8 Chapter 7 – Bankruptcy

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- default and the signs that can indicate a client is not financially stable.

- the different parties involved in the bankruptcy process.

- the criteria an individual must meet to declare bankruptcy.

- what assets are non-exempt from bankruptcy and what debts still must be paid.

- the advantages and disadvantages of declaring bankruptcy.

- how to calculate surplus income.

- the alternative options to bankruptcy and the advantages and disadvantages of each.

Risk of Default

While lenders do their best to ensure that each credit application is of sound quality, there are times when a client, for one reason or another, does not fulfill their obligations to the lender and defaults on their loan. There is a process that exists for this type of client, and understanding this process will help a lender remain cognizant of the fact that there is always the potential for a deal to go wrong. In addition, the lender should be aware of what options are available for the client in this type of situation, and the lender should help the client develop a plan to address it.

There are signs that can indicate an individual is experiencing challenges with their financial situation (see the list below). If these challenges are caught early, the lender can provide credit counselling to the client and help them avoid bankruptcy.

|

Client is using credit to create income. |

|

Client is making only their minimum payments. |

|

Client indulges in impulse buying (look at their bank statements for patterns). |

|

Client has no savings or has no money before payday. |

|

Client requests loan consolidations often. |

|

Client is not sure of their monthly expenses. |

|

Client has employment problems. |

|

Client has a substance abuse problem. |

|

Client has a problem with compulsive spending. |

|

Client has an issue with gambling. |

|

Client is facing medical problems. |

|

Client is financing their education. |

|

Client is dealing with a breakdown in their marriage. |

|

Client is involved in lawsuits. |

|

Client has a history of bad investments. |

|

Client fails to pay income tax on self-employed earnings. |

Credit counselling is an option for a client who still has the ability to pay but is overwhelmed by high interest rates. If the lender is not equipped to provide credit counselling, they can recommend another financial advisor or other credit counselling organizations to the client.

Bankruptcy

An individual should only consider bankruptcy after they have tried every debt management option available to them. If these options do not work, then seeking out a licensed insolvency trustee (LIT) would be the next step. An LIT will advise the individual about the effects of filing for bankruptcy and explain all the possible options. A lender should have a good understanding of bankruptcy and be able to support their client when and if the time to file bankruptcy arrives.

To understand how bankruptcy works, it is important to learn about the different parties that are involved in the bankruptcy process. Two important terms that will be used throughout this section are debtor and bankrupt.

Representatives of the Bankruptcy and Insolvency Act

(Plus Other Roles Involved in the Bankruptcy Process)

Office of the Superintendent of Bankruptcy Canada

The Office of the Superintendent of Bankruptcy Canada (OSB) is responsible for overseeing all matters for which the Bankruptcy and Insolvency Act (BIA) applies as well as certain issues relating to the Companies’ Creditors Arrangement Act (CCAA). The OSB licenses and regulates the insolvency profession. It also oversees estates in bankruptcy, the reorganizations of commercial organizations, consumer proposals, and receiverships (Office of the Superintendent of Bankruptcy Canada, 2018).

Official Receiver

An official receiver is a federal government employee, specifically in the OSB. They are appointed by Governor in Council. This role has many responsibilities, including accepting all documents that are filed in proposals and bankruptcies. The official receiver also examines bankrupts under oath and will chair the meetings of the creditors (Office of the Superintendent of Bankruptcy Canada, 2015).

Registrar in Bankruptcy

The registrar in bankruptcy is a court official who has a judicial role in bankruptcy court on discharge hearings, bankruptcy and insolvency-related motions, and examinations of the debtors, creditors, and any other parties involved in insolvency matters (Rumanek & Company Ltd, 2022).

Licensed Insolvency Trustee (LIT)

An LIT is a federally regulated professional who provides advice and services to individuals and businesses in Canada who are experiencing debt problems (Office of the Superintendent of Bankruptcy Canada, 2016). The trustee notifies creditors of bankruptcy assignments and will collect, review, and approve submitted claims. Throughout the bankruptcy period, the trustee will collect payments, ensuring that the debtor fulfills their requirements. The trustee also distributes funds to the creditors. An LIT has a fiduciary duty and is obligated by the BIA to act honestly and in good faith; they are bound to the established code of ethics for LITs.

