. (2015). “Credit Score Range – Where Do You Fit In?” Retrieved from: http://www.thetruthaboutcreditcards.com/credit-score-range/. ↵

- Gerson, E. S., & Simon, J. M. (2016). “10 Ways Students Can Build Good Credit.” Retrieved from: http://www.creditcards.com/credit-card-news/help/10-ways-students-get-good-credit-6000.php ↵

A process that individuals use to manage their finances with the aim of achieving their financial goals and ensuring long-term financial security.

A pool of readily accessible money set aside to cover unexpected expenses that could arise due to unforeseen circumstances.