7 Chapter 6 – Fraud Awareness

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- what the most common types of fraud in lending are.

- the meaning of Know Your Customer (KYC) and Know Your Transactions (KYT) and how they help detect and deter fraud.

- what acceptable forms of identification are.

- straw buyers, auto loan fraud, internal banking fraud, and mortgage fraud.

- how good decision-making skills are necessary to meet client needs while still maintaining business objectives.

Fraud Prevention in Lending Transactions

Lenders have a responsibility to protect the financial institution at which they are employed. They also have a responsibility to their clients to ensure that fraud or other financial crimes are not being committed in their name and that the client does not becomes a victim of a fraud scheme. Lenders need to proceed with care and caution with each client interaction to ensure their credit file is legitimate.

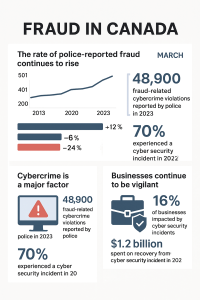

Understanding the Prevalence of Fraud

According to the 2021 Federal Trade Commission report, almost all financial fraud in the U.S. involved identify theft, which represented a 50% increase from the previous year.

Loan application fraud was one of the main complaints. Lenders need to know how to recognize and prevent fraud and, with experience, anticipate fraud happening. This chapter provides an overview of the techniques used by lenders and financial institutions to prevent fraud in lending transactions.

Source: (Statistics Canada, 2024)

Know Your Customer/Client

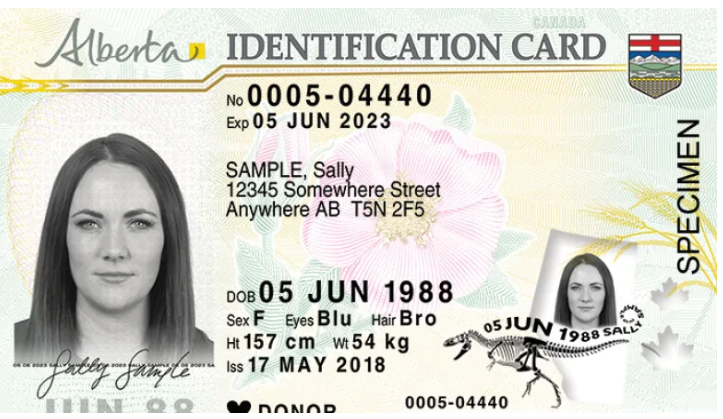

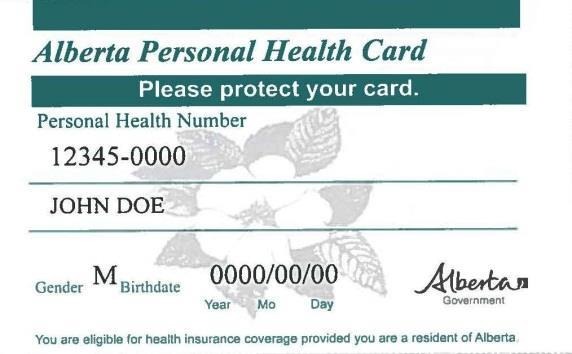

The know your customer/client (KYC) rule plays a significant role in all areas of banking because it is a way of detecting and deterring financial crimes. What is KYC? KYC is a mandatory process to identify and verify a client’s identity when first meeting with them to discuss their credit request. KYC ensures that the client is real and that they are who they say they are. If the client is an already existing client, it is still necessary to verify their identity by taking two pieces of accepted ID and verifying those against the information on file that had been previously collected.

According to the Financial Consumer Agency of Canada, there are different combinations of acceptable identification (Financial Consumer Agency of Canada, 2022).