Inspector

An inspector is appointed by the creditors and represents the interests of the creditors during the administration of the bankrupt’s estate. An inspector also has a fiduciary duty and performs their duties impartially and in the interest of the creditors. An inspector will give direction to the LIT regarding any required actions that need to be taken in the handling of the bankrupt’s estate. The inspector also oversees the LIT’s administration to ensure that the LIT acts in accordance with their direction.

Creditors

There are three types of creditors: secured, unsecured, and preferred. Creditors are to participate in and vote at the meetings of the creditors. They have a duty to appoint an inspector and can also serve as an inspector. A creditor informs the LIT of any irregularities that are seen on the part of the debtor of the bankrupt.

Debtor

The debtor owes money and has been assigned or petitioned into bankruptcy, or they filed a proposal.

How Does an Individual Qualify for Bankruptcy?

To qualify for bankruptcy, an individual must meet the following criteria (Bankruptcy Canada, 2022):

- owes a debt of at least $1000 (minimum);

- the value of the debts exceeds the value of assets; and

- they are unable to pay debts as they come due.

Once the LIT has filed bankruptcy, creditors are barred from contacting the individual. For the debtor, this provides relief from the hassle of dealing with collection calls, legal actions, and garnishment of wages, along with making payments on most debts.

The LIT will prepare and file any outstanding tax returns up until the date of bankruptcy. Any outstanding balances and/or penalties will be included in the bankruptcy filing. An individual’s income tax refunds are considered assets to the bankrupt’s estate.

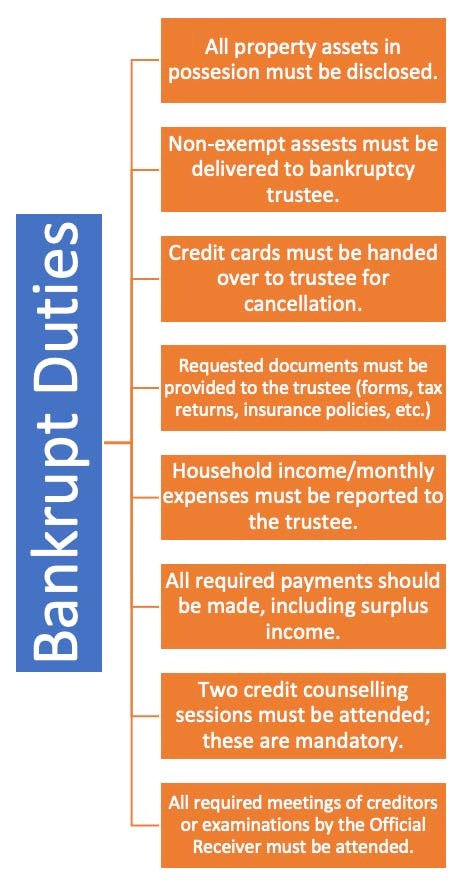

The bankrupt is obligated to fulfill all their requirements to eventually be discharged from bankruptcy.

[Figure 7.1] Requirements the bankrupt must satisfy to be discharged from bank.

Duties of the Bankrupt:

[Video 7.1] Duties of the bankrupt. (Source: Hoyes and Michalos/YouTube)

