9 Chapter 8 – Commercial Credit

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- the four different types of business entities in Canada.

- the intricacies of commercial credit and how it differs from consumer credit.

- the five Cs of commercial credit.

- the importance of financial analysis in commercial credit.

- the different types of ratios used by commercial lenders.

Types of Business Entities in Canada

A lender has to understand how the business entities that exist within Canada differ. How a business is organized has implications on its opportunities and borrowing needs. The lender may be able to guide and advise their client when they are deciding which form of ownership is best suited for them.

There are four forms of business ownership in Canada:

- Sole Proprietorship

- Partnership

- Corporation

- Cooperative

(Note: We will be focusing on the first three forms of business ownership. Cooperatives are often funded internally and rely on other sources outside of a financial institution.)

It is likely that these business entities have been explained in other courses. In this course, we will approach these business entities from a lender’s perspective.

Why do we care about the form of the business entity we are lending to?

- Each form has distinct tax and liability provisions for the owners.

- These provisions result in different credit structures and credit-risk reduction methods.

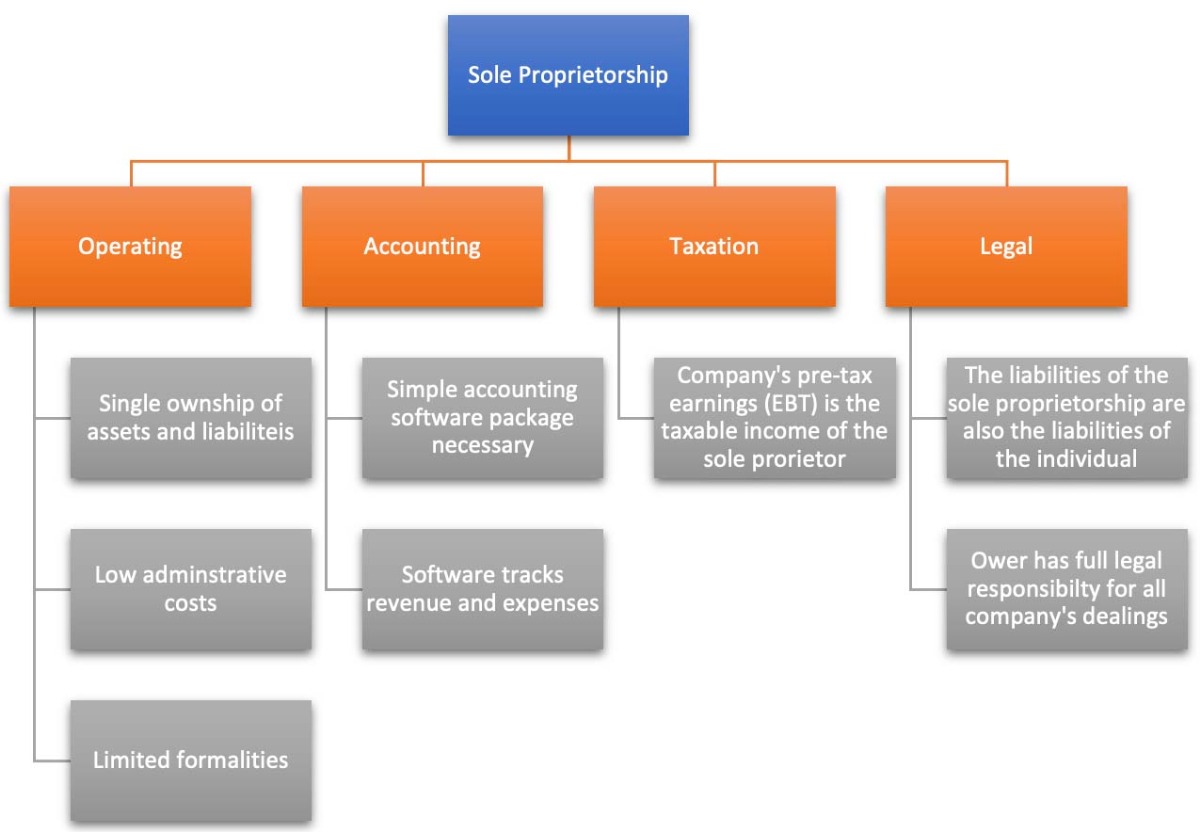

Sole Proprietorship