Option 1

Show two pieces of ID from List A:

|

List A |

|---|

|

Valid Canadian driver’s licence that can be used as ID under provincial or territorial law |

|

Canadian passport |

|

Birth certificate issued in Canada |

|

Social Insurance card issued by the Government of Canada |

|

Old Age Security card issued by the Government of Canada |

|

Certificate of Indian Status |

|

Provincial or territorial health insurance card that can be used as ID under provincial or territorial law

|

|

Certificate of Canadian Citizenship or Certification of Naturalization |

|

Permanent Resident card or an Immigration, Refugees, and Citizenship Canada (IRCC) form IMM 1000, IMM 1442, or IMM 5292

|

|

Document or card with your picture and signature on it issued by one of the following authorities or its successors:

|

Option 2

A person can:

- show one piece of ID from List A above, and

- show one piece of ID from List B

|

List B |

|---|

|

Employee ID card with your picture on it that has been issued by an employer well known in the community |

|

Debit card or bank card issued by a member of Payments Canada with your name and signature on it |

|

Credit card issued by a member of Payments Canada with your name and signature on it |

|

Client card from the Canadian National Institute for the Blind with your picture and signature on it |

|

Foreign passport |

Example of Common IDs (Alberta)

While lenders need to be vigilant to ascertain their client’s identity, they must be careful not to falsely accuse someone, as repercussions can be severe. Read this article where a bank employee suspected clients of presenting fraudulent Indigenous status cards and called 911.

Know Your Transaction

Know your transaction (KYT) is a commonly used term in the financial industry. It means to examine all financial transactions for fraudulent or suspicious activities, including money laundering (CipherTrace, 2022). In regard to lending, the lender should always ask themselves, “Does this transaction make sense?” Product knowledge and a solid understanding of the financial institution’s processes is critical for the lender to grasp. It is vital to re-examine the purpose of the loan request and confirm that it appropriately aligns with what the client is asking for from the lender. Fraud prevention is a significant part of the lender’s role. If a lender misses seeing something suspicious or chooses to ignore something questionable just to get a credit deal done, this can lead to the lender being fired by their employer.

Different Types of Fraud

Straw Buyer Fraud

A straw buyer is a person who buys something on behalf of another person to circumvent legal restrictions or enable fraud (Lexico, 2022). Straw buyer mortgage fraud occurs when someone agrees to put their name on application on behalf of another person. The straw buyer typically receives a cash payment (Real Estate Council of Alberta, 2022). Click the following links to learn more about how the scam works and how to spot straw buyers.

Auto Loan Fraud

As with all financial transactions, auto loans are occasionally subject to fraud. This can take many different forms and involve a variety of different scams. Often, it will involve the use of stolen identification and the transactions will be completed online rather than in person.

Click the following link to a CBC News report to see how the pandemic lead to spike in auto fraud cases.

Internal Banking Fraud

Employees and former employees of financial institutions are known to participate in fraud schemes as well. In fact, fraud carried out by internal employees is a significant global problem. These employees are in a unique position as they have a front seat to an institution’s internal controls and it is easy for them to exploit any weaknesses (NetGuardians, 2022).

Click the following link to a CTV news report to review a recent example of bank loan fraud.

Mortgage Fraud

Mortgage Fraud

Case Study – Inexperience Isn’t a Defense

By Chip Cumming, CFE

Originally published in Mortgage Compliance Magazine (June 5, 2014)

Even though it was ten o’clock in the morning, it was still unusual to hear a knock at the front door. Sonya opened it slowly and was surprised to find two sharp dressed men on the porch.

“Good morning, are you Sonya?”

“Yes, I am” she replied.

“We’re with the FBI, and we’d like you to come with us….”

Such was the start of a 3-year nightmare for Sonya, in a twisted tale of mortgage fraud that involved over a dozen loans and millions of dollars in losses. Well, it actually started long before that.

Sonya was a processor hired directly by Charles, an experienced loan originator working for a “net branch” operation back in 2003. Although she had no experience, Charles was quickly able to teach her the basics of putting a loan package together, and she loved the fast pace of the new job.

Charles was a top producer, working exclusively with single-family investment properties, and some seemingly experienced rehabilitation specialists. Investors would purchase properties, fix them up, and then sell them to new first-time homebuyers. Charles would help the new families obtain the FHA mortgage and even arrange for gifts or creative down-payment scenarios to help them get into the new home for little or no money down…

You can see where this is headed. Unfortunately, Sonya didn’t.

