6 Chapter 5 – Real Estate Lending: How is It Different?

Learning Objectives

LEARNING GOALS

Upon completion of this chapter, you should understand:

- why clients seek out a mortgage or may want to access the equity in their home.

- why clients may want to refinance and what they should examine prior to refinancing.

- the different types of mortgages available.

- how mortgage rates and mortgage-interest rates are structured.

- important terms and definitions relating to mortgages.

- how to complete a real-estate–secured application.

- how a builder mortgage is different.

Why Clients Seek Out a Mortgage Lender

There are several reasons why clients apply for a mortgage:

- to purchase a new or existing residential property;

- to build a residence or other property;

- to renew a mortgage term;

- to refinance a mortgage;

- to obtain interim (bridge) financing;

- to transfer an existing mortgage to a new lender;

- to change the people on a title;

- to remove a lien against a property; or

- to free up additional funds.

When individuals have accumulated equity in their home, they can use it to address financial needs that would otherwise be more costly to finance. Clients will use these funds for a variety of wants and needs, including:

- to purchase large ticket items;

- to renovate their home or to build an addition to their home;

- to fund their children’s education;

- to take a long-awaited vacation;

- to use the funds for investment purposes;

- to purchase a rental property;

- to purchase a business;

- to establish a business operating line of credit (with the property as collateral); and

- to fund retirement.

All of following can be used to obtain access to the equity in a home:

- a home equity line of credit (HELOC);

- equity taken out of a mortgage;

- a second mortgage; and

- a reverse mortgage.

Mortgage refinancing occurs when the terms and conditions of an existing mortgage are replaced with new terms and conditions before a mortgage is due for renewal.

Reasons why someone would consider refinancing are as follows:

- to consolidate debt;

- to extend an existing mortgage amortization for lower monthly payments;

- to rewrite the mortgage to take advantage of lower-interest rates; and

- to pull out capital for a specific purpose by increasing the principal of the mortgage.

Refinancing can be very costly, and the client would need to consider the following before doing so:

- a discharge penalty consisting of the greater of 3 months’ interest or interest rate differential (IRD);

- appraisal fees;

- legal fees;

- the additional cost of borrowing; and

- transactional fees.

Types of Mortgages

There are many different types of mortgages available. It is important for a mortgage lender to have a good understanding of the different types of mortgages so they can determine which type will best suit the client.

Conventional Mortgage

If a client has 20% of the purchase price of the property to use for a down payment, a traditional mortgage is acceptable. This means the bank provides the remaining 80% in the form of a conventional mortgage. For the lender, this is considered favourable as the risk is reduced by the client having more equity in the home. For example,

- Suzanne has saved $90,000 for a down payment.

- The home is worth $450,000 on the real estate market.

Her lender calculates the following mortgage amount:

|

Appraised value of home: |

$450,000 |

|

Less 20% down payment: |

$90,0000 |

|

Total mortgage amount |

$360,000 |

High-Ratio Mortgage

A high-ratio mortgage occurs when the mortgage amount exceeds 80% of the value of the property up to the maximum of 95% of the value of the property.

The Bank Act and the Trust and Loan Companies Act require high-ratio mortgages to be insured against default (Office of the Superintendent of Financial Institutions of Canada, 2020). The lender is insured against the risk, and the client pays the premiums. The client can choose to pay the premiums up front, or the premiums can be added to the mortgage principal. In Canada, there are three acceptable insurers of this type of insurance: 1) Canada Mortgage and Housing Corporation (CMHC), 2) Genworth Financial, and 3) Canada Guaranty Mortgage Insurance. The insurance premium can be transferred from one financial institution to another without added cost to the client if the mortgage principal amount increases. In a refinance, a new premium is charged on the top-up amount only.

| Loan-to-Value | Premium on Total Loan | Premium on Increase to Loan Amount for Portability |

|---|---|---|

| Up to and including 65% | 0.60% | 0.60% |

| 65.01% to 75% | 1.70% | 5.90% |

| 75.01% to 80% | 2.40% | 6.05% |

| 80.01% to 85% | 2.80% | 6.20% |

| 85.01% to 90% | 3.10% | 6.25% |

| 90.01% to 95% | 4.00% | 6.30% |

| 90.01% to 95% with non-traditional down payment | 4.50% | 6.60% |

[Table 6.1] CMHC mortgage loan insurance information and premium rates. (Source: CMHC, 2025a)

It is important to note that for certain specialty properties, the mortgage is required to be insured despite the loan to value being less than 80%, and this can vary by financial institution. For example, some financial institutions write mortgages on mobile homes, which require CMHC insurance regardless of the loan to value. For example,

- Roger and Pat have found their first home to purchase, and the asking price is $275,000.

