Chapter 7: Payroll Obligations on Termination of Employment

7.5 Incorporating Termination Payments into the Determination of Payroll

7.5.1 Calculating Net Pay on Termination (Last Paycheque)

Work through the following example:

Shayenne works for RAD in British Columbia and earns an annual salary of $74,600.00, paid biweekly. Shayenne’s employment will be terminated at the end of this pay period. She is entitled to 6% vacation pay on her vacationable earnings of $78,000.00 and five weeks’ wages in lieu of notice. Her vacation pay and wages in lieu of notice will be paid together on a separate payment from her regular pay.

Shayenne’s federal and provincial TD1 claim codes are 3. She will not reach the Canada Pension Plan or Employment Insurance annual maximums this pay period.

Calculate the employee’s net pay on the separate payment. Use 2022 rates.

Hint: Use the bonus method when calculating income taxes.

7.5.2 Retiring Allowances and Severance

Under the Income Tax Act, the term retiring allowance is used to describe payments made to an employee upon or after termination of employment. A payment sometimes called severance may qualify as a retiring allowance if it is paid:

-

on or after retirement from employment, or

-

as compensation for loss of an office or employment.

If a payment does not meet these criteria, it is not considered a retiring allowance for income tax purposes.

Eligibility for RRSP Transfers

A portion of a retiring allowance may be transferred directly to an RRSP without using the employee’s regular RRSP contribution room if it relates to years of service before 1996:

- $2,000 for each year or part year of employment before 1996, and

-

an additional $1,500 for each year or part year of employment before 1989 during which the employee did not belong to or was not fully vested in a registered pension plan (RPP), pension fund, or deferred profit-sharing plan (DPSP).

Any amount above these limits can still be contributed to an RRSP if the employee has sufficient personal contribution room.

Tax Withholding on Payment

When paying a retiring allowance to a Canadian resident:

-

Employers may use lump-sum withholding rates to calculate the tax to be deducted, or

-

At the employee’s request, the employer may calculate the income tax deduction using the annual tax tables (regular taxation method).

Employees have the right to request that tax be withheld at their annual rate. Lump-sum rates are simply an administrative option used when regular earnings are no longer being paid.

CPP/QPP, EI, and Payroll Tax Treatment

-

Retiring allowances are not pensionable and not insurable—do not deduct CPP/QPP or EI.

-

The Northwest Territories and Nunavut payroll tax applies to retiring allowances and qualifying severance payments.

-

Provincial or territorial health/payroll taxes may also apply depending on jurisdictional rules.

Reporting Requirements

Report retiring allowances on the T4 slip as follows:

- Code 66: Eligible portion (transferable to an RRSP without using contribution room).

- Code 67: Non-eligible portion

In Québec, employers must also report the payment on the RL-1 slip and may use the Québec lump-sum withholding rates if applicable.

Example

An employee retires after 25 years of service. They have 10 years of employment prior to 1996 and 5 years prior to 1989 in which they were not vested in the pension plan.

-

Eligible portion: (10 × $2,000) + (5 × $1,500) = $27,500

This amount may be transferred directly to the employee’s RRSP without affecting their contribution room. Any additional retiring allowance is subject to regular taxation.

Classifying Eligible and Non-Eligible Portions

When calculating a retiring allowance, the total payment must be separated into eligible and non-eligible portions for T4 reporting and RRSP transfer eligibility:

- Eligible limit = ($2,000 × number of years or part years before 1996) + ($1,500 × number of years or part years before 1989 not vested).

-

-

This portion may be transferred directly to an RRSP without affecting the employee’s regular RRSP room.

-

Eligible portion – the amount related to employment before 1996, plus any pre-1989 years where the employee did not belong to or was not fully vested in a registered pension plan (RPP), pension fund, or deferred profit-sharing plan (DPSP).

-

-

Non-eligible portion – any amount above the eligible limit. This portion may also be contributed to an RRSP if the employee has sufficient personal contribution room.

Employers must report these amounts on the T4 as follows:

-

Code 66 – Eligible Retiring Allowance

-

Code 67 – Non-Eligible Retiring Allowance

7.5.3 Prepare a Record of Employment (ROE)

7.5.3.1 What is a Record of Employment?

A Record of Employment (ROE) is a form completed by the employer that reflects the employee’s employment history with an organization. This record allows the employee to apply for employment insurance (EI) benefits if they meet the qualifications.

7.5.3.2 When to Issue an ROE

Employers are required to issue a Record of Employment (ROE) after an employee is terminated. The ROE provides information about the employee’s employment history and is used to determine the employee’s eligibility for employment insurance benefits.