The Scheme

Under the premise of “prepaying for repairs,” the seller of the property would advance certain funds to the borrower prior to closing. For convenience, Charles and the seller would document this as “gift funds” and coordinate with the appraiser to obtain an inflated “as is” appraisal. After the closing, some additional funds were promised to the borrower so they could complete the repairs, and the seller would walk away with the profit. Charles earned a nice commission, and the repairs eventually got done so the appraiser was covered.

Things seemed to be going so well that Charles even helped the sellers out by participating in transactions as an equity partner (under the guise of an LLC) and would take a percentage of the profits after the deal closed.

Everyone was happy. Investor sellers were happy, new homebuyer borrowers were happy, Sonya was busy and earning nice bonuses and Charles was living a comfortable life. Maybe too comfortable.

But there’s always a catch.

The Catch

One of the problems with fraud is that success breeds greed. The participants eventually want a bigger slice of the action or to build up the operation to generate more deals. The profits are too good, and the money spends too easy.

But there was one catch that Charles didn’t plan on—uncompleted repairs.

The city housing commission cited one of the property owners for safety violations. The homeowner who had financed the property with Charles had turned it into a rental property, and the tenants had complained about the condition of the home. Upon inspection, the city decided that there were severe safety issues and subsequently condemned the property.

With no rental income, the mortgage payments stopped, and the loan went into foreclosure. When investigating the loan, it was quickly discovered that stated repairs were never completed, the appraisal was fraudulent, and the true value was a fraction of what everyone thought it was. But that was just the tip of a very large iceberg that was about to come crashing down.

The homeowner filed a complaint stating that the seller was supposed to complete and pay for the repairs but of course didn’t. Loan files with similar problems and patterns became evident. Cross litigation followed, but as everyone looked around, nobody was there to pick up the pieces.

With the turn of the market, values had gone down, investors became hesitant, buyers became fearful, and mortgage offices shut down. At this point, even Sonya had been working at a health club for the past year and hadn’t seen or talked to Charles in years.

The Charges

The interview at the FBI office didn’t go well for Sonya. She was asked about her time at the mortgage company, her processing duties, and about her experience. Sonya indicated that she hadn’t had any formal training or experience in the mortgage industry but that she had enjoyed her time working with Charles. She confirmed that she had worked on many loan files for him and that he seemed like an experienced investor and finance expert. As a processor, her signature was on many of the documents.

Sonya was then charged with multiple felony counts, including mail fraud, wire fraud, and conspiracy to commit fraud. She was now looking at several years in federal prison.

As a certified fraud examiner, I became involved with her defense team to try to find out what really happened and what Sonya knew—or didn’t know. As I poured over stacks of loan files, her inexperience became obvious, and I could see that Charles was running the show. He had trained her in a specific way, and she knew nothing different, and she certainly didn’t question him on the operation.

But unfortunately for Sonya, inexperience isn’t a plausible defense. There were plenty of warning signs, and looking back, she knew something didn’t feel right. But what could she have done?

What should have tipped her off to the scheme? How could the lender have better protected itself? And was she really looking at hard prison time?

The “Red Flags”

In analyzing the loan files, there were several warning signs that should have alerted Sonya that something was wrong. Loan processors are a gateway for lenders to detect and prevent fraud, and processors should be extra careful in documenting unusual circumstances and similar patterns involving the same parties in a transaction, and they should not be afraid to ask questions when things are not clear. Some of the red flags that Sonya could have questioned included the following:

- multiple deals with the same investor within a short period of time

- similarly structured Gift Letters on multiple transactions with the same parties

- agreements for advance repairs or payments to a buyer prior to closing

- any agreements outside of the closing

- the loan officer involved as a “silent partner” on transactions with payments prior to or after closing

While these are just a few of the identified patterns and individually may not constitute a fraudulent transaction or intent, these red flags are among the easiest to catch by a processor on the front lines early in the process.