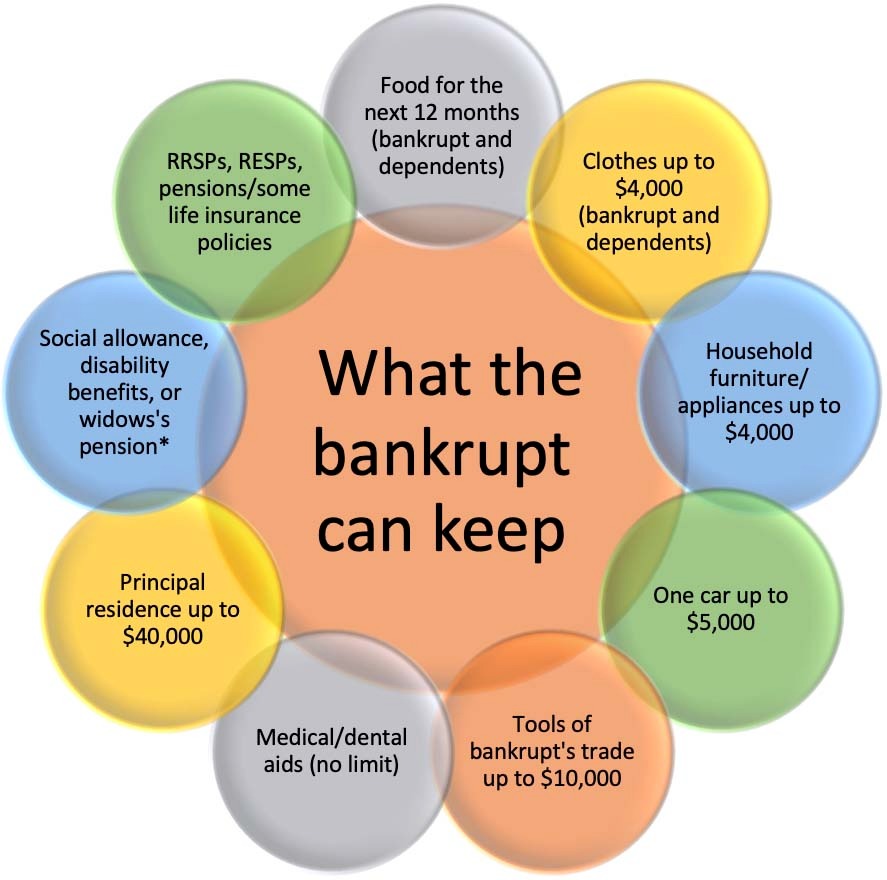

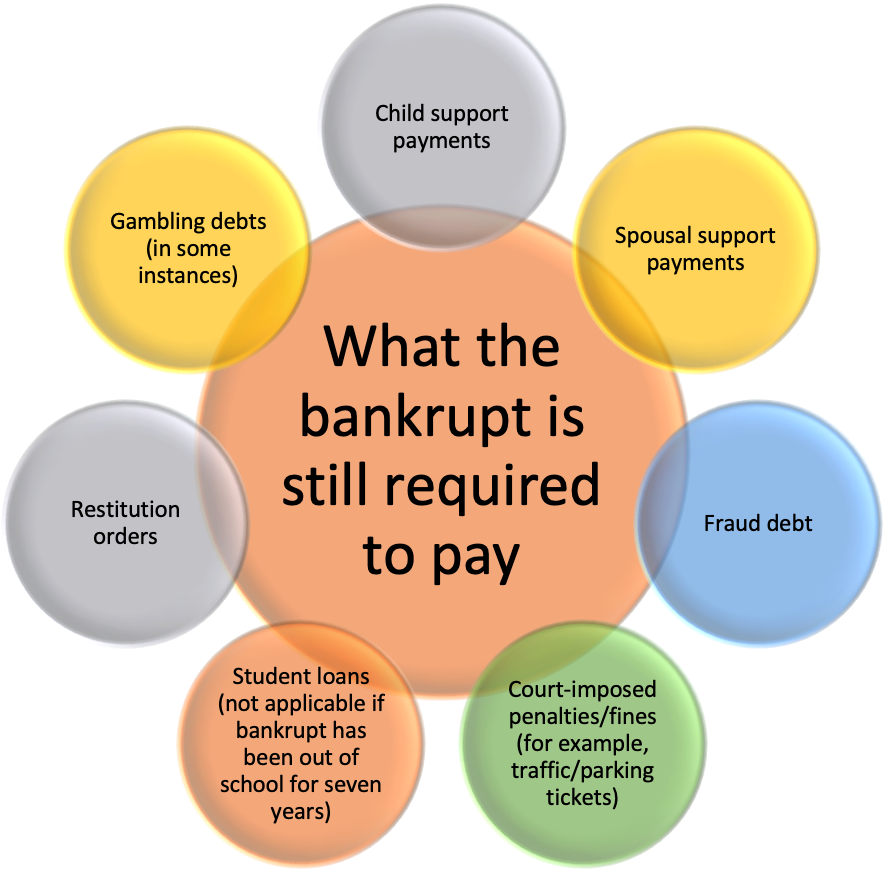

What the Bankrupt Can Keep and What They are Required to Pay

The bankrupts will have an R9 on their credit rating, and that will remain on their credit report for six years after they are discharged. While it will be difficult for the bankrupt to obtain credit in the future, it does not necessarily disqualify them.