- The couple has $13,750 in a combination of savings and RRSPs.

- They would like to include the CMHC premium into their mortgage as they do not have additional funds set aside for this cost.

Their lender calculates the following mortgage amount:

|

Appraised value of home |

$275,000 |

|

Less required 5% down payment |

–$13,750 |

|

Potential maximum for a high-ratio mortgage, based on appraised value (maximum 95% LTV) |

$261,250 |

|

Calculation of the CMHC premium: |

|

|

CMHC premium at 4% (261,250 x 0.04) |

$10,450 |

|

ADD premium to high-ratio mortgage amount. |

$271,700 |

|

Total mortgage amount, including CMHC premium |

$271,700 |

Note that mortgage payments can now be calculated for Roger and Pat using the mortgage balance of $271,700.

|

The approach used will depend on the nature of the application for mortgage-loan insurance and the information available. For instance, when the property is the subject of the mortgage-loan insurance application, the following will apply:

|

Refinancing

Some lenders offer their customers refinancing options. This provides homeowners with the option to access the equity they have built up over time. Refinancing may involve changing the terms of the original mortgage agreement, and the refinanced portion may have a different interest rate than the original mortgage. There may be associated penalties, and these can vary from one financial institution to another.

Home Equity Lines of Credit

A home equity line of credit (HELOC) works much like a regular line of credit. A client can borrow money whenever they want (up to the credit limit), pay it back, and borrow again. A HELOC allows clients to make interest-only payments, which means that clients could never actually pay the principle. Lenders should recommend that clients pay more than the monthly interest payment to ensure their balance (debt) is being reduced.

The Office of the Superintendent of Financial Institutions (OSFI) is an organization that regulates lenders and has set guidelines that address the maximum amount for HELOCs. Lenders may have a maximum of 80% loan-to-value (LTV) for a HELOC; however, the revolving portion cannot exceed 65% (Office of the Superintendent of Financial Institutions of Canada, 2020).

Example 1.0 – Client is applying for a HELOC and has an existing mortgage of $200,000:

|

Current Market Value of Home: |

$500,000 |

|---|---|

|

Max. LTV on HELOC 80%: |

$400,000 |

|

Subtract existing mortgage: |

-$200,000 |

|

Amount of new HELOC: |

$200,000 |

Example 2.0 – Client is applying for a HELOC with no existing mortgage:

|

Current Market Value of Home: |

$500,000 |

|---|---|

|

Max. LTV on HELOC 80%: |

$400,000 |

|

No existing mortgage: |

0 |

|

Amount of HELOC (revolving portion) 65%: |

$325,000 |

|

Amount of HELOC (fixed portion): |

$75,000 |

For a revolving home equity lines of credit the lender calculates the minimum payment as interest only. As an example, if a client has a line of credit balance of $50,000 and the interest rate is 5%, the payment is calculated as:

Step 1: (0.05 * $50,000) = $2500

Step 2: $2,500/365 = $6.85

Step 3: $6.85 * 30 = $205.48 minimum payment due

The fixed portion of the home equity lines of credit is principal + interest, and is calculated the same as a regular mortgage.

Stress test rules (see below) apply for HELOC qualification purposes.

Stress Testing for Mortgages

The Canadian Government decided that the housing market needed to slow down in 2017. New regulations were put in place in January of 2018 that apply to anyone applying for a mortgage. The stress test is not an added cost to the borrower; it is another method to determine if a client can afford their mortgage payments if interest rates increase in the future. Since the introduction of the stress test, the government has continued to modify the requirements. Lenders need to be aware of these changes and adjust accordingly. As of June 1, 2021, the rules changed to include the following (Financial Consumer Agency of Canada, 2021):

The lender will use the HIGHER of:

- the rate of 5.25% OR the client’s negotiated rate plus 2%.

