4 Chapter 4 – Credit: Investigations and Applications Part 1

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- what is involved in a credit investigation.

- the importance of credit applications.

- what is required when completing a credit application.

- how financial institutions handle their credit/lending departments.

Credit Investigations

Credit investigations are undertaken by the lender to vet a client’s ability to pay back the loan. Clients who do not meet the requirements of the investigation will likely be denied the loan.

The more complex a client’s debt request, the more information gathering will be required. Financial institutions have specific requirements that need to be determined before funds can be released to the client.

Consider the following situation:

- Would you do the same level of investigation for a $1,500 overdraft request as you would for a $15,000 car loan request? Which warrants more investigation?

Due Diligence

Due diligence is a critical exercise in a lending transaction. It allows the lender to make an informed decision as to whether to grant credit or not and on what terms.

Considerations in Acquiring Information

Clients should be prepared to provide information that the lender requires to investigate their ability to repay the debt being requested. Personal information is required to determine their identity, and there is information required for the credit analysis that needs to be completed.

It is important to recognize that some credit deals are high risk, meaning the likelihood of repayment is questionable. There will be deals that do not get processed. In some cases, it is possible to mitigate the risk or modify the deal to get it approved. Risk can be mitigated by securing collateral for the loan, adding a co-signor, closing out other credit cards, or reducing the amount of money the client is requesting.

Clients should be prepared to provide the needed documentation. A lender must do their due diligence to verify that what the client has stated is, in fact, true. For example, if a client indicates that they have $100,000 in RRSPs, the lender may need to get statements to verify that this is the case.

Legal Authorization to Investigate

To proceed with a credit investigation, the client(s) need to sign a credit application. Their signature allows a lender to proceed with the investigation and access a client’s credit bureau for the credit analysis.

Credit Applications

Purpose

The lender and the client need to establish the purpose of the credit request. This formalizes the request and gives the lender authorization to proceed with a credit investigation. The purpose should align with the credit being requested. For example, if a client wishes to purchase a car, they will get a car loan, not a mortgage. The purpose can provide the lender with information on the credit worthiness of the applicant. Are they making a legitimate request, and does it make sense given their current financial situation?

Applications

The lender must verify the identity of the client. This is done by obtaining two pieces of identification and at least one piece of picture identification. Personal information required includes an address, date of birth, and social insurance number. The lender should ask questions about the information being provided. For example, if the client lives in Sherwood Park, why are they applying for credit at a branch in the west end of Edmonton? A lender must always be on guard for individuals posing as someone else to commit fraud. Remember, if something does not make sense, more questions need to be asked.

While collecting information, be careful to only discuss credit information with the applicant to whom the information applies. Privacy is important! Even with a married couple, the lender cannot provide one spouse’s financial information to the other spouse. It may be necessary to have discussions with each spouse separately, even though the loan is being requested jointly. If clients provide consent to share this information, then proceed with the discussion.

Required Information for an Application

Personal Contact Information

- social insurance number

- date of birth

- citizenship status

- marital status

- email address

- primary telephone number

- permanent address (minimum of three years history is required)

Employment and Income Information

- employment status (minimum of three years history is required)

- work phone number

- employer name

- gross monthly income amount and source(s) of income (all sources being considered for the loan)

Personal Loan Information (Loan Being Applied For)

- loan purpose

- desired term

- loan amount

- preferred payment due date

Additional Documents (Required as Necessary)

- recent pay stubs or other income verification documents

- utility bills (to verify address)

- driver’s license or social insurance number card

- consumer debt information (including mortgage or monthly rent payments)

- consumer debt information (to determine which accounts need to be paid out and closed [if necessary])

- power of attorney documentation (if one exists for the client)

- client’s asset information (for verification purposes)

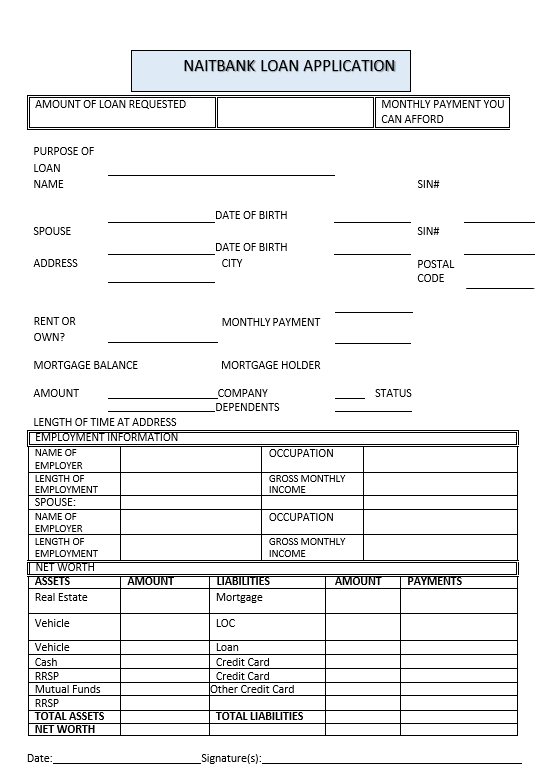

Example of a Credit Application

Most financial institutions use software to collect the data required for a credit application. Below is an example of a credit application. Note the required information the lender needs to collect.

mple of a credit application. Note the required information the lender needs to collect.

Credit Granting

The lender will need to review the applicant’s past financial behaviour to predict how they will handle credit in the future. This process ensures that the financial institution does not grant credit to clients who are unable to pay (AccountingTools, 2022). The goal for both the lender and the client is to continually improve their financial position so their financial goals can be achieved.

Financial institutions will have a strategic approach to how they handle their credit and lending departments. Some financial institutions will be more aggressive and take on higher-risk clients. This allows them to charge higher rates of interest to compensate them for the additional level of risk they are taking on. Other financial institutions will take a more measured and conservative approach to the extension of credit to clients. During times of economic uncertainty, it is not uncommon to see institutions tighten up their credit-granting processes as a way to navigate difficult times.

Reference

AccountingTools. (2022, May 14). Credit granting procedure. AccountingTools, Inc. https://www.accountingtools.com/articles/credit-granting-procedure

Media Attributions

- image (22)

- image (23)