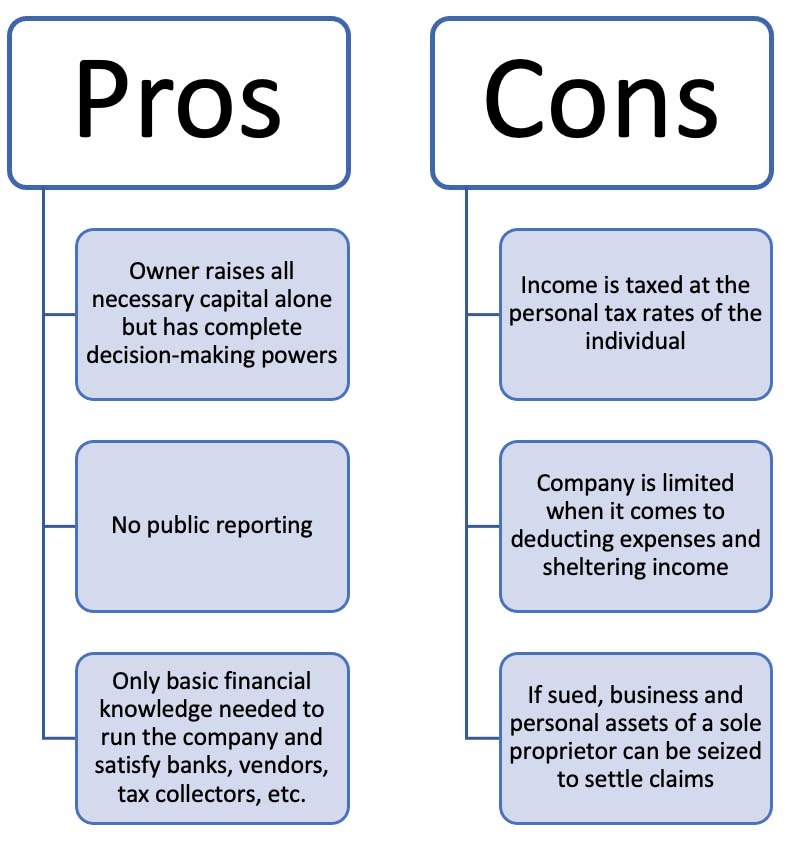

Many small businesses start as a sole proprietorship, and there are many reasons for a business to choose this option. The main benefit to registering a business as a sole proprietorship is the cost—it is inexpensive. Sole proprietorship is also flexible; there is less documentation required for setup. The flexibility of the structure also offers a higher degree of control, which allows for faster decisions, making it is easier to take advantage of opportunities as they arise. The tax filing process is simplified for a sole proprietor as well.

Proprietorship is the simplest way a business can be structured. For a business to become a sole proprietorship, the owner needs to (bdc, 2022):

- register a trade name;

- obtain a tax number; and

- open a bank account.

[Figure 8.2] Features of a sole proprietorship.

[Figure 8.2] Features of a sole proprietorship.

According to Farber, a licensed insolvency trustee headquartered in Toronto, 15% of start-ups fail in their first year, and only 50% make it to their fifth year (Farber, 2022). Other concerns that face sole proprietors are the following:

- the owner’s personal assets are at risk—a creditor can collect from the owner’s personal assets; and

- there is there is typically a lack of management skills.

A way to address the first risk is to ensure that sufficient personal assets exist and that the principal/owner has disability and life insurance (which may require tax returns and personal and business financials).