Automatic Discharge

If the bankrupt meets all their requirements and obligations and there is no opposition to an automatic discharge, they will be granted one based on the following:

|

Automatic Discharge Period |

No Surplus Income |

Surplus Income |

|---|---|---|

|

First Time Bankrupt |

9 months |

21 months |

|

Second Time Bankrupt |

24 months |

36 months |

Advantages and Disadvantages of Bankruptcy

What are the advantages of bankruptcy?

It provides a bankrupt with legal protection from creditors. They will not face wage garnishments or judgements. It also wipes out the majority of an bankrupt’s unsecured debts (e.g., loans, credit card debt, etc.) With a first bankruptcy, it is common for an individual to be debt free within 9 to 12 months. The cost of filing for bankruptcy is rather low, notably when compared to the cost an individual would face if they had to continue paying their debts (Bankruptcy Canada, 2022).

What are the disadvantages of bankruptcy?

An bankrupt’s credit score will be lower for a minimum of six years from the time the bankruptcy is complete. Some assets may have to be surrendered. A portion of the bankrupt’s income (above a certain level) may be allocated toward their bankruptcy. The trustee must be provided with detailed information on the bankrupt’s income and expense information. An income tax refund, if received, is part of the bankruptcy. The refund will be forfeited to the trustee for the year of the bankruptcy (Bankruptcy Canada, 2022).

