Chapter 4: Statutory and Non-Statutory Deductions

4.1 Overview

In this chapter, you will learn about the most common payroll deductions from employees’ gross pay. There are three categories of deductions you will learn about: 1) source deductions, which are mandatory by law; 2) other mandatory deductions; and 3) non-mandatory or optional deductions.

Source deductions are required for all Canadian employees. The three core statutory source deductions are Canada Pension Plan (CPP) contributions, Employment Insurance (EI) contributions, and income tax. For each, you will learn what income is subject to deductions, the maximum income thresholds where applicable, and how to calculate the amount of the source deductions.

In addition to these federal requirements, certain provinces and territories impose additional statutory deductions. For example, both Nunavut and the Northwest Territories require employers to deduct a 2% Territorial Payroll Tax from employees’ gross earnings. This tax applies regardless of where the work is performed, as long as the employee is a resident of the territory. It is considered a statutory deduction because it is mandated by law and must be withheld at source, similar to CPP, EI, and income tax.

Several other mandatory deductions are also important for payroll compliance. These include deductions made under a Canada Revenue Agency (CRA) Requirement to Pay (RTP), court-ordered wage garnishments, wage assignments (not permitted by law in most jurisdictions, with limited exceptions), union dues, and pension contributions.

Finally, payroll processing also involves optional or non-mandatory deductions. These may include contributions to health benefit plans, insurance premiums, or social funds. Other deductions may be made by agreement between the employer and employee, provided they comply with employment standards legislation.

Payroll deductions are a key element of payroll processing. By learning how to accurately assess and apply these deductions, payroll professionals gain essential knowledge that ensures compliance with the law and accuracy in employee pay.

Specific Learning Outcomes

Upon successful completion of this chapter, you will be able to

- Identify the three statutory source deductions: CPP, EI, and income tax

- Determine which earnings are subject to CPP deductions and calculate employee CPP contributions

- Determine which earnings are subject to EI deductions and calculate employee EI deductions

- Determine taxable earnings and calculate income tax withholdings

- Identify other mandatory deductions and when they apply

- Identify non-mandatory (optional) payroll deductions and when they apply

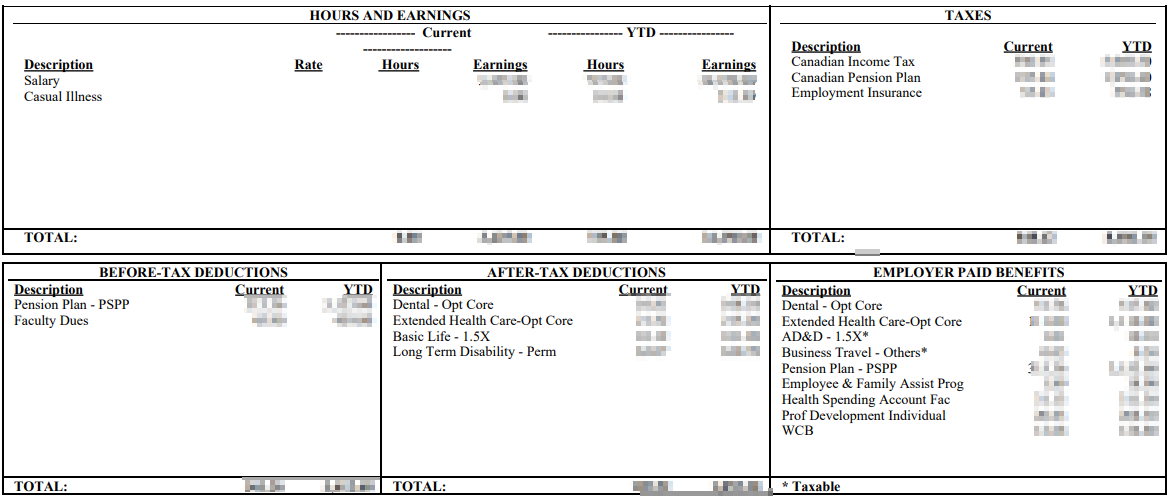

Image Credit

Employee pay stub by Meena Gupta, NorQuest College