If a client already owns their home, they will be subject to the stress test under the following conditions:

- the clients are refinancing their existing mortgage;

- the clients are transferring their mortgage to a new lender; and

- the clients are taking out a home equity line of credit.

Mortgage Reform in Canada: 2024 Update

New Measures Introduced in 2024

On August 1, 2024, the federal government implemented a policy allowing 30-year insured mortgage amortizations for first-time homebuyers purchasing new builds. This change lowers monthly payments and increases accessibility to the housing market.(Department of Finance Canada, 2024)

Building on this measure, the government of Canada announced additional reforms to take effect on December 15, 2024, including:

-

Increasing the insured mortgage price cap from $1 million to $1.5 million, acknowledging rising home prices. This adjustment—unchanged since 2012—enables more Canadians to qualify for mortgage insurance with a down payment under 20%.

-

Expanding 30-year amortization eligibility to:

-

All first-time homebuyers, not just those purchasing new builds.

-

All buyers of new construction homes, regardless of whether it’s their first purchase.

-

These changes are also designed to stimulate new home construction, including condos, to help address Canada’s ongoing housing supply shortage. (Department of Finance Canada, 2024)

Strengthened Canadian Mortgage Charter

The updated mortgage charter, introduced in Budget 2024, includes provisions that allow insured mortgage holders to switch lenders at renewal without undergoing a new mortgage stress test. This promotes lender competition and helps consumers secure better rates and terms at renewal. (Department of Finance Canada, 2024)

Structure of a Mortgage

Open Mortgage

An open mortgage allows the client to pay off their mortgage without the risk of penalty. Terms for an open mortgage can range from six months to five years. This type of mortgage is beneficial for a client who wants flexibility as they are expecting funds to pay off the mortgage. The rate of interest can be fixed or variable.

Closed Mortgage

A closed mortgage indicates that the client cannot exceed the agreed-upon repayment terms of the mortgage without a penalty being applied. The rate of interest can be fixed or variable.

Mortgage Interest Rate Structure

Fixed-Rate Mortgage

A fixed-rate mortgage has an interest rate that is fixed, and it will not change over the length of the term chosen. The benefit for the client is that they will have consistent mortgage payments for the length of the term. They will not need to be concerned that their payments will change. For example, a 5-year term mortgage has a rate of 4.75%, and this rate remains the same for the entire 5-year period.

Variable-Rate Mortgage

A variable-rate mortgage has an interest rate that is tied to the prime rate. Each financial institution will offer this type of mortgage in variation from prime to prime plus a certain percentage. This interest rate will change if the prime rate increases or decreases. Clients will find that when interest rates drop, more of their mortgage payment is being applied to the principal, while the opposite would be true if interest rates increase.

Split-Rate Mortgage

A split-rate mortgage offers the client the ability to combine the features of a fixed-rate mortgage and a variable-rate mortgage into one product. A portion of the mortgage may have a fixed rate, while another portion has a variable rate. This option allows the client to take advantage of rate changes without exposing their entire mortgage principal to an interest rate risk.

Mortgage Terms and Definitions

Assumable Mortgage: An assumable mortgage allows purchasers to take over (assume) an existing mortgage, though there is a requirement that the purchaser also needs to qualify for the mortgage. This would be beneficial to the purchaser if the existing mortgage has an interest rate that is lower than the current rates being offered.

Cash Back: This is an option that can be offered to a client that provides “cash” to them upon the funding of the mortgage. Clients often will use these funds for furniture, renovations, landscaping, or to assist in paying down other debts. This is not always the most favourable option, as the interest rate in a cash-back mortgage is higher than regular mortgage rates. Clients will pay more in interest costs over the term of their mortgage.

Construction/Builder Mortgage: For a client who is building a home, most financial institutions will have the option of a construction/builder mortgage. This allows funds to be provided to the builder in stages. At each funding stage, the property is inspected to determine that the stage is complete, and then new funds can be advanced. During the building process, the client is responsible for paying interest on the amount that is outstanding. Once the house is complete, the mortgage converts to a standard mortgage, and principal and interest payments would be required.