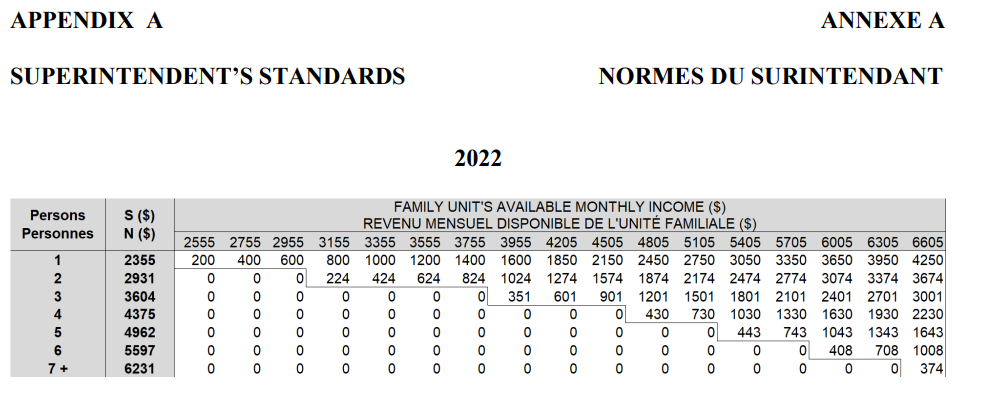

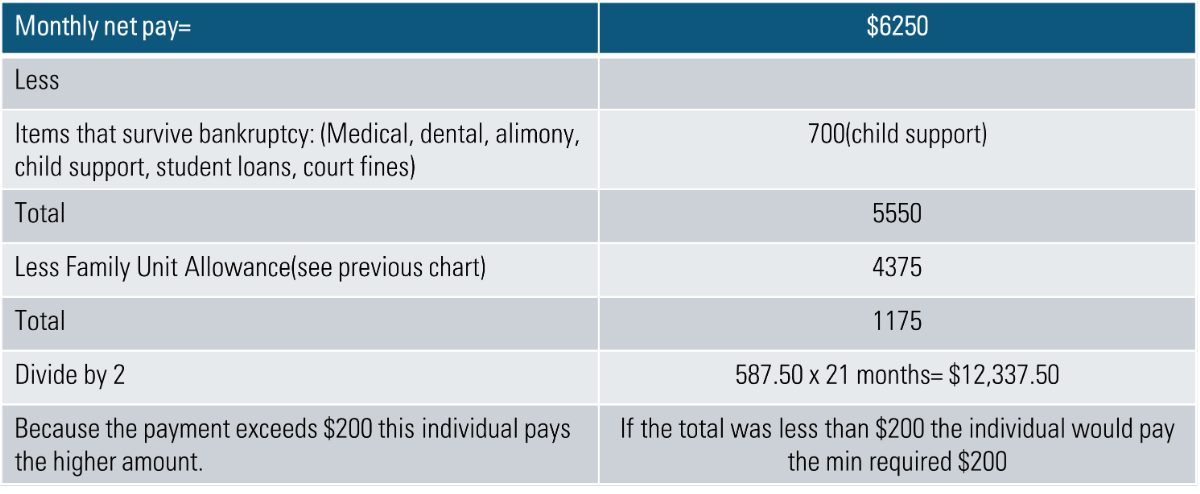

Determining Calculations for Surplus Income in Bankruptcy

The bankrupt is required to make as much restitution as possible for their failure to pay their debts. The OSB has established the Superintendent’s Standards, which are derived from the low-income cutoffs released by Statistics Canada (Office of the Superintendent of Bankruptcy Canada, 2020).

released by Statistics Canada (Office of the Superintendent of Bankruptcy Canada, 2020).

Calculation Examples

Note: The minimum payment required is $200/month that a bankrupt will need to pay. If there is surplus income, the bankrupt is required to pay the higher amount.

[Video 7.2] Surplus income explained. (Source: Innovation, Science and Economic Development Canada/YouTube)

Alternate Options to Bankruptcy

While bankruptcy can be an option for some individuals, it is important that a lender be knowledgeable about the other options that are available. In this course, we will focus on consumer proposals and orderly repayment of debts.

Consumer Proposals

Consumer proposals are one alternative option to bankruptcy for a person experiencing challenges meeting their debt obligations.

A consumer proposal is administered under Part III, Division I of the Bankruptcy and Insolvency Act (Justice Laws Website, 2022). It is an agreement made on behalf of the debtor and their creditors in which they settle the debts and create a schedule for repayment. Consumer proposals allow for lump sum payments to be applied; otherwise, the repayment term for the proposal is a maximum of five years.

In Alberta, for a debtor to be eligible for a consumer proposal, they must be incapable to make payments as they come due (for any reason), or they must stop making payments as they come due. They must owe their creditors less than $250,000. It is 500,000 for married couples. The amount of their assets must be insufficient to satisfy their debts, and they are required to hire a licensed bankruptcy trustee to mediate with their creditors on their behalf (Debt.ca, 2022).

Creditors must be in a better position than they would be if a debtor filed for bankruptcy. Creditors must be in agreement (of at least 51%) to support a consumer proposal. The consumer proposal will result in an R7 rating on the individual’s credit report and remain on the credit report for a maximum of five years.

|

The LIT will report any adverse change to the creditors. |

|

The LIT will assist the debtor in the preparation of the proposal. |

|

The LIT will provide a report and recommendation for the creditors on whether or not to accept the proposal. |

|

The LIT will collect amounts due from the debtor and pay dividends to creditors as per the proposal. |

|

Once the proposal is complete, the LIT will issue a certificate of full performance to the debtor and then apply for the trustee’s discharge. |

|

A complete list of all assets (property) and liabilities (debts) must be provided to the LIT. |

|

If a meeting is requested by the creditors, the debtor must attend the first meeting. |