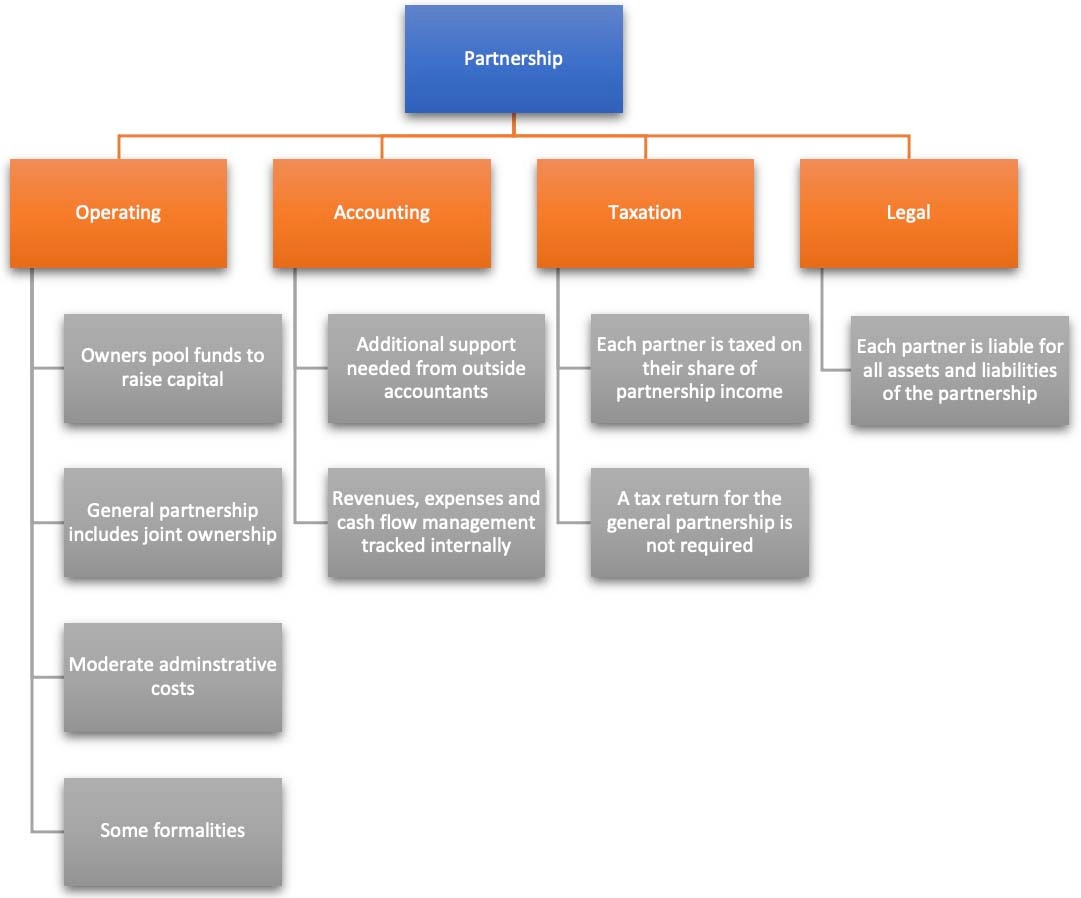

Partnership

A partnership is a business that two or more owners establish. Like sole proprietorships, partnerships are relatively simple and inexpensive to form (bdc, 2022). Advantages for the owners are that they can pool their assets and skills to help start their business right. To establish a partnership, the owners need to do the following:

- register a trade name;

- obtain a tax number; and

- open a bank account.

Owners will typically work out a partnership agreement that outlines the ownership shares, capital contributions, and the percentage of ownership and decision-making powers each will have. In this written agreement, the following would be accounted for:

|

the amount of investment from each partner |

|

the division of management responsibilities |

|

the limitations and conditions for withdrawal of cash |

|

the division of loss and/or profit |

|

the provisions regarding admission and withdrawal of partnerships |

Lenders will need a copy of this agreement so they can determine how it will impact their lending decisions and risk mitigation.

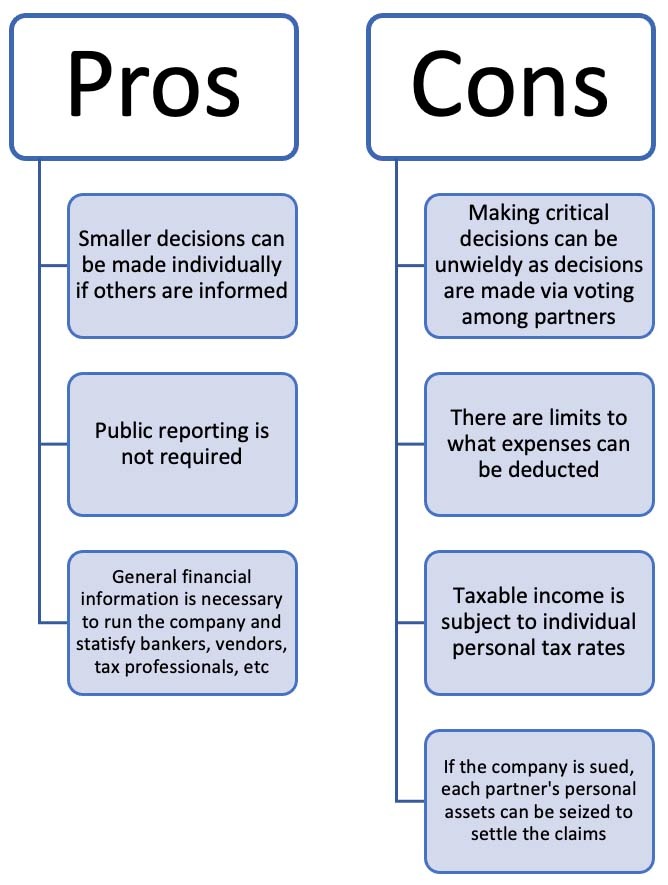

Some negative aspects of a partnership include the following:

- creditors can collect from partners’ assets;

- partners are jointly and severally liable for debts;

- it is the most likely business entity to dissolve;

- the is an immediate dissolution of if one partner dies; and

- partners may pass the buck to each other on decision-making.

