5 Chapter 4 – Credit: Income Verification Part 2

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- why the income verification process is so important.

- the different sources that are acceptable for income verification.

- the income guidelines that could be used by a financial institution.

Income verification is a critical step in the credit file process, and the lender needs to make sure it is completed accurately. A client’s income indicates their ability to pay off their debt and affects how much of a debt load they can carry. If a lender has miscalculated a client’s income, there can be serious problems with the credit file.

Imagine a situation in which a lender incorrectly calculates the client’s income where the income is inflated. In this situation, a client could be approved for a debt load that will put them in the position of not being able to repay the debt. Alternatively, imagine the lender is halfway through the credit file, discovers their error, and corrects it. In this situation, the client no longer qualifies for the credit deal that was proposed. The lender will have to have an uncomfortable conversation with the client to let them know they do not qualify for the previously approved amount. Errors like this can hurt the client’s relationship with the lender and the financial institution.

In another example, envision a situation in which the lender incorrectly calculates the client’s income as being less than it actually is. In this situation, the client’s credit request would be unnecessarily declined. This missed opportunity is a loss of business for the financial institution and the lender. It is important that the lender verify and calculate the client’s income correctly to show that the client can support the new debt, per the application, and confirm CAPACITY.

Each bank/financial institution has its own policies for income verification. It is important that a lender follow the guidelines of the financial institution where they are employed. The income verification guidelines described in this chapter are for the purposes of this course.

The lending products and services that a financial institution offers can have different income verification requirements. For example, a mortgage could have different requirements than overdraft protection placed on an account. Lenders need to have a strong understanding of the requirements necessary for each credit file. This will help ensure the quality of the credit file and demonstrate efficiency from a client’s perspective.

Sources of Income Verification

Pay Stubs

The lender must ensure that the paystub is current. Usually, two to three pay stubs are required to show that the income is consistent. The paystubs should be clear; make sure the employer is identifiable. The employee information should be consistent with the client in the credit file. Click the following link to see an example of Canadian paystub.

Salary Letter

Clients may be required to provide a salary letter. The letter will help determine if the individual is on probation. It should be on company letterhead. The lender should perform their due diligence by calling the person who wrote the letter to confirm that the letter is legitimate. The lender should document this on the letter by writing the date and time they spoke with the writer. Click the following link to see an example of a salary letter.

Notice of Assessments

Notice of Assessments (NOAs) are another source of income verification that a lender may need to request from their client. Different financial institutions have various policies around using NOAs as a source of income verification. Lenders are most concerned with line 150 for income verification information.

Clients can obtain a digital copy of their NOAs by accessing “My Account” with The Canada Revenue Agency (CRA). Alternatively, clients may have a paper copy that they receive each year after filing their income taxes.

Source: Advantage Wealth, 2025

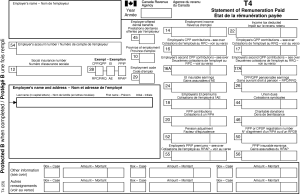

T4 Statement of Remuneration Paid (Slip)

Some financial institutions will accept a client’s T4 as an income verification source. Typically, a T4 statement is accepted as a verification source when a current NOA is not available. A lender would be concerned with line 14; they would use the information found there to verify a client’s income for that year.

Source: Avanti, 2025

Income Guidelines

As mentioned previously, financial institutions can have varying approaches for determining client income. Banks reserve the right to have their own policies regarding income verification. A lender is required to exercise due diligence to verify all sources of income to ensure the integrity of the credit file.

For the purpose of this course, we will follow the following guidelines. Make note of certain requirements for CAPACITY.

Overtime/Commission Income

Usually, a lender cannot make this part of the income calculation as it is not considered to be guaranteed income. If the lender needs the additional income to bring capacity (GDS and TDS ratios) into line, the lender will need to obtain two years of the client’s NOA to show a history of this income.

Part-Time Employment

The lender will need to determine the minimum guaranteed hours per week. A salary letter is the best source of confirmation for this income. For CAPACITY considerations, part-time employment should be included in income. However, use the current wages, not the historical wages.

Full-Time Employment

The lender will require the client to produce current pay stubs. Alternatively, if their pay is received via direct deposit, amounts can be taken, and a gross-up calculation can be used at the bank’s discretion.

Spousal/Child Support

The legal agreement needs to be obtained and a copy retained for the lender’s file.

Pension Income

The verification source could be an NOA or a T5. Some lenders may verify via direct deposit; amounts can be taken, and a gross-up calculation can be used at the bank’s discretion.

Rental Income

Rental income can be included in the calculation of the debt service ratios and form part of the client’s total gross annual income. To verify rental income as a source, the client needs to produce rental agreements along with bank statements confirming consistent collection of rent.