Homeowner’s Insurance: All financial institutions that issue mortgages require that the homeowner carry insurance on the property for not less than the replacement value in Canadian dollars. This ensures that the collateral/security is protected against damage or loss. The lender is required to obtain proof from the client that the property is adequately insured.

Investment Mortgage: An investment mortgage is an option for a client looking to purchase a rental property or to purchase a property to renovate and later sell for a higher amount. Each lending institution will have its own guidelines for this type of mortgage that lenders must adhere to.

Mortgage for Newcomers: These mortgage applications can often be quite difficult and involve a lengthy process to verify the identity and legitimacy of the information being provided. The lender needs to adhere to the financial institution’s guidelines to determine creditworthiness and protect the institution against fraud.

Portable Mortgage: If a client has an existing mortgage and they are looking to purchase a new property, the client could choose to port their mortgage. In effect, this allows the client to move their existing mortgage with them to their new property. A portable mortgage option is typically reserved for fixed-term mortgages and does not include variable-rate mortgages. If a client needs additional funds to purchase, the lender can do a top-up for the required additional funds; this portion of the mortgage would be at the current interest rate. The client would see a blended rate on their mortgage statement, which contains the original mortgage rate and the new mortgage rate. If the existing mortgage is insured, and the mortgage is still considered to be a high ratio (loan to value exceeds 80%), then the client pays the insurance premium on the new funds and not the entire mortgage principal. This is because the original mortgage insurance premium has already been paid.

Property Taxes: Once a mortgage has been advanced, the client is responsible for paying the property taxes associated with the property. When a client requests a refinance, the lender needs to verify that property taxes are paid and up to date. The concern is that if a client is not paying their property taxes, the city or county could put a lien on the property, which, in turn, puts the financial institution’s security/collateral at risk.

Reverse Mortgage: A reverse mortgage allows the client to access the equity in their home either as a lump sum or as ongoing advances. This option is reserved for clients 55 years and older. Clients are not required to make payments but are required to pay property taxes and home insurance. The full amount that is owed comes due when the home is sold or both spouses have either moved or died. This option is beneficial for older clients as it gives them access to funds to assist with their retirement needs and allows them to stay in their homes longer.

Other Required Documentation for Real Estate Lending

- the MLS listing

- purchase and/or sale agreement(s)

- homeowner’s insurance statement

- property tax assessment

Completing the Application

For all mortgage applications, the client would initially meet with the lender to apply for a mortgage and determine what amount they qualify for and what their different options are. In the first meeting, the lender completes the application in the same manner as a consumer loan. The lender needs to ensure they are careful and collect accurate information about the client’s assets and liabilities as these are more closely scrutinized in a mortgage application. Wherever possible, a lender should complete their due diligence and verify all the assets a client states they have.

The initial meeting will bring about many questions and answers. What is the purpose? When is the possession date? When are funds required? How are they obtaining the down payment?

Questions like these can lead the conversation to different solutions that fit the client’s needs. For the purposes of this course, we will address common mortgage applications that a lender would encounter in financial institutions. A high-ratio mortgage purchase and an equity take out are two types of mortgages that a lender would commonly encounter. It is important to keep in mind that financial institutions can vary in the types of mortgages they grant and can approach the approval processes in different manners.

High-Ratio Mortgage Application

A lender needs to clarify several different elements to determine how the mortgage application will be put together.

If the client has a current home, the lender would need to consider the following:

- Who is the holder of the mortgage?

- What are the monthly payments on the existing mortgage?

- What is the balance of the mortgage?

- Is the client planning to sell this home or planning to rent the property?

For the new property, the lender would need to consider the following:

- What is the address and legal description?

- What is the property type (e.g., single-family home, duplex, condo, etc.)?

- What is the purchase price?

- What is the amount and the source of the down payment?

- When is the closing date?

- What is the appraisal value of the new home?

Once the lender has this information, they can consider whether the client could potentially qualify for the mortgage.

A client who is selling their property and buying another home would need to provide the lender with the following:

- the MLS listing of their existing property and their sale agreement;

- the MLS listing for their new property and their purchase agreement;

- the income requirements: recent pay stubs and salary letter;

- the down payment verification; and

- If the down payment is coming from the sale of property, then the sale agreement is sufficient.

- If a client is pulling funds from their savings, typically, 90 days of account history showing this amount is required.