According to the Local Government Chronicle, 70% of partnerships fail to deliver their intended outcomes. The key drivers of this high rate of failure are a lack of trust and deteriorating relationships (LGC Contributor, 2008). A lender may advise their clients to consider incorporation as their clients’ business grows.

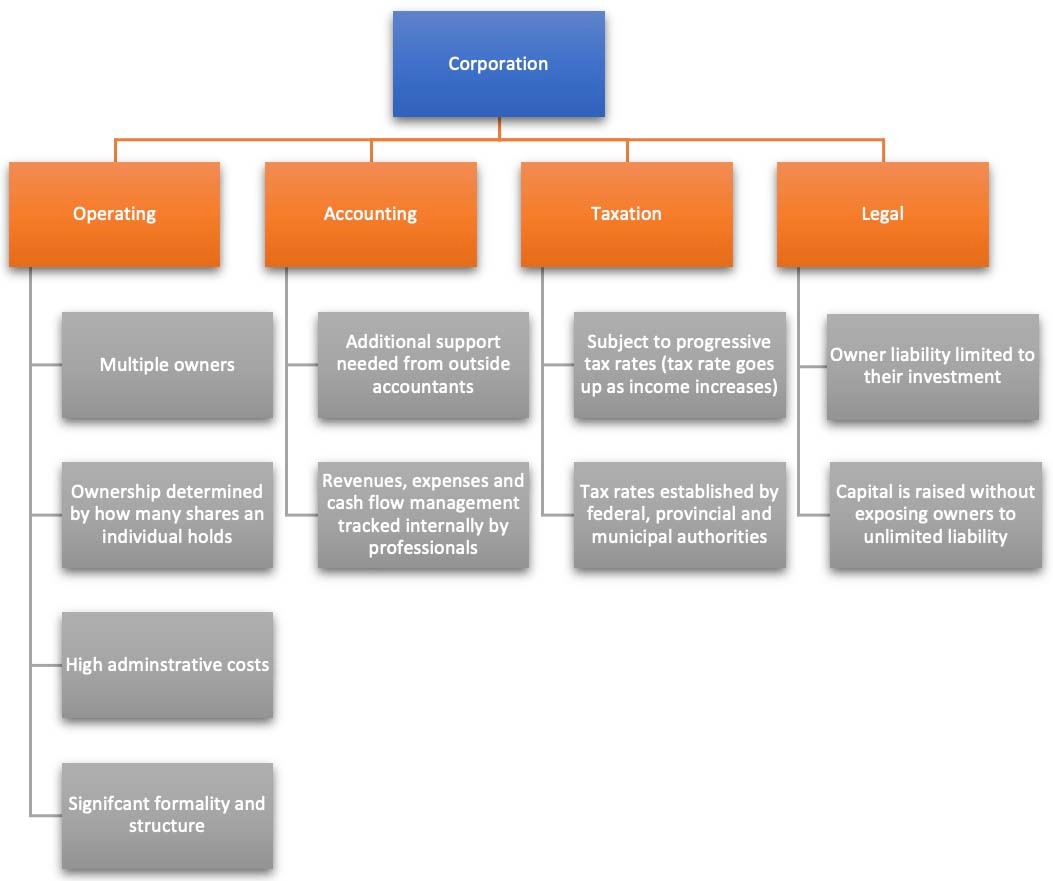

Corporation.