7.5.4 How to Prepare an ROE

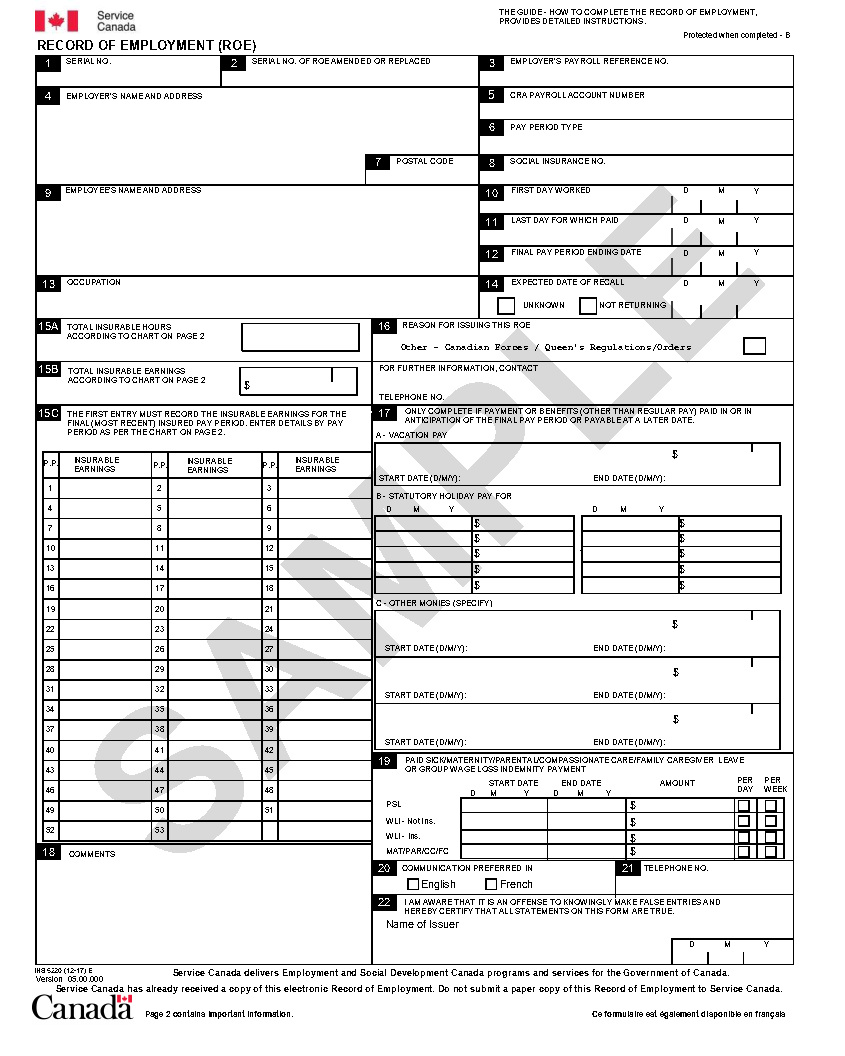

Completing an ROE involves several steps to ensure accurate and timely documentation of an employee’s employment history. The Service Canada (2021) publication How to Complete the Record of Employment form provides step-by-step instructions for completing an ROE. A sample ROE form and instructions are provided below:

Step 1: Administrative information (Blocks 1–9 and Blocks 13–14) can be completed in any order you like.

Step 2: Complete the period of employment information in Blocks 10, 11, and 12. This information provides you with the timeframe for which you need to report the employee’s insurable hours and earnings.

Step 3: Enter any separation payments paid or payable to the employee in Blocks 17A, 17B, and 17C.

Step 4: Calculate the insurable hours and enter them in Block 15A. The hours in Block 15A are for the prior 53 weeks or less depending on first date worked.

Step 5: If you need to complete Block 15C, do it next. Then enter the total insurable earnings in Block 15B for paper ROEs only. Going back the equivalent of 27 weeks or less based on first day worked. Electronic ROEs have this section greyed out. Only payments on termination that are deemed to insurable earnings are included in Block 15B. For instances vacation and wages in lieu of notice. Severance and Retiring Allowances are not insurable and not included. Remember to include the insurable separation payments you entered in Block 7 in the total amount you enter for the final pay period.

Step 6: Block 15C is mandatory for an electronic ROE, going back 53 weeks or less depending on the first date worked. It is optional for Paper ROE not following the variable best weeks initiative as long as there are no NIL pay periods.

Step 7: Indicate vacation payments in 17A, statutory holiday payments after the last date of work in 17B, and termination payments such as wages in lieu of notice, severance, and retiring allowances in 17C.

For Block 17C, include both the payment amount and the payment date (for example, Wages in Lieu of Notice – $7,173.08 paid on 2022-07-15). This ensures Service Canada can confirm when the separation payment was issued.

In Block 1 of 15C include the most recent pay period, and payments on termination that are insurable. For instances vacation and wages in lieu of notice. Severance and Retiring Allowances are not insurable and not included.