|

The debtor should attend two counselling sessions. |

|

The debtor must notify the LIT, in writing, if their address changes. |

|

The debtor should aid the LIT in the administration of the proposal. |

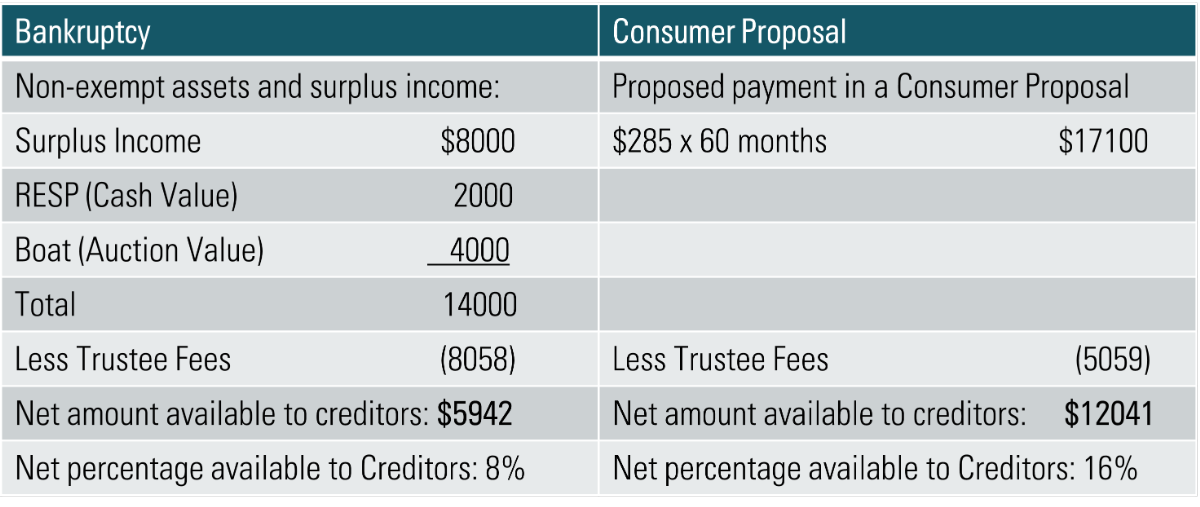

It is important to note that only a portion of the total debt owed by the debtor is repaid, and typically, there is a higher net percentage available to the creditors with a consumer proposal when compared to a bankruptcy.

As shown above, creditors often end up in a better position than they would have been if a bankruptcy process were filed, and that is why consumer proposals generally get approved.

Advantages and Disadvantages of a Consumer Proposal

What are the advantages of a consumer proposal?

For the majority of Canadians, the costs and fees that come with a consumer proposal are significantly less than the costs that come with bankruptcy. Once a consumer proposal has been signed, debt collectors will stop bothering the debtor, and the debtor’s physical assets will be protected. Once the creditors (representing 51% of the debtor’s debt) agree to a consumer proposal, they are obligated to work with the debtor (Debt.ca, 2022).

What are the disadvantages of a consumer proposal?

While a consumer proposal is less expensive, it has the same negative impact on a debtor’s credit that a bankruptcy does. It will remain on the a debtor’s credit report for up to seven years. The proposal will not go into effect if it is denied by 51% of the debtor’s creditors, and trustees are obligated to pay creditors as much as possible (Debt.ca, 2022).

Orderly Payment of Debts

Orderly payment of debts (OPD) is a debt payment program that is an alternative to bankruptcy in Canada. It is offered under the Bankruptcy and Insolvency Act of Canada (Bankruptcy Canada, 2022). This program is only available in the following provinces in Canada: Alberta, Saskatchewan, Prince Edward Island, and Nova Scotia.

Who is eligible for an orderly payment of debt program?

- Someone who is able to afford their debts in full.

- Someone who cannot afford the existing interest rates they are paying.

- Someone who cannot qualify for a consolidation loan.

Filing Process for Orderly Payment of Debt

|

Steps |

Actions |

|---|---|

|

Step 1 |

Contact a local administrator. The debtor would need to find a local organization that is responsible for administering the OPD program in that province. |

|

Step 2 |

Court Application. The administrator will make a court application on behalf of the debtor and establish a fixed interest rate of 5%. They will also initiate a stay of proceedings to stop active collection efforts of creditors. |

|

Step 3 |

Make Monthly Payments. The debtor is required to make monthly payments over a term of 26–48 months; payments are set based on the debtors ability to pay. |

The OPD program will be reflected on the debtor’s credit report for a period of two years. This is because while payments are being made, they are not the originally agreed upon payment terms.

Advantages and Disadvantages of an OPD

What are the advantages of a OPD?

An OPD minimizes or eliminates interest charges. On average, APR is reduced 0 to 10%. It is common for a debtor to become debt-free with 36 to 60 payments. It allows a debtor to make one, affordable payment for all of their total debt (Debt.ca, 2021).

What are the disadvantages of an OPD?

A debtor cannot use their current credit cards while they are enrolled in the program. They cannot apply for a new credit card while they are enrolled. Their credit card accounts will be closed once they are paid off. The OPD will be noted in the debtor’s credit report for two years from the date they complete the program (Debt.ca, 2021).

Note: It is important to note that lenders are not licensed insolvency trustees; they can only inform the client of the options that are available to them. It is best for the lender to refer their clients to an LIT to properly advise them on the best options for their situation.