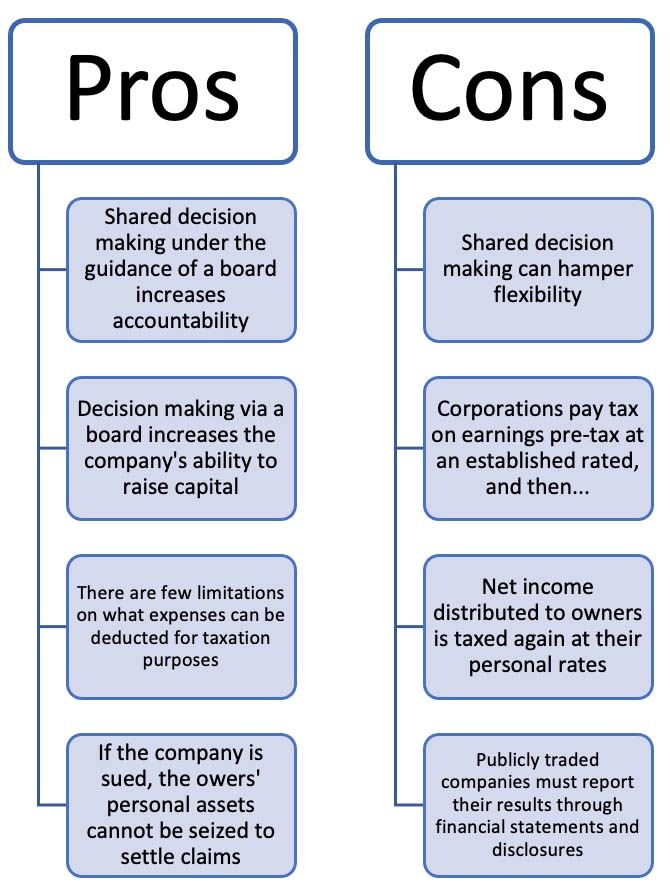

A corporation is a separate legal entity. It has the ability to enter into contracts in its name and be distinctly separated from its owners. Corporations can raise large amounts of capital more easily than a sole proprietor or partnership (Government of Canada, 2022). The process for setting up a corporation is expensive and complex. Entrepreneurs should work with an accountant and a corporate lawyer when establishing their corporation. In Canada, a corporation is created when one or more entrepreneurs register a business provincially or federally through the filing of the articles of incorporation. The articles of incorporation describe the business and its purposes and list the officers, directors, and the bylaws (bdc, 2022).

Corporations have unlimited lives and can, in theory, exist forever. When the owner dies, the company can continue on without issue. Owners’ personal assets are not at risk like they are in a sole proprietorship or partnership, and creditors can only seek payment from the assets of the corporation (bdc, 2022).

The main benefit of forming a corporation is the protection it provides from creditors; however, the costs to establish a corporation are often a hindrance to new, start-up business. Lenders need to be prepared to advise their clients on the best options and refer them to a corporate lawyer as needed.

Types of Business Activities

Why do you need to know what a client’s business does? The lender needs to identify if there are possible restrictions on lending, applicable to certain types of businesses, due to the nature of the entity (government) or its level of risk (casino or amusement park). Plus, understanding what a business does may influence the loan structure.

Types of businesses include the following:

- manufacturing;

- wholesaling;

- retailing;

- service; and

- other (e.g., agriculture, mining, construction).

The type of business the client is involved in will impact the type of loan required, the level of risk, and the repayment schedule of the loan.

Commercial Credit: Financing for a Business

Commercial credit (or lending) is when a bank/financial institution lends funds to a business to help that business with its capital funding needs. In most cases, collateral is required (e.g., property or equipment) for commercial lending. Collateral helps to mitigate risk in the event a bank cannot collect if the business declares bankruptcy. Future cash flows from future accounts receivable can be taken as collateral if needed.

Commercial credit is contingent on the company’s viability. Banks want to see progression in a company’s long-term plans and feel confident that their debt will be repaid. Commercial lending often involves more parties and more signing authorities, and all have a say in the business and the taking on of debt. When a significant number of people are involved in the decision-making process for a business, there is often less personal contact between lender and client. The lender will need to determine the best contact method (the one also preferred by the client) so timely communication can occur. The entire process (from start to finish) of a commercial credit file can be lengthy. A lender needs to collect the information needed without having to go back to the client multiple times. Given that the lender will likely have less contact with the client, waiting for information can impede the entire loan process.

The structure of the debt in commercial lending could be lending a lump sum repaid in scheduled installments, and the debt is usually self-liquidating. Depending on the needs of the business, the term of the loan(s) could be short or long. Short-term funding needs could be for operational costs or to purchase equipment to facilitate business operations.

Step 1: Screen against loan policy. The lender needs to determine whether the request for capital is within the scope of the financial institution’s lending parameters. If the request is suitable and meets the parameters of the financial institution, the lender can continue.

Step 2: Gather data (e.g., financials, business plan, forecasts). The lender requests access to financial statements from the client; at a minimum, three years of statements are required. It is preferred that these statements are audited. Depending on the request, the lender may also ask for a business plan. A business plan helps the lender and financial institution determine how serious the business is about the request they are making. Financial forecasts are often requested. The financial institution is looking to see how this request for capital could potentially be realized and when the debt can be repaid.