- If a client is using funds from investments, current investment statements showing sufficient amounts for the down payment are required.

- If the down payment is a gift from family, a gift letter that is authenticated by the family’s bank is required.

- If RRSPs are the source of funds, first-time homebuyers require RRSP investment statements.

- home insurance and property tax confirmation would be handled by the solicitor upon completion of the deal.

A client who is buying their first home would need to provide the lender with the following:

- the MLS listing for their new property and their purchase agreement;

- the income requirements: recent pay stubs and salary letter;

- down payment verification, which is the same as outlined above; and

- home insurance and property tax confirmation would be handled by the solicitor upon completion of the deal.

Home Equity Line of Credit Application (Equity Take-Out)

A client who is applying for a home equity line of credit to complete an equity take-out would need to provide the lender with the following:

- their mortgage statement with the current balance shown. If the mortgage is at another financial institution, then a request would be made by the lender on behalf of the client to obtain that information from the other bank;

- the income requirements: recent pay stubs and salary letter;

- home insurance statement showing their policy is up to date; and

- property tax confirmation showing that property taxes are paid and up to date.

Builder Mortgages

There comes a time when a client does not want to purchase an existing home. If they want to build the house of their dreams, a lender needs to be prepared to work with the client through this process, as it typically can be lengthy. On average, six months to a year can be expected from start to finish, but if complications arise, that timeframe can be much longer. The lender who sets the right expectations around the timing of a build will be appreciated by their clients.

What do you need from the client?

- construction plans/blueprints – for an appraisal of the plans

- contract with the builder outlining all costs

- if the land is purchased, a copy of the deed and proof of sale

- if the clients are existing homeowners, they will need to determine their ability to carry two mortgages for the length of time the new home is built

- clients may need to rent out their existing home if they cannot carry two properties—you will need the rental agreement. Alternatively, a rental market evaluation may be needed.

The challenge that clients may not realize is how they can keep their existing home while waiting for their new home to be built. For some, this is very difficult as they must demonstrate that they can debt service both mortgages during the build. Sometimes clients will have to make difficult decisions like selling their home and renting—this would be factored into debt servicing, and clients would still need to show that they are within guidelines. Alternatively, if they sell, they move in with family while the building is happening. Another option is for the clients to rent their existing home and move in with family. The home-building process is time-consuming and not the easiest for clients, but the goal for them is their home once completed.

The land lot the clients are looking to build their home on is critical to the builder’s mortgage process. Often land may not be developed, nor have services set up for the land reducing the value of the land. Financial institutions often seek that the client has a minimum of 35%–50% invested in the land. Depending on the home builder, the clients may have options for purchasing the land. It is important to note that the options below are unavailable to all home builders; it will depend on how the home builder structures their business.

|

Option 1: Lot is included in the overall price |

Option 2: Client must purchase the land separately |

|---|---|

|

This option makes the process more ideal and can be less costly to the buyer. |

This is known as a land loan. |

|

There is concern that the lot price is inflated in these deals. |

Dependent on the financial institution clients are required to have minimum of 35%–50% down. |

Once we have received the construction plans or blueprints, you would need to have them appraised. The cost of the appraisal can be carried by the client, though, at times, the financial institution may have promotions to waive this cost. Appraisal fees can be between $350–$500. Getting the appraisal done and the lender receiving this information takes time. Once the value has been ascertained, the lender can determine if the client’s financing needs are sufficient and begin the application. This is much similar to the process for an existing home mortgage.