The lender could also have identified certain red flags in its process that may have alerted them to a problem. Internal procedures should include the following:

- identifying similar parties to multiple transactions

- Gift Letter verification procedures

- review of borrower verifications

- internal valuation reviews (acknowledging that appraisal requirements and procedures have changed in recent years)

- on-site branch audits, vendor due diligence and agreements, and compliance checks and certifications

The Fallout

After a lengthy investigation and review of the files, I was able to prepare a report which demonstrated that Sonya was an unintended co-conspirator, and she was offered a deal to cooperate and testify against others involved in the fraud. While this spared her jail time, it didn’t come without a cost. Probation, fines, the elimination of certain types of future employment, and public embarrassment—not to mention attorney fees, costs, time, and whole boatload of headaches and stress. Charles is now serving time in federal prison, and several others were charged in the case.

But that’s not the only fallout. Additional damage was done to the scores of buyers and families caught up in a system that allowed them to be led down a dangerous path. While there are certainly procedures and systems in place to protect buyers, lenders, and even people like Sonya, the systems are only as good as the people who run them. The integrity of the team members, practical and comprehensive training, attention to detail, and the willingness to ask simple questions if something doesn’t seem quite right—those are the best protections against fraud.

That’s something Sonya wished she had learned many years ago.

Author Note: The names and identifying features of this case study have been modified for privacy reasons.

Chip Cummings is the CEO of Northwind International Corp. and a certified fraud examiner with over 27 years of real estate lending and compliance experience. He is a best-selling author of nine books and a frequent speaker around the country. Chip can be reached at (866) 977-7900, via email at Info@NorthwindInternational.com, or through www.MortgageFraudConsultants.com.

Balancing Client Needs Against Business Objectives

Lenders are absolutely required to protect the financial institution for which they work, but they need to be able to balance this against the needs of their clients and what they need to do to help their clients achieve their goals. Read the following article, “Principles of Good Lending Every Banks Follows – Loans“ by Gaurav Arkani. In this article, he looks at seven general principles of good lending:

- Safety

- Liquidity

- Purpose

- Profitability

- Security

- Spread

- National interest, suitability, etc.

These are principles that all lenders should follow when appraising a proposal.

References

Akrani, G. (2010, September 9). Principles of Good Lending Every Banker Follows – Loans. Kalyan City Life Blog. https://kalyan-city.blogspot.com/2010/09/principles-of-good-lending-every-banker.html

CipherTrace Mastercard. (n.d.). Know Your Transaction (KYT). CipherTrace, Inc. Retrieved June 2021, 2022. https://ciphertrace.com/glossary/know-your-transaction-kyt/#:~:text=Know%20Your%20Transaction%20or%20KYT,As%20cryptocurrency

Federal Trade Commission. (2021, February). Consumer Sentinel Network: Data Book 2020. Federal Trade Commission. https://www.ftc.gov/system/files/documents/reports/consumer-sentinel-network-data-book-2020/csn_annual_data_book_2020.pdf

Financial Consumer Agency of Canada. (2022, March 31). Opening a bank account. Government of Canada. https://www.canada.ca/en/financial-consumer-agency/services/banking/opening-bank-account.html

Lexico. (n.d.). Definition of straw buyer. Lexico.com. Retrieved June 2021, 2022. https://www.lexico.com/en/definition/straw_buyer

NetGuardians. (n.d.). A-Z of internal banking fraud. NetGuardians, Inc. Retrieved June 2021, 2022. https://netguardians.ch/internal-banking-fraud/

Real Estate Council of Alberta. (n.d.). Straw Buyer Mortgage Fraud. Real Estate Council of Alberta. Retrieved June 2021, 2022. https://www.reca.ca/wp-content/uploads/2019/03/Straw-Buyer-Mortgage-Fraud.pdf

Statistics Canada. (2024, March 15). How much is fraud affecting Canadians and Canadian businesses? https://www.statcan.gc.ca/o1/en/plus/7905-how-much-fraud-affecting-canadians-and-canadian-businesses

Media Attributions

- ChatGPT Image Jun 26, 2025, 02_47_32 PM