Review of Income Verification

|

Full-Time Employment |

Pay stubs, direct deposits (bank dependent), T4s, or a salary letter are all acceptable. |

|

Overtime/Commission |

NOAs are needed to show a history of the income. |

|

Part-Time Employment |

The bank will need to determine the minimum guaranteed hours per week. These hours are used in the calculation of monthly income. A salary letter is the best source of confirmation of this income. |

|

Spousal/Child Support |

The legal divorce agreement must be obtained, and a copy must be retained for the lender’s file. |

|

Pension Income |

NOAs, T5s, or direct deposit amounts can be taken, and a gross-up calculation can be used (at the bank’s discretion.) |

|

Self Employed |

The last two years’ NOAs can be used, taking the average of the two years. |

|

Maternity/Paternity Leave |

An employment letter is required to verify the full amount of income. The letter should indicate the timeframe of the leave and when the client is to return to the position in its full capacity. |

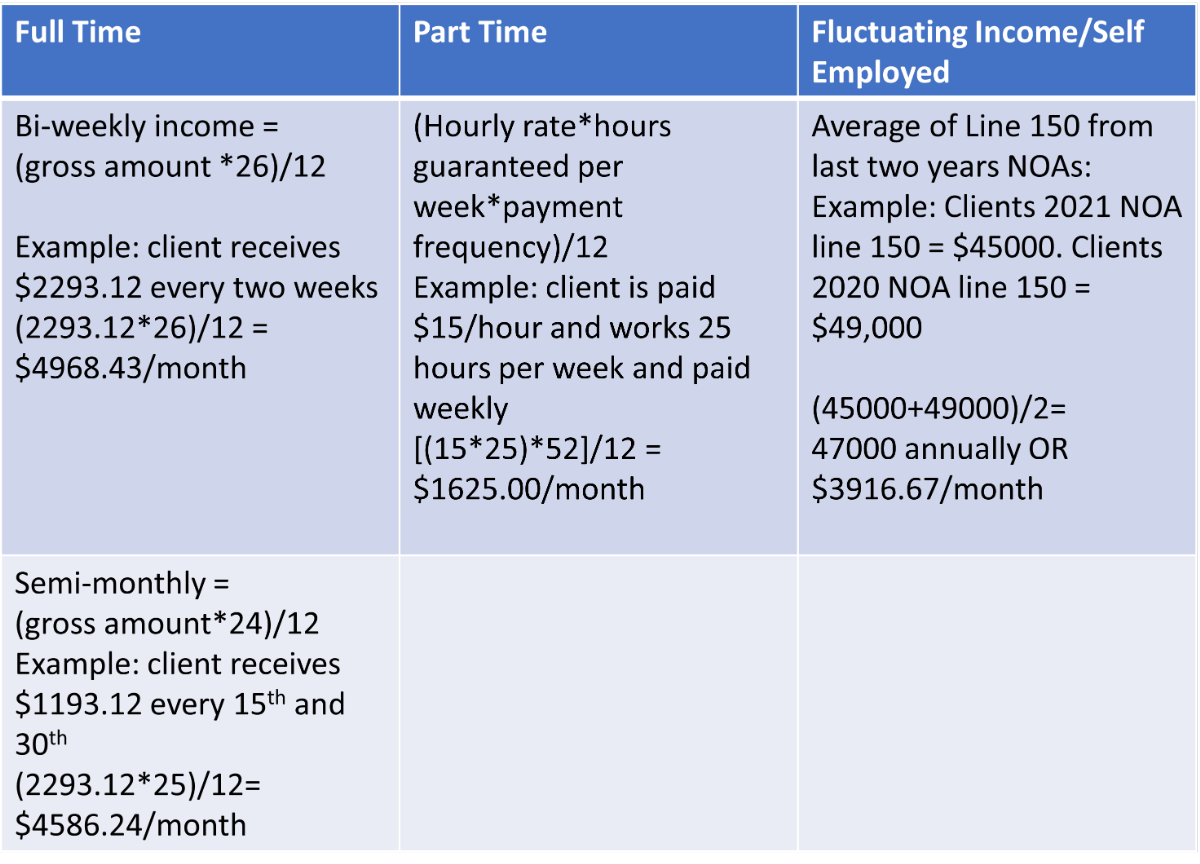

Calculating Income

Reference

Kagan, J. (2020, October 31). Direct Deposit. Investopedia. https://www.investopedia.com/terms/d/directdeposit.asp

Media Attributions

- NOA

- 6557bddd8f621b72ff4a321a_T4-Guide