Step 3: Analyze financial data. This involves a financial ratio analysis, which will be covered later in this chapter.

Step 4: Complete financial risk, management risk, and market risk assessments. These assessments are a continuation of the previous step but will often go further. They involve the lender interviewing key people within the organization.

Step 5: Build projections or analyze projections. The lender reviews the projections provided to check for accuracy. There are situations where the lender will be required to build projections.

Step 6: Identify risk mitigation strategies. The lender seeks out any risk concerns and determines the risk can be mitigated by collateral.

Step 7: Determine pricing. This varies from financial institution to financial institution. Usually, the lender and financial institution will consider the strength of the client, the assets being pledged as collateral, and the purpose of the request when they are determining pricing for the debt.

Types of Commercial Loans

Commercial loans are often considered to be a short-term source of funding for business needs. Some financial institutions will offer renewable loans that may end up being extended indefinitely (Kenton, 2020). During the renewable period, the business is required to produce the needed documentation to ascertain their ability to continue carrying the debt load. Examples of these types of capital requests include the following:

- purchase of assets which will result in sales, then cash (i.e., machinery and equipment, a manufacturing plant, another company [assets are always taken as security]); and

- finance receivables (or inventory) to even out/bridge cash flow (accounts receivables or inventory is security).

The key is to identify the real reason the business needs the loan. The real reason is not always the reason given by the client. For example, a client requests a “working capital” loan to meet payroll. The lender investigates and finds that the problem is not a temporary cash shortage but is actually slow collections. The lender will need to find out why this is occurring and determine if it is on-going or temporary.

Questions to Ask

- Is there any policy restricting the stated loan purpose?

- Is the loan purpose to finance an illegal activity?

- What is the real loan purpose?

- How long is the trading cycle? Changed?

- What is the financing gap? (ACP + DSI – APP)

Should the borrower address these issues, the chances are that the loan would indeed be paid in record time.

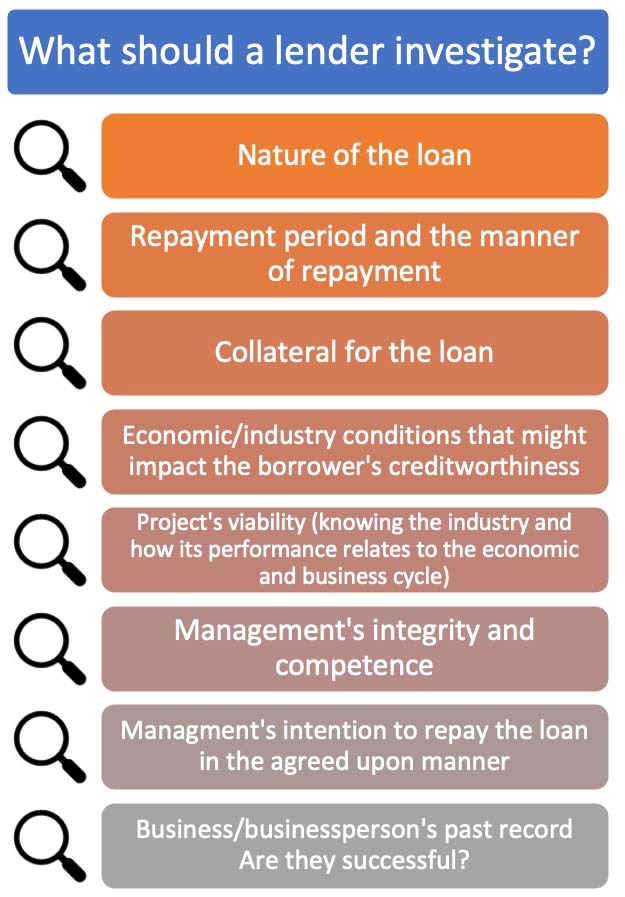

The Five Cs Analysis

The five Cs of credit assist the lender in determining a client’s creditworthiness . This goal is to determine the likelihood of default based on the information available at the time of application. The five Cs is one of the tools the lender can use to determine the risk and balance against the needs of the client and the financial institution. The list of Cs for commercial credit is different from what is seen with consumer credit in Chapter 3. The lender needs to distinguish between the different types of clients when lending.

Character

Character forms the foundation of a management risk assessment. Here, the lender seeks to establish the borrower’s reputation for repaying debts. Does the borrower demonstrate a willingness to honour its obligations? Look at their repayment history and credit record. Some questions the lender should ask to establish character are:

- Does the company have ethical business practices?