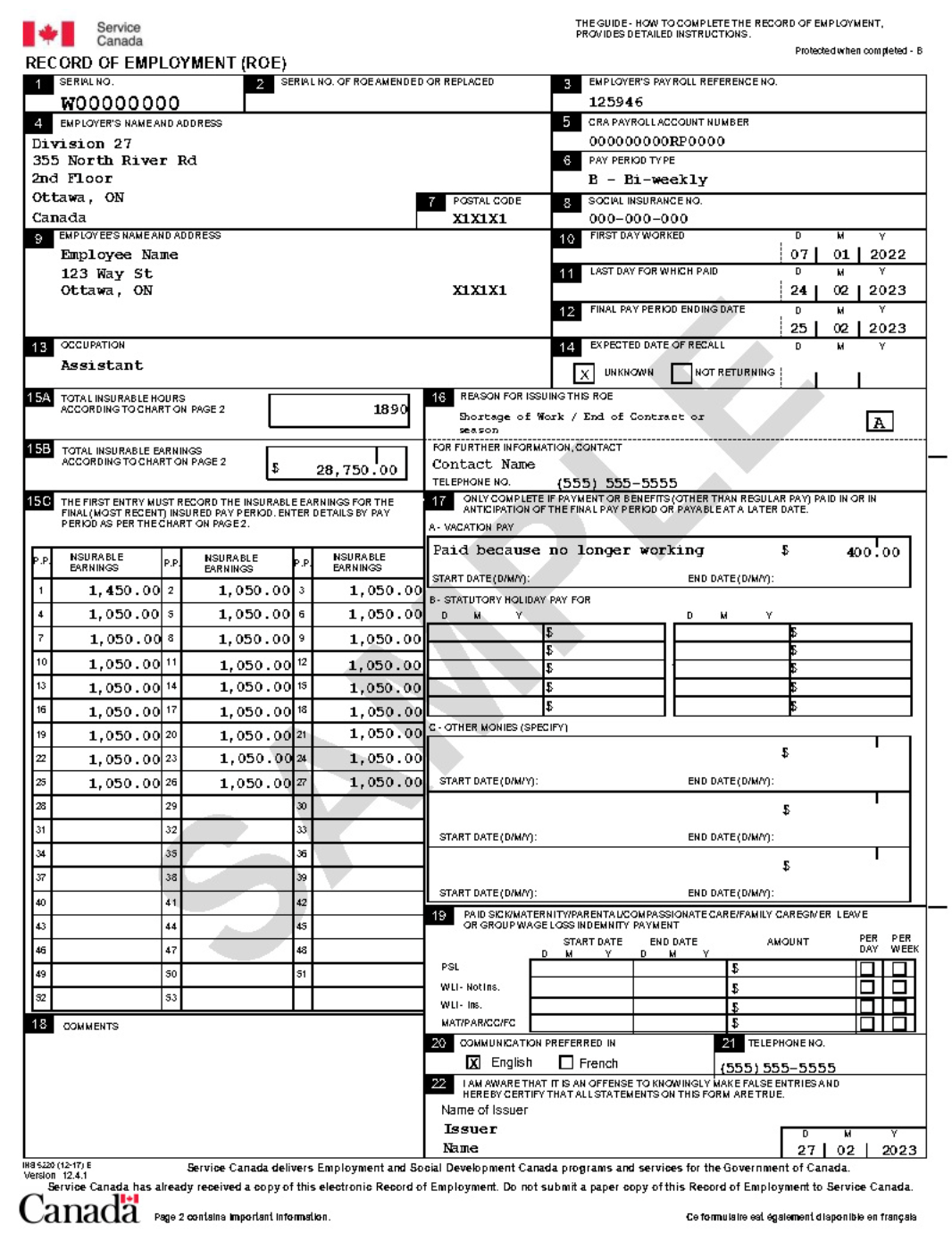

An example of a completed ROE form is shown below:

The following ROE blocks must be completed:

- Blocks 1 through 9, and Blocks 13 and 14 require administrative information to be inputted.

- Blocks 10 through 13 require information on the insurable hours and earnings during the employment period.

- Blocks 17A through 17C require amounts for any separation payments either paid or payable.

- Block 15A requires calculating insurable hours.

- Block 16 requires the reason for preparing the ROE.

- Block 18 allows the employer to record any additional information, usually for unique circumstances.

- Block 19 is completed when the employee is to receive paid leave related to illness, maternity, parental leave, compassionate leave, caregiver leave, and loss indemnity (group wage payment).

References

Government of Canada. (2024a). Access record of employment on the web for employers. https://www.canada.ca/en/employment-social-development/programs/ei/ei-list/ei-roe/access-roe.html

Service Canada. (2021). Employment insurance: How to complete the Record of Employment form. https://www.canada.ca/content/dam/canada/employment-social-development/migration/images/assets/portfolio/docs/en/reports/ei/roe_guide/pdf/3106-ROE-Web-layout-EN.pdf

Image Credits (images are listed in order of appearance)

Government of Canada. (2023). How to complete the record of employment (ROE) form. Annex 3: Example of a blank electronic ROE [Screenshot]. https://www.canada.ca/en/employment-social-development/programs/ei/ei-list/reports/roe-guide.html#h2.7

Government of Canada. (2023). How to complete the record of employment (ROE) form. Annex 4: Example of a completed electronic ROE [Screenshot]. https://www.canada.ca/en/employment-social-development/programs/ei/ei-list/reports/roe-guide.html#h2.7