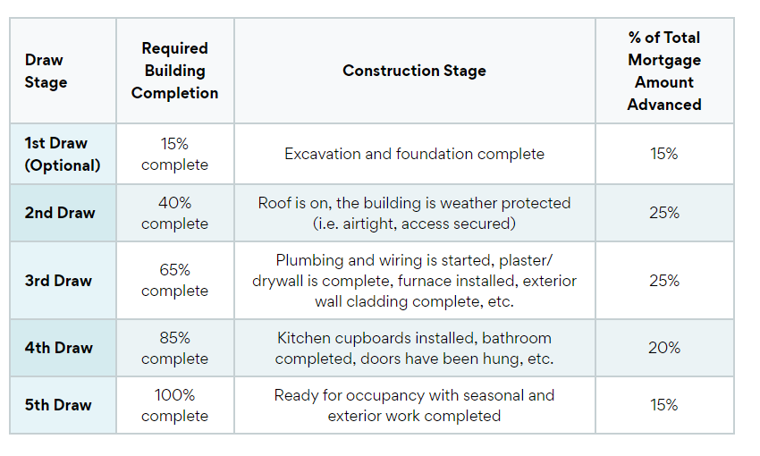

Construction/Builder Mortgages: Funds are advanced in stages. At each stage, there is an inspection before new funds are advanced. The customer only pays interest on the outstanding balance. When construction is complete, the mortgage becomes a standard mortgage, and blended payments of interest and principal begin. There are two options for a builder mortgage that clients can work through. Again, this will depend on the home builder on what they allow.

|

Completion Mortgage |

Progress Draw Mortgage |

|---|---|

|

Builder fully funds the build and requires clients to have their mortgage fund when they move-in to the home. Similar to a regular mortgage application. |

When the build meets certain stages of progression the lender will fund in installments until the project is completed or close to completion. |

|

Advantage to the client: allows time to sell their existing home if they have one. |

|

|

Disadvantage to the client: dependent on the builder whether this is the option. |

More common practice that is seen is the progress draw mortgage. Let’s take a look at a progress draw:

If the client already owns the land being built, a first advance is available as equity take-out. If the land is not yet purchased, a first advance is available to assist the client with purchasing a vacant lot.

Before each draw is advanced, an inspector will go to the property to ensure the builder follows the NHW (New Home Warranty) policies and to ensure each stage is completed with accuracy before releasing funds.

The cost of the inspections falls on the client. Some banks deduct appraisal and progress inspection fees from each draw.

After the mortgage is approved and signed, the client will not be able to change their mortgage amount to accommodate any upgrades or changes made to the home.

A lender needs to be versatile in residential lending; there are a variety of requests that a lender could receive and each one different. The more experience a lender gets working through applications, the more experienced and successful they will be.

References

Canada Mortgage and Housing Corporation. (2018a, March 31). CMHC mortgage loan insurance costs. Government of Canada. https://www.cmhc-schl.gc.ca/en/consumers/home-buying/mortgage-loan-insurance-for-consumers/cmhc-mortgage-loan-insurance-cost

Canada Mortgage and Housing Corporation. (2018b, March 31). Calculating GDS/TDS. Government of Canada. https://www.cmhc-schl.gc.ca/en/professionals/project-funding-and-mortgage-financing/mortgage-loan-insurance/calculating-gds-tds

Department of Finance Canada. (2024, September 16). Government announces boldest mortgage reforms in decades to unlock homeownership for more Canadians. Government of Canada. https://www.canada.ca/en/department-finance/news/2024/09/government-announces-boldest-mortgage-reforms-in-decades-to-unlock-homeownership-for-more-canadians.html

Financial Consumer Agency of Canada. (2021, July 13). Preparing to get a mortgage. Government of Canada. https://www.canada.ca/en/financial-consumer-agency/services/mortgages/preparing-mortgage.html#toc2

Lexico. (n.d.). Definition of mortgage. Lexico.com. Retrieved June 20, 2022. https://www.lexico.com/en/definition/mortgage

Office of the Superintendent of Financial Institutions. (2014, November 6). Final Guideline B-21 – “Residential Mortgage Insurance Underwriting Practices and Procedures” and Consequential Amendments. Government of Canada. https://www.osfi-bsif.gc.ca/Eng/fi-if/rg-ro/gdn-ort/gl-ld/Pages/b21_let.aspxOffice of the Superintendent of Financial Institutions. (2020, October). Home Equity Lines of Credit (HELOCs) Report (J2). Government of Canada. https://www.osfi-bsif.gc.ca/Eng/fi-if/rtn-rlv/fr-rf/dti-id/Pages/heloc.aspx

Ratehub.ca.(2022, October). Construction Mortgage Loans. https://www.ratehub.ca/construction-mortgage-loans

Media Attributions

- image (24)

- image (25)

- image (26)

- ChatGPT Image Jun 26, 2025, 02_20_49 PM

- image (27)

- image (28)

- image (29)