- Is the company willing to provide information?

- What is the company’s profit retention history?

- Does the company have a dividend policy?

- Does company have justifiable compensation for management/owners?

- Are there signs of trouble? This can include misleading advertising/pricing, frequent change of suppliers, fires, and labour problems.

Remember, the character of a small, privately held company may come from the character of the principals.

Capacity

Capacity is part of both the management risk assessment and the financial risk assessment. The lender seeks to determine the borrower’s financial ability to pay their debts when due. A review would be required in which the lender reviews the business’s financials to determine its profitability and long-term viability. This includes doing a historical review and reviewing forecast statements that the business provides. Some questions the lender should ask are to establish capacity are the following:

- What is the capacity of the business to repay any new debt?

- What is the capacity of the business itself to get paid?

- What is the capacity of the business to receive and absorb payments?

- What is the capacity of the financial institution to expose themselves to extending credit to this business?

The lender will also need to consider the intangibles of the business. This includes things such as the experience and training the business owners have in their business/industry. How long have they been in business? This dive into the business will include looking at their knowledge and experience with financials, marketing, production, and purchasing. Moreover, the staff and the location of the business is critical. Are they able to maintain staffing levels or are there concerns surrounding staff turnover? Is the business located in an area that lends to itself to a successful business? Or is the business in an area cut off from shipping routes? Capacity also seeks to see how the business has handled challenges in the past. Are they innovative and willing to take on new technology?

Capital

Capital looks at a business’s long-term financial strength to repay their debt. Does the business owner(s) invest in their own business? The lender looks at the balance sheet to see the current position and makeup of the business’s debt structure. How are they currently managing to pay their debts? The lender reviews the business’s level of working capital, net worth, and cash flow. This helps the lender ascertain the financial viability of the business’s debt structure. Does the business have the ability to take on more debt? Furthermore, where does this new capital request fit in with the overall debt structure?

Audited financials are preferred and often required by financial institutions, and, if needed, the lender may contact the accountant who prepared the financials. The challenge of reviewing financials is that the lender is trying to determine a business’s future ability to pay. Combining all the Cs of credit is critical to help determine whether approval is warranted.

Collateral

In some cases, collateral helps mitigate risk in a credit deal, or it can provide an incentive for the borrower to repay their debt. In business lending, some collateral is required. Having collateral will help mitigate risk and help establish the business’s future ability to pay. Typically, in commercial lending, the pledge of an asset (e.g., real estate or equipment) is necessary to satisfy the collateral requirement. Appraisals may be required to determine the value of an asset being pledged for collateral.

Conditions

Conditions refer to the external conditions that could impacted the business the lender is analyzing. Are there any systemic or environmental issues that the business faces or could face? For example, when considering a logging business, an environmental impact could be the recent increase in forest fires. How is the business structured to handle such situations? Lenders also need to consider the economic impacts that a business can experience. How does the business’s management overcome these situations? Government actions are another consideration. If the government mandates specific legislation, what are the implications to the business? Conditions explore how well a company can cope with change and how change could impede their ability to pay their bills.

Financial Analysis

Financial analysis helps evaluate the performance of a business and potentially identify problems (bdc, 2022). Analysis provides the lender with more information so they can make a better credit decision and establish the degree of risk associated with granting credit to a customer. Financial analysis also helps answer the five Cs of credit.

Financial Statements

When obtaining a business’s financial statements, the lender should request three years of statements. The lender should receive the following:

- the balance sheet;

- the statement of earnings (income statement);

- the statement of retained earnings; and

- the statement of cash flows.

The lender can request/obtain the financial statements from the customer, from a trade reporting agency, and, if company is publicly traded, statements are readily available on their website. Banks can demand financial statements, but trade creditors cannot. An analysis of a business’s financial statements is only one facet of credit analysis and may raise more questions than provide answers.

Some key takeaways to remember about financial statements are the following:

- Financial statements do not predict the future.

- Three years of statements are necessary to determine trends.

- Statements should be audited for fraud.

- It can be tough to obtain financial statements.

- Statements should be centered around generally accepted accounting principles (GAAP) (Kenton, 2022).

Types of Financial Statement Analysis

Financial statement analysis is the process of analyzing a company’s financial statements for decision-making purposes (Kenton, 2022). There are different types of analysis, including the following:

- Simple analysis. This involves the analysis of one set of statements.

- Comparative analysis. This involves the analysis of two sets of statements or one set and industry ratios.

- Trend analysis. This involves the analysis of three or more sets of statements.