References

Bankruptcy Canada. (2014, January 22). Orderly Payment of Debts. Bankruptcy Canada. https://bankruptcy-canada.com/bankruptcy-blog/what-is-an-orderly-payment-of-debts-or-consolidation-order/

Bankruptcy Canada. (n.d.). Are You Eligible For Bankruptcy. Bankruptcy Canada. Retrieved June 22, 2022. https://bankruptcy-canada.com/how-to-file-bankruptcy-canada/eligible-for-bankruptcy/

Office of the Superintendent of Bankruptcy Canada. (2018, October 12). About the OSB. Government of Canada. https://www.ic.gc.ca/eic/site/bsf-osb.nsf/eng/h_br01852.html

Office of the Superintendent of Bankruptcy Canada. (2020, March 23). Directive No. 11R2-2022R Surplus Income. Government of Canada. https://www.ic.gc.ca/eic/site/bsf-osb.nsf/eng/br03249.html

Office of the Superintendent of Bankruptcy Canada. (2015, March 24). Definitions. Government of Canada. https://www.ic.gc.ca/eic/site/bsf-osb.nsf/eng/br01467.html#o

Office of the Superintendent of Bankruptcy Canada. (2015, March 24). You Owe Money – Consumer proposals. Government of Canada. https://www.ic.gc.ca/eic/site/bsf-osb.nsf/eng/br02051.html

Office of the Superintendent of Bankruptcy Canada. (2016, June 6). What is a Licensed Insolvency Trustee?. Government of Canada. https://www.ic.gc.ca/eic/site/bsf-osb.nsf/eng/br03459.html

Bankruptcy Canada. (n.d.). Your Bankruptcy Discharge. Bankruptcy Canada. Retrieved June 22, 2022. https://bankruptcy-canada.com/how-to-file-bankruptcy-canada/bankruptcy-discharge/

Bankruptcy Canada.ca. (n.d.). What Is Bankruptcy? Declaring Personal Bankruptcy Meaning. Bankruptcy Canada Inc. Retrieved June 22, 2022. https://www.bankruptcy-canada.ca/whatisbankruptcy

Consolidated Credit. (n.d.). Consumer Proposal Guide. Consolidated Credit Canada. Retrieved June 22, 2022. https://www.consolidatedcreditcanada.ca/consumer-proposal/

Debt.ca. (2021 February 15). Orderly Payment of Debts, A Bankruptcy Alternative. Debt.ca. https://www.debt.ca/blog/orderly-payment-of-debts-a-bankruptcy-alternativeLexico. (n.d.). Definition of default. Lexico.com. Retrieved June 22, 2022. https://www.lexico.com/en/definition/default

Debt.ca. (n.d.). Alberta Consumer Proposal. Debt.ca. Retrieved June 22, 2022. https://www.debt.ca/consumer-proposal/alberta

Justice Laws Website. (2022, June 10). Part III: Proposals. Government of Canada. https://laws-lois.justice.gc.ca/eng/acts/b-3/page-12.html

Monkhouse Law. (2018, October 9). What Does It Mean to Have a Fiduciary Duty?. Monkhouse Law Employment Lawyers. https://www.monkhouselaw.com/what-does-it-mean-to-have-a-fiduciary-duty-toronto-employment-lawyer

Rumanek & Company, Ltd. (n.d.). Registrar In Bankruptcy In Ontario. Rumanek & Company Ltd. Retrieved June 22, 2022. https://www.rumanek.com/who-is-the-registrar-in-bankruptcy/

Additional Resources

BDO Canada Limited. (n.d.). Bankruptcy exemptions by province. BDO Canada LLP. Retrieved June 22, 2022. https://debtsolutions.bdo.ca/solutions/bankruptcy/bankruptcy-exemptions-by-province/

Hoyes and Michalos. (n.d.). Debts Eliminated By Bankruptcy Discharge. Hoyes, Michalos & Associates Inc. Retrieved June 22, 2022. https://www.hoyes.com/personal-bankruptcy/bankruptcy-discharge-debts/

Hoyes and Michalos. (n.d.). Duties in Bankruptcy Law. Hoyes, Michalos & Associates Inc. Retrieved June 22, 2022. https://www.hoyes.com/personal-bankruptcy/duties-bankruptcy-law/

Media Attributions

- image (30)

- image (31)

- image (32)

- Orderly payment of debts