- Comparative trend analysis. This involves the analysis of trends for a customer compared to the trends for the industry.

Lenders use certain standards to ascertain what the results of the analysis indicate. They use ratios from one or more previous periods, industry standards, and rule of thumb to come to a conclusion about the results they observed.

Ratio Analysis

Classification of Ratios Used by Lenders

Liquidity

Liquidity ratios provide the lender with information on how quickly a business is able to pay its debts (Hayes, 2021). These ratios are a good indicator of how well a company can cover their expenses. They help lenders determine how quickly a business can generate cash to purchase assets and repay their creditors.

Profitability

Profitability ratios essentially seek to determine whether a business can make profit. A business then uses these profits to repay their debts—again a focus for a lender.

Solvency

Solvency ratios are used to determine how well a business is managing their debt obligations. Lenders view these ratios to determine how a business is using long-term debt to support the business.

Activity Ratios

Activity ratios can indicate the efficiency of a business and how clients are leveraging their assets on the balance sheet to generate sales and cash.

Liquidity Ratios

Can a business meet its current obligations? (This indicates the availability of ready cash.)

Current Ratio = Current Assets/Current Liabilities

- 2:1 preferred

- if low, a company may not be able to pay its debts

- if high, inefficient use of resources

- business should always have more current assets than current liabilities

Quick Ratio = Current Assets – Inventory/Current Liabilities

- also known as the ACID TEST ratio

- 1:1 is preferred

- if low, a company may not be able to pay debts

- if high, inefficient use of resources

- identifies any risk of potential cash flow problems

Working Capital = Current Assets – Current Liabilities

- Working capital is used to measure a business’s ability to generate cash to pay for its short-term financial obligations.

- Positive working capital indicates that a business has the ability to meet their monthly obligations.

- Negative working capital is a concern; the business will likely have difficulty meeting their monthly obligations.

Profitability Ratios

Is the company profitable?

Net Profit Margin = Net Income/Net Sales * 100 (expressed as a percentage)

- If low, the business may not be profitable after paying its operating expenses.

- If high, this is better unless prices for the product or service are too high and reduce sales.

Return on Investments (or ROA) = Net Income/Total Assets (expressed as a percentage)

- varies by industry

- If low, may be due to poor performance; check income statements items.

- the higher, the better

Return on Equity (or Return on Shareholders Equity) = Net Income/Equity (expressed as a percentage)

- Ratio should be greater than prevailing interest rates.

- If low, may be due to poor performance; check income statement items.

- the higher, the better

Activity Ratios

How is the company being run?

Accounts Receivable Days Sales Outstanding = Account Receivable * 365 Days/Sales

*also known as Average Collection Period (ACP)

- Should be slightly higher than the terms of sale; not exceeding 1.5 times.

- if low, strong control of receivables

- if high, poor control of receivables or deliberate acceptance of higher risk accounts

Inventory Turnover = Cost of Good Sold/Inventory

- Inventory turnover rates vary greatly by industry.

- if low, poor control, possible obsolete stock or over buying

- if high, maintaining insufficient stock; could have poor buying procedures or have been cut off by suppliers; if there is significant variance to industry averages, this indicates too much or not enough investment in inventory.

Solvency Ratios

What is the contribution of the owners? What is the company’s reliance on short- and long-term debt?

Average Days Payable Ratio = Accounts Payable * 365 Days/Cost of Sales (or COGS)

- Total should be close to the industry’s average terms; not exceeding 1.5 times.

- If low, the enterprise may be on COD terms with suppliers or paying early (discounts).

- If high, the enterprise is paying beyond term; there is a danger that suppliers will refuse to offer credit if this is excessive.

Debt to Asset Ratio = Total Liabilities/(Current Assets + Fixed Assets) (expressed as a percentage)

- indicates the percentage of a business’s assets financed by creditors

- low ratio is a good indicator that a company is able to pay its debts or take on new opportunities

- high ratio indicates dependence on debt and could indicate financial weakness

Debt to Equity Ratio = Total Liabilities/Shareholders Equity

- Measures the amount of debt a business is carrying compared to the amount invested by its owners.

- If low, it is a strong company; easy to borrow/lend.

- If high, it is highly leveraged and risky; may have high interest rate expense; difficult to borrow/lend.

Media Attributions

- image (33)

- image (34)

- image (35)

- ChatGPT Image Jun 26, 2025, 03_14_50 PM

- image (36)

- image (37)

- image (38)

- dcdf9845-bddc-43fd-b2a2-1376ae27f404